Global Portable Medical Devices Market Report: By Product (Diagnostic Imaging, Therapeutics, Monitoring Devices, and Smart Wearable Medical Devices) By Application (Cardiology, Urology, Gynecology, Gastrointestinal, Neurology, Respiratory, Orthopedics and Others), and Region (North America, Europe, Asia-Pacific, Latin America, Middle-East and Africa) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2023-2031.

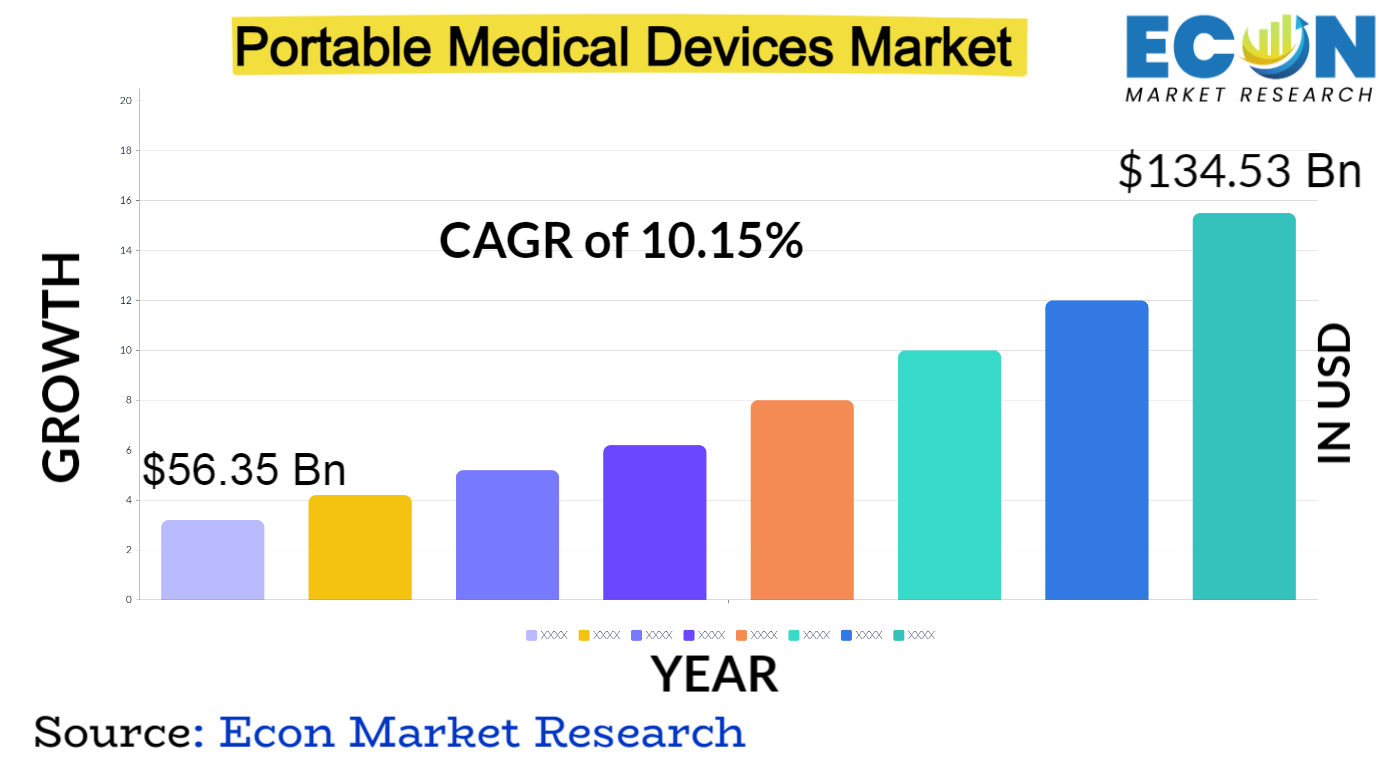

Global Portable Medical Devices market is predicted to reach approximately USD 134.53 billion by 2031, at a CAGR of 10.15% from 2022 to 2031.

A wide variety of small, lightweight medical devices with easy portability that offer therapeutic, monitoring, and diagnostic options are included in the global portable medical devices category. The mobility that portable medical devices provide allows medical professionals to provide care in areas that are remote or underserved, going beyond traditional clinical settings. These gadgets consist of, but are not restricted to, portable X-ray machines, blood glucose metres, handheld ECG monitors, and portable ultrasound devices. The global trend towards personalised and home healthcare, the rise in chronic disease prevalence, and the growing demand for point-of-care diagnostics are driving the growth of this market.

Patients are empowered to actively participate in their own healthcare management thanks to the versatility of portable medical devices, which can address a wide range of healthcare needs. Portable medical devices are defined as those that are lightweight, small, and user-friendly, making it possible to provide effective healthcare in a variety of environments. Technological developments like wireless connectivity, miniaturisation, and longer battery life also support the market's growth. Furthermore, the COVID-19 pandemic has highlighted the significance of portable diagnostic instruments for quick and dispersed testing.

