Global Wind Turbine Market Research Report: By Axis Type (Horizontal and Vertical), By Installation (Onshore and Offshore), By Component (Rotator Blade, Gearbox, Generator, Nacelle, and Others), By Application (Industrial, Commercial, Residential, and Utility), and Region (North America, Europe, Asia-Pacific, and Rest of the World) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2023-2031.

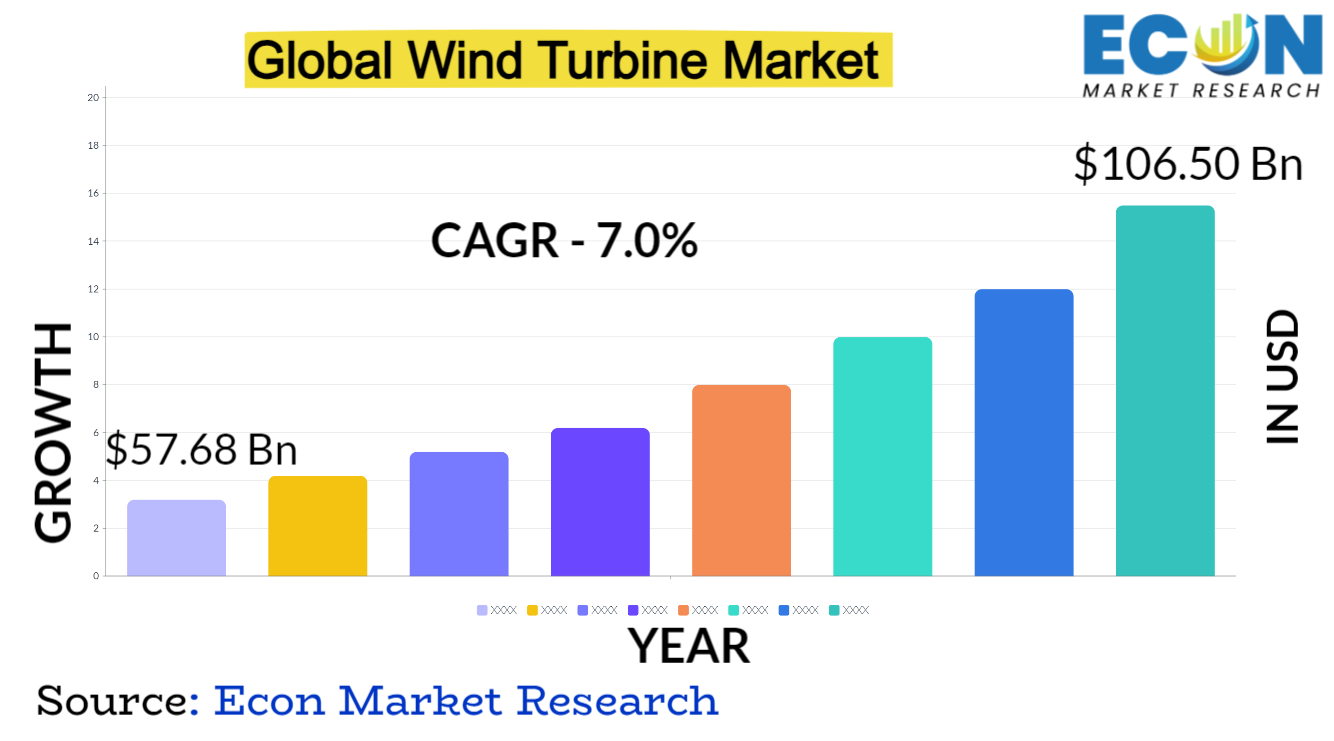

The global wind turbine market was valued at USD 57.68 billion in 2022 and is estimated to reach approximately USD 106.50 billion by 2031, at a CAGR of 7.0% from 2023 to 2031.

