Digital Agriculture Market Size, Share, Trends, Growth, and Industry Analysis By Business Channel, By Product Type, By Component Type, By Deployment, By Type, By Company Type, Regional Insights and Forecast to 2031

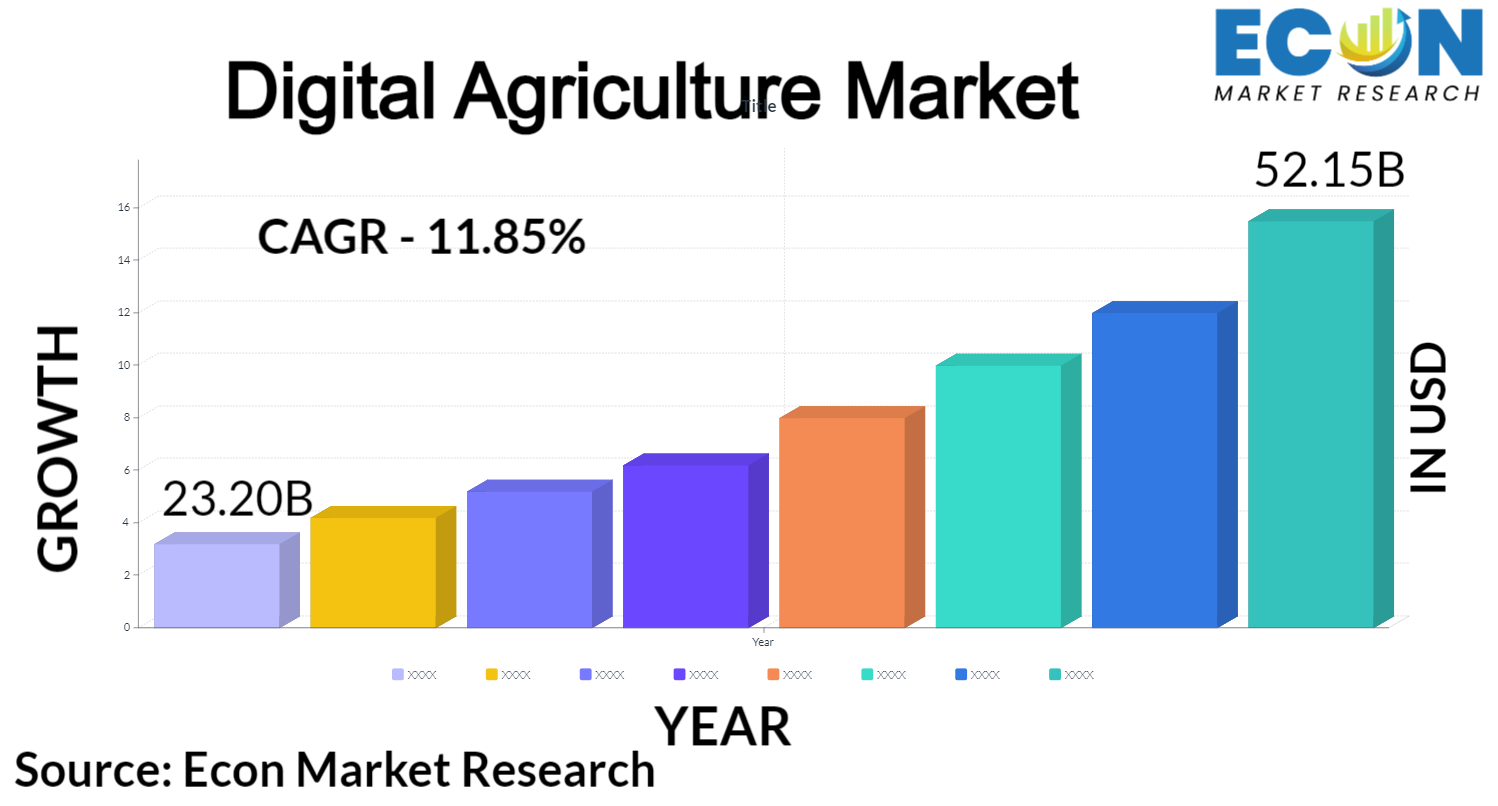

global digital agriculture market size was USD 23.20 billion in 2022 and is predicted to reach USD 52.15 billion in 2031, exhibiting at a CAGR of 11.85% during the forecast period.

Farmers are under increasing pressure to use fewer pesticides to produce more food and animal feed. It is getting harder to feed the growing population because of the rising population. Agriculture production is under more stress than before. The usage of precision farming software and Internet of Things solutions will benefit the agriculture industry. Digital agricultural instruments that employ sensors to track the growth of the crops and keep tabs on the temperature and soil quality in the fields are becoming more and more common. These tools let farmers examine the climate for the growth of different crops. Post-pandemic, farming is using internet channels much like all the other industries. Digital agriculture is seeing a surge in investments and technologies. The lives of diverse farmers around the world are getting better thanks to an increasing reliance on technology.

