Global Smart Insulin Pens Market Report: By Type (First Generation Pens, and Second Generation Pens), Usability (Prefilled, and Reusable), Connectivity Type (Bluetooth, and USB), Application (Type 1 Diabetes, and Type 2 Diabetes), and Region (North America, Europe, Asia-Pacific, Latin America, Middle-East and Africa) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2023-2031.

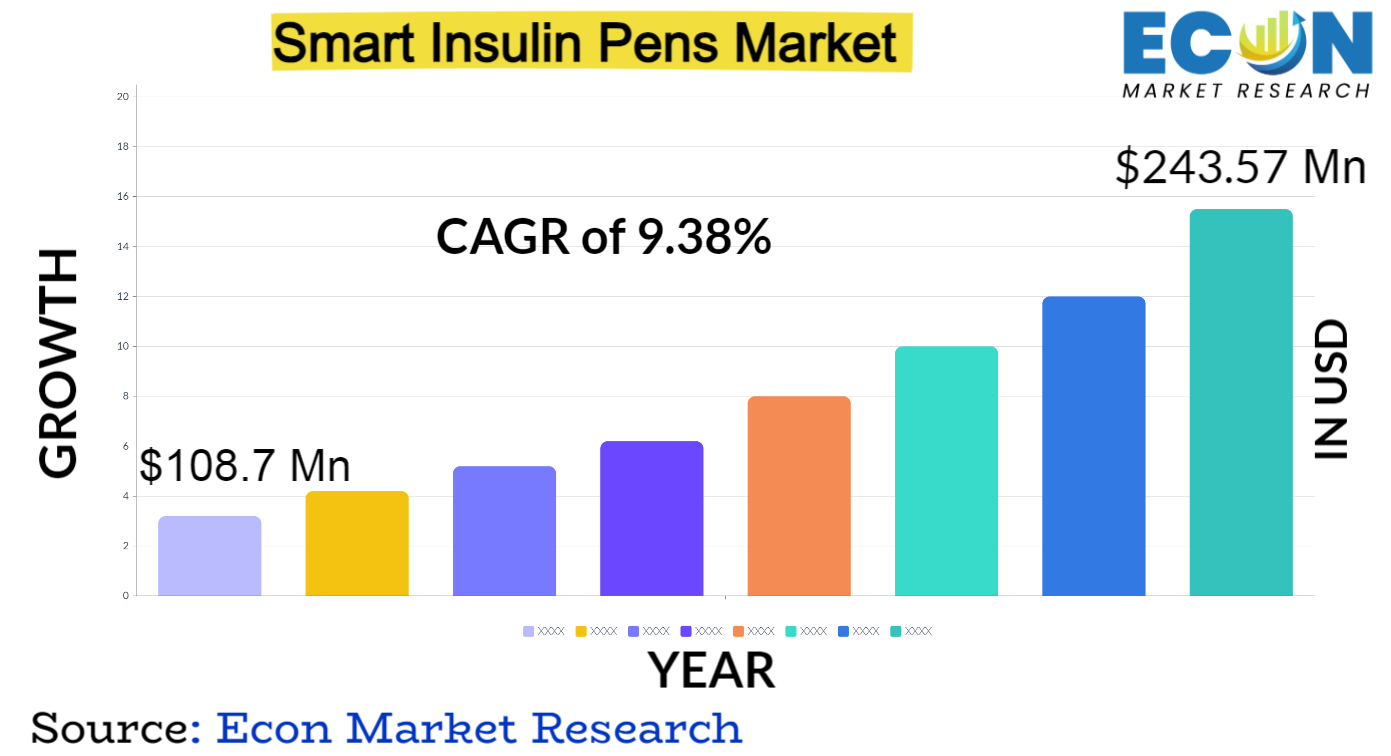

Global Smart Insulin Pens market is predicted to reach approximately USD 243.57 million by 2031, at a CAGR of 9.38% from 2022 to 2031.

Smart insulin pens are cutting-edge tools made to improve the accuracy and convenience of insulin delivery for people with diabetes. With the help of these pens, which combine dose monitoring, data analytics, and Bluetooth connectivity, patients can better monitor and control their insulin consumption. The global rise in diabetes prevalence and the growing need for connected, user-friendly healthcare solutions are driving the market.