Since its launch, the worldwide wind turbine market has grown and innovated remarkably. Wind turbines, which capture and transform wind energy into electrical power, are becoming a major player in the sustainable energy space. Since their inception, technological developments have produced more cost-effective, capacity-boosting turbines that are also more efficient. Significant investments in R&D and infrastructure have been made in this area as a result of growing environmental concerns and the push to use renewable energy sources. The market's growth has also been aided by government programs supporting sustainable energy and the falling cost of producing wind power. Larger and more potent turbines can now be placed in maritime environments thanks to the development of offshore wind farms, which has also opened up new possibilities for wind energy harvesting. Forecasts indicate that the market will continue to grow at a promising rate due to technology advancements, policies that are supportive of the industry, and increased global awareness of the critical need for clean and sustainable energy solutions.

WIND TURBINE MARKET: REPORT SCOPE & SEGMENTATION

|

Report Attribute |

Details |

|

Estimated Market Value (2022) |

57.68 Bn |

|

Projected Market Value (2031) |

106.50 Bn |

|

Base Year |

2022 |

|

Forecast Years |

2023 - 2031 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- By Axis Type, By Installation, By Component, By Application, & Region |

|

Segments Covered |

By Axis Type, By Installation, By Component, By Application, & Region |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2023 to 2031 |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, and the Rest of World |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis, and COVID-19 impact analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Global Wind Turbine Market Dynamics

Turbine efficiency is continuously improved by technological advancements, which also increase capacity and lower operating costs. The progress of the market is influenced by various factors, including the development of larger rotor diameters, taller towers, and more complex materials. Government rules and policies are crucial because they influence market demand by providing incentives and subsidies to encourage the use of renewable energy. Economic variables including shifting energy prices and wind power's cost competitiveness with respect to other energy sources influence market dynamics as well. Moreover, the market is greatly influenced by the interaction of supply chain dynamics, which include production, transportation, and maintenance. Market dynamics are further influenced by social pressure for sustainable energy solutions and worldwide environmental concerns. International agreements and trade policies are other geopolitical elements that can affect the direction of the wind turbine business. The market dynamics are defined by a precarious equilibrium of governmental frameworks, technological innovation, economic volatility, and societal needs, all of which influence the wind turbine industry's growth trajectory and rate.

Global Wind Turbine Market Drivers

In an effort to mitigate climate change and lessen reliance on fossil fuels, governments over the world are progressively putting laws into place that support renewable energy sources. A variety of incentives, including feed-in tariffs, tax credits, renewable portfolio standards, and subsidies, are frequently included in these policies to encourage investment in wind energy infrastructure by both individuals and companies. By lowering the costs and hazards involved in implementing wind turbines, these programs foster a market expansion atmosphere. Governments encourage private sector participation and innovation in renewable energy projects by providing financial incentives. Additionally, these rules offer regulatory certainty, which promotes long-term planning and dedication from market participants for wind turbines. Policies promoting renewable energy not only hasten the installation of wind turbines but also support economic expansion, job development, and environmental sustainability. They encourage consumer behavior and business decisions to use cleaner energy sources by sending a strong message about their commitment to a greener future.

Improvements are made in several areas, including as materials science, control systems, blade aerodynamics, and turbine construction as a whole. By improving energy capture, lengthening the lifespan of turbines, and lowering operating expenses, these advancements seek to make wind power more competitive. Blade design advancements allow turbines to more efficiently capture energy from lower wind speeds by optimizing blade shapes for greater efficiency and quieter operation. Innovations in material science are concentrated on creating stronger, lighter materials that extend the life and performance of turbines. Furthermore, improvements in data analytics and control systems allow for improved monitoring and predictive maintenance, which lowers downtime and boosts overall operating efficiency. The trend toward larger turbines, which capture more wind energy and provide economies of scale, is also driven by technological advancement. The industry continuously pushes the envelope through expenditures in research and development to create next-generation turbines that are more economical and efficient. These developments raise the competitiveness of wind power over traditional energy sources by lowering the levelized cost of energy (LCOE) and enhancing wind turbine performance.