Market Growth

The expansion of the agriculture market can be attributed to a greater understanding of the advantages of digital agriculture in improving the optimization of agricultural production. Numerous farmers have started using these digital agricultural instruments as a result of the rising demand for food caused by the growing population. Strategic policymaking helps to encourage farmers to use these new technologies in many nations. The adoption of these new, cutting-edge technology by farmers is supported by a variety of agricultural consulting services, allowing them to use resources cost-effectively and effectively while also overcoming hurdles. Farmers can increase their yield and reduce losses by using these software programs.

Market Dynamics

Market Drivers

There has been a significant rise in the agriculture business as a result of growing knowledge about how digital agriculture may optimize agricultural production. Farmers will inevitably adopt digital agriculture equipment to keep up with the rising food demand brought on by the expanding world population. Farmers should be encouraged to use the relevant technology through strategic policy decisions made by the nations about precision farming. Science and practice are being bridged via farm advisory services. One of the main forces propelling the digital agriculture market is the technological developments and improvements, which assist farmers to optimize productivity and reducing losses through resource-efficient resource utilization.

Market Restraints

The lack of technological expertise among people is another factor that is anticipated to restrain the growth of the digital agriculture market over the forecast period. The quick standardization process, however, may present further difficulties for the development of the digital agriculture sector in the near future.

This report on the global digital agriculture market details recent developments, trade regulations, import-export analysis, production analysis, value chain optimization, market share, the impact of domestic and localized market players, analyses opportunities in terms of emerging revenue pockets, changes in market regulations, strategic market growth analysis, market size, category market growths, application niches and dominance, product approvals, product launches, and geographical information

Market Opportunities

Through improved yields and the avoidance or reduction of food loss, artificial intelligence and the Internet of Things have the potential to revolutionize agriculture. For example, the world population increased to 7.87 billion in 2021 from 7.76 billion in 2020, according to "The World Bank," a US-based international financial institution that offers loans and grants to the governments of low- and middle-income nations. The market for digital agriculture is therefore being driven by the growing population. A crucial trend gaining popularity in the digital agriculture market is the penetration of technology and electronic devices. To maintain their market share, major companies involved in digital agriculture are concentrating on the uptake of technology and electronic devices.

|

Report Attribute |

Details |

|

Projected CAGR in % |

11.85% |

|

Estimated Market Value (2022) |

23.20 Billion |

|

Base Year |

2022 |

|

Forecast Years |

2023 - 2031 |

|

Segments Covered |

By Business Channel, By Product Type, By Component Type, By Deployment, By Type, By Company Type |

|

Forecast Units |

Value (USD Billion), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2023 to 2031 |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, and Rest of World |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis, and COVID-19 impact analysis. |

Covid-19 Impact on the Digital Agriculture Market

Digital agriculture has suffered significantly as a result of the recent coronavirus outbreak. The COVID-19 pandemic produced supply chain delays, lockdowns, and a shortage of equipment, which led to a minor fall in the digital agricultural market in 2020. However, during the post-COVID-19 period, greater adoption may result through the usage of remote sensing and farm management software applications. The digital agriculture supply chain has been disrupted by COVID-19, and businesses are testing out novel technological approaches to interact with producers and farmers.

Competitive Landscape

Some of the major players operating in the digital agriculture market are:

Regional Analysis

During the time of forecasting, the Asia-Pacific region is anticipated to lead the global digital agricultural market. Regarding the use of smart farming techniques, the Chinese agriculture sector has undergone a major change. The market is anticipated to expand as a result of the use of sensor-based technologies such as gear tooth sensor-based irrigation and fertilizer equipment. Mechanization has accelerated, and farmers are embracing innovative agricultural techniques. India's progress toward agricultural modernization and vitalization is greatly aided by digital technology. The growth of technologically advanced agricultural equipment, which is readily available throughout the Asia Pacific area, as well as an increase in government support for the formation of these tech enterprises, are what is driving the market for digital agriculture in this region.

Report Segmentations

Product Type Insight

The perishable segment is anticipated to rule the market over the forecast period based on product type. Perishable items in the online agriculture market include dairy goods, fresh fruits and vegetables, meat, fish, and poultry.

Business Channel Insight

In the market for digital agriculture, it is anticipated that the B2B segment will hold the largest market share. Instead of the end user and the company, B2B commerce takes place between businesses. The farmers are given access to a wide range of resources, including software tools, data analysis, and value-added services for logistics. These B2B services help farmers increase the productivity and cultivation of their crops.

Recent Development

Segmentations

By Business Channel

By Product Type

By Component Type

By Deployment

By Type

By Geography

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.