In addition to automatically recording insulin doses and providing real-time dosage information, smart insulin pens can share data with healthcare providers via mobile applications. Improved patient outcomes, individualised treatment plans, and remote monitoring are made possible by this connectivity. Pharmaceutical companies and technology companies work together to develop cutting-edge smart insulin pen solutions, which is what defines the market. These devices' combined use of AI and machine learning improves their capabilities even further, offering predictive insights into patient behaviour and enhancing insulin therapy.

Global Smart Insulin Pens report scope and segmentation.

|

Report Attribute |

Details |

|

Estimated Market Value (2022) |

USD 108.7 million |

|

Projected Market Value (2031) |

USD 243.57 million |

|

Base Year |

2022 |

|

Forecast Years |

2023 – 2031 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- Based on By Product, Type, Usability, Connectivity Type, Application, Distribution Channel & Region. |

|

Segments Covered |

By Product, Type, Usability, Connectivity Type, Application, Distribution Channel & By Region. |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2023 to 2031. |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others. |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Global Smart Insulin Pens dynamics

The increasing global incidence of diabetes is a major factor driving the need for novel approaches to improve the accuracy of insulin delivery. The use of smart insulin pens is being fuelled by the increasing emphasis on patient-centered healthcare and the demand for connected, user-friendly tools for managing diabetes. Furthermore, new developments in technology—like data analytics and Bluetooth connectivity—are transforming insulin therapy by enabling smooth communication between patients and medical professionals and providing real-time dosage information.

Strategic partnerships between technology companies and pharmaceutical companies further shape the market dynamics and encourage the development of advanced smart insulin pen solutions. The goal of ongoing research and development is to incorporate machine learning and artificial intelligence into these devices so that predictive analytics can be used to create more individualised treatment regimens. Notwithstanding these encouraging developments, issues like the high price of smart insulin pens and worries about data security remain barriers to widespread adoption.

Global Smart Insulin Pens drivers

The increasing incidence of diabetes worldwide is a major factor driving the growth of the market for smart insulin pens. The need for sophisticated and user-friendly insulin delivery systems is rising as more people are being diagnosed with diabetes. The adoption of smart insulin pens by patients and healthcare providers is fuelled by their connectivity features and data tracking capabilities, which address the need for more effective diabetes management.

The market for smart insulin pens is significantly driven by the ongoing advancements in technology, especially in the areas of data analytics, artificial intelligence, and Bluetooth connectivity. By giving real-time data on insulin dosages, enabling remote monitoring, and providing predictive insights for individualised treatment plans, these technological advancements improve the functionality of smart insulin pens. By incorporating these features, healthcare providers are better equipped to make educated decisions and increase patient adherence, which in turn fuels the market's expansion.

Restraints:

A significant impediment to the growth of the smart insulin pen market is the comparatively elevated expense linked to these cutting-edge technological instruments. Cost is still a major concern, especially in developing nations where access to high-priced medical equipment may be restricted. The cost of smart insulin pens makes them difficult to adopt widely, impeding market penetration and possibly restricting their benefits to a particular group of people.

The integration of digital features in smart insulin pens raises concerns about data security and patient privacy. The storage and transmission of sensitive health information through connected devices create potential vulnerabilities. Addressing these concerns is crucial for gaining the trust of patients and healthcare providers, as well as ensuring compliance with data protection regulations, which may otherwise impede the market's growth.

Opportunities:

In developing nations where diabetes is becoming more common, there are large growth prospects in the smart insulin pen market. Reaching these areas presents an opportunity to take care of unmet medical needs and reach a consumer base that hasn't been reached before. For market participants, customising smart insulin pen solutions to the unique needs of various demographics offers a strategic advantage.

Segment Overview

The Smart Insulin Pens Market is segmented by product into four categories: Smart Insulin Pens, Adaptors for Conventional Pens, Disposable Pens, and Reusable Pens. Smart Insulin Pens represent the forefront of innovation, integrating digital technology to provide features such as dose tracking and connectivity. Adaptors for Conventional Pens offer a bridge to digitization for traditional insulin pens. Disposable and Reusable Pens cater to diverse patient preferences, with disposable options providing convenience and reduced infection risk, while reusable pens offer a sustainable and cost-effective solution.

The market is further categorized by type into First Generation Pens and Second Generation Pens. First Generation Pens laid the foundation for smart insulin delivery, featuring basic connectivity. Second Generation Pens represent a leap forward, incorporating advanced technologies such as artificial intelligence and machine learning. This segmentation reflects the evolutionary trajectory of smart insulin pen technology, showcasing the continuous innovation within the market.