Restraints:

Because wind resources are inherently erratic, it can be challenging to maintain a steady power output because wind speeds vary and cause uneven energy production. Strong grid integration solutions are needed to manage the variability and unpredictability of wind power, which is made more difficult by the intermittency of wind power. The timing of wind power output and electricity use is one of the main issues. Because wind resources are unpredictable, it becomes more difficult to balance supply and demand, which increases the risk of grid instability and dependability problems. Furthermore, the geographic distribution of wind farms frequently deviates from regions with strong energy demand, making efficient transmission and grid infrastructure necessary for the long-distance delivery of energy. The necessity for cutting-edge technologies, including energy storage devices, to store excess energy during times of strong wind and release it when wind speeds drop, is one of the issues associated with grid integration. Furthermore, to account for the erratic nature of wind energy, improvements to the grid infrastructure are essential. These include more intelligent grid management systems and adaptable demand-response mechanisms. In order to overcome these obstacles, significant investments in technology advancements and grid modernization are needed to create more complex grid systems that can smoothly integrate intermittent renewable energy sources like wind power while maintaining grid stability and dependability.

Purchasing turbines, preparing the site, installing them, and connecting them to the grid all come at a large upfront expense when starting a wind farm. These expenses frequently act as a barrier, impeding the quick installation of wind energy infrastructure, particularly for smaller investors or areas with restricted access to money. Furthermore, there are risks and uncertainties related to finances because wind energy projects require a lot of resources. Some investors are put off by these investments' extended payback periods, which can last anywhere from a few years to a decade or longer. This is because it takes a while to recover initial costs and turn a profit. Financial difficulties make this limitation more worse. Funding wind projects can be difficult to get and require cooperation from a variety of organizations, including banks, governments, and private investors. Furthermore, investor confidence may be impacted by unclear long-term regulations and incentives, which makes it difficult to consistently raise capital for wind energy projects. Wind energy's competitiveness with respect to conventional sources is also impacted by its high initial investment costs. Even while wind farms have relatively low operating costs, their large upfront capital requirements frequently prevent their fast adoption and growth, especially in areas or markets with weaker infrastructure or financial resources.

Opportunities:

Compared to their onshore equivalents, offshore wind farms have a number of benefits, chief among them being the availability of stronger and more reliable wind resources at sea. More energy can be produced as a result of the installation of larger, more capable turbines made possible by the steady and ample wind flow. In addition, compared to onshore projects, offshore wind farms have less land restrictions, which allows for the construction of larger facilities. Large oceanic areas offer sufficient room for the installation of wind turbines, which can allay aesthetic and environmental issues related to onshore installations. The prospective locations for offshore wind farms have increased due to the technological developments in offshore wind turbine design, which have made it possible to put deeper water installations and float platforms, opening up new opportunities for wind energy production in deeper oceans. Furthermore, being close to coastal urban centers lowers transmission losses and makes it easier to distribute electricity efficiently to areas with high demand, which eases grid congestion. The offshore wind industry's expansion offers financial prospects as well, which stimulate the creation of jobs, particularly in coastal areas where wind farms are built and maintained.

Smart grids improve energy distribution networks' flexibility, dependability, and efficiency by utilizing cutting-edge digital communication and control technologies. Smart grid technologies, in particular, make it easier to integrate power systems for wind turbines by enabling real-time power generation and distribution monitoring, control, and management. This capacity is especially important for managing the intermittent nature of wind energy. By enabling dynamic modifications in response to variations in wind speed, smart grids maximize the use of available wind resources and enhance grid stability. Predictive maintenance techniques for wind turbines could be implemented with the help of digitalization. Predictive analytics is the ability to anticipate probable defects or maintenance needs by gathering and analyzing enormous volumes of operational data. This allows for proactive and timely interventions. By using a predictive strategy, turbine performance is improved, downtime is decreased, and operational lifespan is increased. Moreover, demand-side management programs and energy storage systems can be integrated more easily thanks to the cooperation between smart grids and renewable energy sources like wind power.

