Powered Surgical Tools Market Report: By Power Source (Electric Instruments, Battery-Powered Instruments, Pneumatic Instruments), Product (Handpieces, Power Sources and Controls, Accessories), Application (Orthopedic Surgery, Oral and Maxillofacial Surgery, Neurosurgery, ENT Surgery, Cardiothoracic Surgery, Plastic and Reconstructive Surgery), and Region (North America, Europe, Asia-Pacific, Latin America, Middle-East and Africa) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2023-2031.

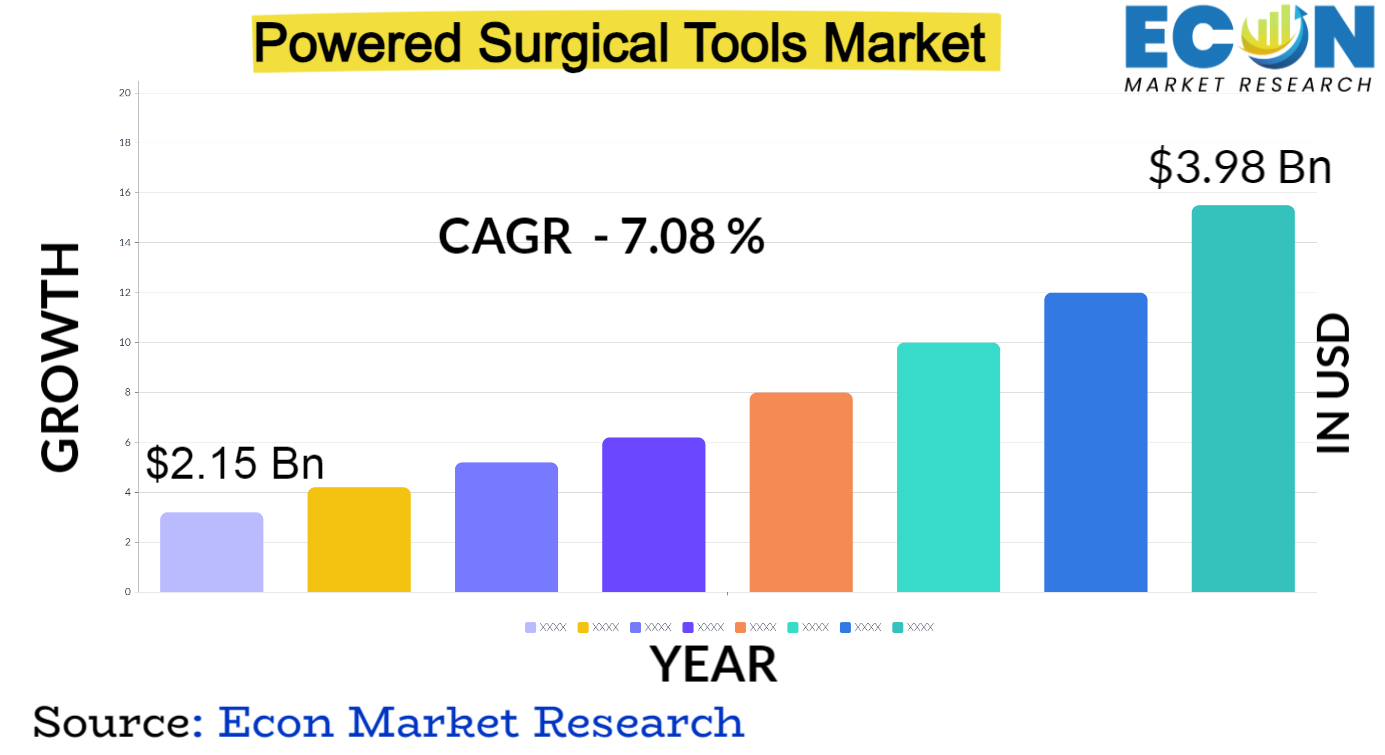

Global Powered Surgical Tools market is predicted to reach approximately USD 3.98 billion by 2031, at a CAGR of 7.08% from 2022 to 2031.

Surgical instruments that use electric or pneumatic power to carry out different surgical tasks accurately and effectively are referred to as powered surgical tools. Numerous surgical specialties, such as orthopaedics, neurology, cardiology, and general surgery, use these instruments extensively. They are essential in improving surgical results because they give surgeons more control, less fatigue, and better procedural accuracy.