Usability is categorized into Prefilled and Reusable options. Prefilled pens provide convenience, eliminating the need for manual insulin filling and simplifying dosage administration. Reusable pens, on the other hand, offer sustainability and cost-effectiveness, allowing patients to replace insulin cartridges while retaining the pen device. This segmentation addresses the diverse preferences and requirements of individuals managing diabetes, providing options that align with their lifestyle and treatment needs.

The connectivity aspect is divided into Bluetooth and USB options. Bluetooth-enabled pens enable seamless wireless communication, facilitating real-time data tracking and remote monitoring. USB connectivity provides a more direct and traditional method for data transfer. This segmentation highlights the importance of connectivity in smart insulin pens, offering patients and healthcare providers choices that align with their technological preferences and compatibility.

The application segment is divided into Type 1 Diabetes and Type 2 Diabetes. This categorization recognizes the distinct needs of these patient groups. Type 1 Diabetes patients, who require insulin for survival, benefit from the precise dosage control and connectivity features of smart pens. Type 2 Diabetes patients, who may use insulin as part of their treatment plan, can also benefit from the convenience and data tracking capabilities of smart insulin pens, addressing the specific requirements of each diabetes type.

The distribution channels include Hospital Pharmacies, Online Sales, Retail Pharmacies, and Diabetes Clinics/Centers. These channels cater to the varied preferences and accessibility of patients. Hospital Pharmacies provide institutional access, while Online Sales offer convenience and a wide reach. Retail Pharmacies serve as accessible community hubs, and Diabetes Clinics/Centers provide specialized care and guidance. This segmentation reflects the diverse avenues through which smart insulin pens reach end-users, ensuring a comprehensive and accessible market presence.

Global Smart Insulin Pens Overview by Region

North America is leading the market growth due to its sophisticated healthcare systems, high diabetes prevalence, and early adoption of new technologies. Because of the region's favourable reimbursement policies and strong pharmaceutical industry, smart insulin pens are becoming more widely integrated.

The market for smart insulin pens is growing in Europe as nations place a higher priority on digital health solutions. Adoption of these novel devices is encouraged by the prevalence of diabetes and the proactive management of chronic illnesses. With a rapidly increasing number of people living with diabetes and a growing awareness of cutting-edge diabetes management technologies, the Asia-Pacific region is starting to emerge as a major player in the market. China and India are important contributors, with an increasing emphasis on addressing the diabetes burden and enhancing healthcare infrastructure.

Latin America and the Middle East & Africa regions are experiencing a gradual uptake of smart insulin pens. Factors such as improving economic conditions, increasing healthcare investments, and growing awareness of diabetes management contribute to market expansion in these regions. However, challenges related to accessibility, affordability, and technological infrastructure may impact the pace of adoption.

Global Smart Insulin Pens market competitive landscape

Key players such as Novo Nordisk, Eli Lilly and Company, and Sanofi dominate the market with their extensive experience in insulin therapies. These companies have been at the forefront of developing smart insulin pens, integrating connectivity features, and leveraging their established market presence to introduce advanced products.

In addition to traditional pharmaceutical giants, technological innovators like Companion Medical and Bigfoot Biomedical are making significant strides in the market. These companies bring a fresh perspective, focusing on the convergence of cutting-edge technology and healthcare to create smart insulin pen solutions with enhanced features and usability. The competitive landscape is characterized by strategic collaborations, mergers, and acquisitions as companies seek to bolster their technological capabilities and broaden their product portfolios.

Furthermore, start-ups such as Common Sensing and Emperra GmbH are contributing to the competitive dynamics by introducing novel approaches to smart insulin pen development. These agile and innovative firms often focus on specific technological niches, such as data analytics or user interface design, to differentiate themselves in the market. The increasing emphasis on patient-centric solutions and the demand for personalized diabetes management tools are driving competition, prompting companies to continuously innovate and enhance their offerings.

Global Smart Insulin Pens Recent Developments

Scope of global Smart Insulin Pens report

Global Smart Insulin Pens report segmentation

|

ATTRIBUTE |

DETAILS |

|

By Product |

|

|

By Type |

|

|

By Usability |

|

|

By Connectivity Type |

|

|

By Application |

|

|

Distribution Channel |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Objectives of the Study

The objectives of the study are summarized in 5 stages. They are as mentioned below:

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.