Segment Overview

By Axis Type

Based on axis type, the global wind turbine market is divided into horizontal and vertical. The vertical category dominates the market with the largest revenue share in 2022. VAWTs have their rotor axis aligned vertically, and the blades rotate around a vertical axis. Unlike HAWTs, VAWTs do not need to be pointed directly into the wind to generate power, making them potentially suitable for areas with turbulent or changing wind directions. They are often considered for urban or low-wind-speed environments due to their compact size and lower noise profile compared to HAWTs. VAWTs are available in various configurations such as Darrieus, Savonius, and helical designs, each with its unique blade arrangement. HAWTs are the most commonly deployed type of wind turbines globally. They feature a horizontal rotor shaft, with blades attached at a perpendicular angle to the shaft. As the wind flows parallel to the ground, it causes the blades to rotate around a horizontal axis, harnessing wind energy to generate electricity. HAWTs come in various sizes, from small-scale residential turbines to large utility-scale turbines used in wind farms. These turbines typically have higher efficiency due to their ability to capture wind from various directions by employing a yaw mechanism to orient themselves into the wind.

By Installation

Based on the installation, the global wind turbine market is categorized into onshore aOnshore wind turbines are installed on land and represent the more traditional and commonly deployed type of wind energy generation. These wind farms are typically situated in various terrains, including plains, hills, and mountainous regions, depending on the availability of suitable wind resources. Onshore wind turbines are relatively easier and less expensive to install and maintain compared to offshore installations. They benefit from easier access for installation, maintenance, and grid connection, leading to lower upfront costs.nd offshore. The onshore category leads the global wind turbine market with the largest revenue share in 2022. Offshore wind turbines are installed in bodies of water, usually in coastal areas or farther out at sea. These installations harness stronger and more consistent wind speeds compared to onshore locations, offering the potential for higher energy production. Offshore wind farms have larger turbines and benefit from better wind conditions, resulting in increased efficiency and power generation. However, offshore installations involve more complex engineering, installation, and maintenance processes due to the harsh marine environment, deeper water depths, and logistical challenges.

By Component

Based on component, the global wind turbine market is segmented into rotator blade, gearbox, generator, nacelle, and others. The rotator blade segment dominates the wind turbine market. Rotor blades are aerodynamic components attached to the hub of the wind turbine. Their primary function is to capture the kinetic energy from the wind and convert it into rotational energy. These blades come in different sizes, shapes, and materials, designed to optimize energy capture and withstand varying wind conditions. Advances in blade design focus on improving efficiency, reducing noise, and enhancing durability. The gearbox is an essential component that facilitates the conversion of low-speed rotation from the rotor into high-speed rotation for the generator. It contains a system of gears that adjusts the rotational speed to match the generator's requirements. Gearboxes have been a critical area for innovation to improve efficiency, reduce maintenance needs, and mitigate issues related to wear and tear. The generator is responsible for converting the mechanical energy generated by the spinning rotor into electrical energy. Typically, wind turbines use synchronous or asynchronous generators to produce electricity. Advancements in generator technology focus on improving efficiency, reliability, and grid compatibility. The nacelle houses crucial components such as the gearbox, generator, control systems, and other electronics. It sits atop the tower and supports the rotor and blades. Nacelles are designed to protect internal components from harsh weather conditions and ensure efficient operation of the turbine.

By Application

Based on application, the global wind turbine market is divided into industrial, commercial, residential, and utility. The utility category dominates the market with the largest revenue share in 2022. Utility-scale wind turbines are large installations primarily developed by utility companies or independent power producers for supplying electricity to the grid. These wind farms consist of numerous large turbines placed in optimal locations with favorable wind conditions. Utility-scale wind turbines contribute significantly to the overall energy production, providing electricity to meet the demands of cities, regions, or even entire countries. Industrial applications of wind turbines involve larger-scale installations used for powering industrial operations, manufacturing facilities, or industrial complexes. These turbines are typically larger in size and have higher power capacities, providing electricity to meet the significant energy demands of industrial processes. Industrial wind turbines often contribute to offsetting the power consumption of factories or industrial sites, promoting sustainable and cost-effective energy solutions for large-scale operations. Commercial applications involve wind turbines installed for commercial purposes such as offices, retail centers, hotels, or small businesses. These turbines are generally smaller in size compared to industrial turbines but larger than those used for residential purposes. Commercial wind turbines aim to supplement the energy needs of commercial establishments, reduce operational costs, and demonstrate a commitment to sustainability, often visible as part of a company's corporate social responsibility initiatives. Residential wind turbines are designed for individual homes or small communities. These turbines are smaller in size compared to industrial or commercial variants, typically mounted on rooftops or installed in backyards. Residential wind turbines cater to the energy needs of households, providing a supplementary or alternative energy source to reduce reliance on the traditional power grid. They offer homeowners the opportunity to generate their electricity, reduce utility bills, and contribute to environmental conservation.