The growing need for minimally invasive surgeries, which call for specialised powered instruments for complex procedures, is driving the market's expansion. The market is growing as a result of technological advancements like the incorporation of robotics and intelligent features in powered surgical instruments. Furthermore, the need for surgical interventions is increasing due to an ageing population and a rise in chronic diseases, which is propelling the adoption of these cutting-edge instruments. Geographically, North America and Europe have emerged as major drivers of the market's success because of their strong healthcare systems and high levels of knowledge about the advantages of powered surgical instruments.

Powered Surgical Tools Report Scope and Segmentation

Powered Surgical Tools Report Scope and Segmentation

|

Report Attribute |

Details |

|

Estimated Market Value (2022) |

USD 2.15 billion |

|

Projected Market Value (2031) |

USD 3.98 billion |

|

Base Year |

2022 |

|

Forecast Years |

2023 – 2031 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- Based on By Power Source, Product, By Application & Region. |

|

Segments Covered |

By Power Source, Product, By Application & By Region. |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2023 to 2031. |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others. |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Powered Surgical Tools Dynamics

One of the main factors driving the need for surgical interventions and, in turn, the uptake of powered surgical instruments is the growing incidence of chronic diseases and an ageing population. One important trend is the move towards minimally invasive surgeries. These instruments provide more control and precision for complex procedures, which helps patients heal more quickly. Furthermore, the market is continually changing due to technological advancements like the addition of robotics and smart features, which give surgeons access to state-of-the-art instruments that enhance procedural outcomes.

The market is confronted with obstacles, though, such as strict legal requirements and the high price of sophisticated surgical instruments. Adherence to regulatory requirements is crucial, requiring substantial expenditures in research and development for innovative product creation and safety observance. The significant initial investment required for these tools places a financial strain on healthcare professionals and facilities, which restrains market expansion. Additionally, the changing landscape of healthcare reimbursement and policy frameworks has an impact on market dynamics and healthcare providers' purchasing decisions.

Powered Surgical Tools Drivers

One of the main factors driving the global market for powered surgical tools is the ongoing advancement of technology and creative product creation. Continuous developments improve surgical accuracy, control, and overall results. Examples include the incorporation of robotics, artificial intelligence, and smart features into powered surgical instruments. Surgeons are looking for tools more and more that can automate tasks, give real-time feedback, and increase operating room efficiency. In addition to satisfying the increasing need for sophisticated instruments, this push for technological excellence creates a competitive environment where businesses must spend in R&D to stay ahead of the curve.

The market for powered surgical tools is significantly driven by the rising incidence of chronic diseases, such as neurological disorders, orthopaedic disorders, and cardiovascular conditions. The increasing prevalence of these health problems raises the need for surgical interventions, which in turn raises the use of powered instruments. The market is further stimulated by the fact that an increase in surgical procedures is a result of the ageing global population. The capacity of powered surgical instruments to provide accuracy in intricate procedures and reduce invasiveness corresponds with the requirements of patients with long-term illnesses, making these instruments indispensable elements in contemporary medical procedures.

Restraints:

The market is hampered in large part by the high cost of purchasing and maintaining powered surgical instruments. Healthcare facilities face financial difficulties due to the upfront costs associated with acquiring these cutting-edge devices as well as continuing maintenance and upgrade costs. This cost issue may prevent powered surgical instruments from being widely used, especially in areas with limited funding for healthcare, which would impede market expansion. Cost concerns must be addressed by manufacturers and stakeholders in order to guarantee greater accessibility and uptake of these instruments in a variety of healthcare settings.

Strict approval procedures and regulations are two more important barriers to the market for powered surgical tools. To enter the market, a company must adhere to strict regulatory frameworks and obtain approvals from health authorities like the European Medicines Agency (EMA) and the U.S. Food and Drug Administration (FDA). These lengthy and intricate regulatory procedures can hinder new entrants, postpone product launches, and raise development costs. The amount of money needed to invest in quality assurance and regulatory affairs to get past these regulatory obstacles will affect how quickly new tools can be released onto the market.

Opportunities:

A significant opportunity for powered surgical instruments is presented by the expanding acceptance of telemedicine and the possibility of remote surgery. By combining these instruments with teleoperated robotic systems, surgeons can conduct operations remotely, increasing access to highly skilled surgical care. This is especially important in circumstances where it is difficult to be physically present, like in underserved or rural areas. By creating instruments that work with remote surgical setups, manufacturers can take advantage of this chance to further telemedicine and increase access to healthcare worldwide.

Segment Overview

The power source segment in the global powered surgical tools market is delineated into three categories, each catering to diverse surgical needs. Electric Instruments harness electrical power for consistent and controlled surgical actions, providing surgeons with precision and reliability. Battery-Powered Instruments offer mobility and flexibility by relying on rechargeable batteries, enabling surgeons to navigate procedures with enhanced manoeuvrability. Pneumatic Instruments, powered by compressed air, excel in situations where electrical power may be impractical or unavailable, offering efficient and reliable surgical tools. This segment reflects the industry's commitment to providing a range of power sources to meet the varied demands of surgical procedures.

Within the Product segment, the global powered surgical tools market encompasses three vital components. Handpieces, serving as the handheld interface, play a pivotal role in surgeon control, offering ergonomic design and adaptability. Power Sources and Controls, central units regulating power and instrument operation, incorporate advanced features to enhance surgical precision and safety. Accessories, comprising supplementary components, contribute to the versatility of powered surgical tools, allowing customization based on procedural requirements. This segment underscores the holistic approach taken by the industry to address the multifaceted needs of surgeons and optimize surgical outcomes.

The application segment categorizes powered surgical tools based on the medical specialties they serve. Orthopedic Surgery tools address musculoskeletal conditions, providing solutions for fractures and joint disorders. Oral and Maxillofacial Surgery tools cater to procedures involving the mouth, jaw, and facial structures, including dental and reconstructive surgeries. Neurosurgery tools excel in delicate procedures related to the brain and spine.

ENT Surgery tools focus on Ear, Nose, and Throat procedures, while Cardiothoracic Surgery instruments are tailored for interventions involving the heart and thoracic organs. Plastic and Reconstructive Surgery tools round out the segment, addressing cosmetic and reconstructive procedures. This diverse array of applications demonstrates the industry's commitment to supporting surgeons across a spectrum of medical disciplines, contributing to advancements in specialized surgical care.

Powered Surgical Tools Overview by Region

North America holds a substantial market share, driven by a well-established healthcare system, high awareness levels, and a growing demand for minimally invasive surgeries. The region benefits from significant investments in research and development, fostering technological advancements in powered surgical tools. Europe follows closely, with a strong emphasis on innovation, particularly in countries with advanced healthcare infrastructure. The presence of key market players and a rising geriatric population contributing to the demand for surgical interventions further bolster the market in this region.

The Asia-Pacific region presents a significant opportunity for expansion, driven by factors such as rising healthcare expenditures, enhanced infrastructure, and an increase in chronic illnesses requiring surgical procedures. A growing middle class and increased access to healthcare services are fuelling a surge in demand for powered surgical instruments in countries like China and India. While at a slightly slower pace, market growth is also being observed in Latin America and the Middle East & Africa regions. In these areas, initiatives to improve healthcare accessibility, increased healthcare spending, and a slow transition to more sophisticated surgical methods all have an impact on market expansion.

Powered Surgical Tools Market Competitive Landscape

Key industry participants such as Stryker Corporation, Johnson & Johnson, and Medtronic dominate the market with extensive product portfolios spanning electric, battery-powered, and pneumatic instruments. These companies invest significantly in research and development to introduce cutting-edge technologies, ensuring a competitive edge. Strategic partnerships, mergers, and acquisitions are commonplace, allowing players to broaden their market reach, diversify product offerings, and leverage complementary strengths.

Emerging players, such as MicroAire Surgical Instruments and DePuy Synthes, are gaining prominence by focusing on niche segments and introducing innovative solutions. The market also sees the entry of startups and smaller firms, contributing to the overall competitive dynamics by introducing specialized products and driving innovation. With a growing emphasis on sustainability, companies are incorporating eco-friendly materials and energy-efficient technologies in their product development, aligning with global trends and meeting the rising demand for environmentally conscious solutions.

Powered Surgical Tools Market Leading Companies:

Powered Surgical Tools Recent Developments

Global Powered Surgical Tools Report Segmentation

|

ATTRIBUTE |

DETAILS |

|

By Power Source |

|

|

By Product |

|

|

By Application |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.

+1 812 506 4440

+1 812 506 4440

+91 7875074426

+91 7875074426