Global Wind Turbine Market Overview by Region

The global wind turbine market is categorized into North America, Europe, Asia-Pacific, and the Rest of the World. Asia-Pacific emerged as the leading region, capturing the largest market share in 2022. Demand for energy is rising as a result of the Asia-Pacific region's fast industrialization and economic growth. To keep up with this growing demand, governments in nations like China, India, and South Korea are aggressively looking for greener and more sustainable energy sources. With its plentiful resources and falling costs, wind energy is emerging as a desirable solution to close the energy gap. To encourage the use of wind energy, governments around the region have put in place supportive policies, such as feed-in tariffs, renewable energy targets, subsidies, and incentives. These regulations promote investment in wind energy projects, creating a favorable atmosphere for market expansion. Asia-Pacific countries have made significant investments in R&D, which has accelerated the development of wind turbine technology. This has increased the competitiveness and dependability of wind energy through the development of more effective turbines, creative designs, and enhanced manufacturing procedures. The wind power capacity of nations like China, India, Australia, and Japan has increased dramatically in the last several years. With constant investments in onshore and offshore wind projects, China has emerged as the world's largest market for wind energy, helping to diversify its energy mix and lessen its dependency on fossil fuels. Due to the significant investments made by both domestic and foreign companies, the wind energy sector in the region is growing. The Asia-Pacific region has emerged as a leader in the worldwide wind turbine market thanks to technology breakthroughs, favorable government regulations, and expanding market prospects.

Global Wind Turbine Market Competitive Landscape

In the global wind turbine market, a few major players exert significant market dominance and have established a strong regional presence. These leading companies remain committed to continuous research and development endeavors and actively engage in strategic growth initiatives, including product development, launches, joint ventures, and partnerships. By pursuing these strategies, these companies aim to strengthen their market position, expand their customer base, and capture a substantial share of the market.

Some of the prominent players in the global wind turbine market include Vestas Wind Systems, Siemens Gamesa Renewable Energy, General Electric (GE) Renewable Energy, Goldwind, Nordex Group, Enercon, Suzlon Energy, Envision Energy, MingYang Smart Energy, Xinjiang Goldwind Science & Technology Co., Ltd., United Power, and various other key players.

Global Wind Turbine Market Recent Developments

In November 2023, The state-owned Temasek Holdings Pte investor is supporting the Singaporean energy company, which plans to purchase 200 MW of Qinzhou Yuanneng for 130 million Singaporean dollars and 228 MW of operating wind power assets from Leap Green Energy Pvt Ltd for 70 million Singaporean dollars.

In September 2023, With the acquisition of Breeze Two Energy in Germany and France, Statkraft, the biggest generator of renewable energy in Europe, has increased the range of wind power projects it offers. With this transaction, Statkraft's repowering portfolio—which already includes 39 wind farms—is increased by 337 MW. The portfolio was purchased for NOK 4.7 billion.

Wind Turbine Market Report Segmentation

|

ATTRIBUTE |

DETAILS |

|

By Axis Type |

|

|

By Installation |

|

|

By End-Use |

|

|

By Application |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Objectives of the Study

The objectives of the study are summarized in 5 stages. They are as mentioned below:

To identify and estimate the market size for the global wind turbine market segmented by axis type, by installation, by end use , by application, region and by value (in U.S. dollars). Also, to understand the consumption/ demand created by consumers of wind turbine between 2019 and 2031.

To identify and infer the drivers, restraints, opportunities, and challenges for the global wind turbine market

To find out the factors which are affecting the sales of wind turbine among consumers

To identify and understand the various factors involved in the global wind turbine market affected by the pandemic

To provide a detailed insight into the major companies operating in the market. The profiling will include the financial health of the company's past 2-3 years with segmental and regional revenue breakup, product offering, recent developments, SWOT analysis, and key strategies.

Intended Audience

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.