Global Portable Medical Devices report scope and segmentation.

|

Report Attribute |

Details |

|

Estimated Market Value (2022) |

USD 56.35 billion |

|

Projected Market Value (2031) |

USD 134.53 billion |

|

Base Year |

2022 |

|

Forecast Years |

2023 – 2031 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- Based on by Product, by application & Region. |

|

Segments Covered |

By Product, by application & By Region. |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2023 to 2031. |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others. |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Global Portable Medical Devices dynamics

The market dynamics for portable medical devices are defined by a combination of factors driving its expansion. One of the main causes is the rise in chronic illness prevalence, which calls for effective and easily available monitoring and diagnostic tools. The need for remote patient monitoring and point-of-care testing has increased, highlighting the role that portable medical devices play in providing prompt healthcare interventions. Furthermore, technological developments like miniaturisation, connectivity, and data analytics support the growth of more complex and user-friendly devices by enhancing market dynamism.

The COVID-19 pandemic has accelerated the adoption of portable medical devices, with a heightened focus on decentralized healthcare delivery. The pandemic underscored the importance of rapid and portable diagnostics for efficient disease management and containment. Telemedicine and remote patient monitoring, facilitated by portable devices, have become integral components of modern healthcare systems, further driving market growth. Regulatory initiatives and supportive policies also play a crucial role, encouraging the approval and adoption of portable medical devices.

Global Portable Medical Devices drivers

The market for portable medical devices is largely driven by the rising prevalence of chronic illnesses like diabetes, cardiovascular disease, and respiratory disorders throughout the world. The need for prompt and effective diagnostic and monitoring solutions is being driven by the rising incidence of these conditions, which in turn is driving up demand for portable medical devices. These tools improve patient outcomes and healthcare efficiency by empowering patients and healthcare providers to effectively manage chronic conditions outside of traditional clinical settings.

The rapid pace of technological advancements and continuous innovation in the healthcare sector significantly propel the Portable Medical Devices market. Miniaturization, wireless connectivity, and enhanced sensor technologies have led to the development of more sophisticated and user-friendly devices. These technological breakthroughs not only improve the portability and ease of use of medical devices but also enable real-time data transmission, fostering the growth of telemedicine and remote patient monitoring. As a result, the market experiences a surge in demand for cutting-edge portable medical solutions, driven by the potential for better patient care and streamlined healthcare workflows.

Restraints:

The market for portable medical devices is facing difficulties related to regulatory approvals and compliance, even with the growing demand for these devices. Tight regulatory procedures may cause delays in new product introductions and market entry, which may have an impact on the growth trajectory as a whole. Market participants are constrained by the need to make large investments to ensure compliance with a variety of standards and requirements when navigating the diverse regulatory landscapes across regions.

The increasing reliance on portable medical devices for data collection and transmission raises significant concerns regarding data security and privacy. As these devices often handle sensitive patient information, the potential for unauthorized access and data breaches is a critical restraint. Addressing these concerns is paramount to gaining and maintaining the trust of healthcare providers and patients, necessitating robust cybersecurity measures and adherence to strict data protection regulations.

Opportunities:

The growing trend towards home healthcare presents a significant opportunity for the Portable Medical Devices market. As healthcare delivery shifts from traditional settings to patients' homes, portable devices play a pivotal role in enabling remote monitoring and diagnostics. The expansion of home healthcare services, coupled with advancements in wearable technologies, opens new avenues for portable medical devices to enhance patient care and promote proactive health management.

Segment Overview

The portable medical devices market boasts a comprehensive array of product types designed to meet diverse healthcare needs. Diagnostic imaging products, such as portable ultrasound machines and handheld X-ray devices, empower healthcare professionals with on-the-go imaging capabilities, facilitating rapid point-of-care diagnostics. Therapeutic devices, including portable nebulizers and wearable insulin pumps, enable patients to receive essential treatments outside traditional healthcare settings. Monitoring Devices, ranging from portable ECG monitors to blood pressure and glucose meters, offer continuous health monitoring, aiding in early detection and proactive management. The innovative Smart Wearable Medical Devices segment, featuring health-monitoring smartwatches, aligns technology with healthcare, providing real-time data tracking and personalized feedback.

The segmentation of portable medical devices by application caters to various medical specialties and healthcare domains. In Cardiology, portable ECG monitors and ambulatory blood pressure devices contribute to the diagnosis and monitoring of cardiovascular conditions. Urology applications utilize portable ultrasound scanners and uroflowmetry devices for assessing and managing urinary system disorders. Gynecology benefits from portable ultrasound devices for obstetric imaging and handheld colposcopes for cervical examinations. In Gastrointestinal care, portable endoscopy devices and ultrasound tools aid in diagnosing and monitoring digestive system disorders. Neurology applications involve portable EEG monitors and neuroimaging devices for the diagnosis and monitoring of neurological conditions. Respiratory devices, such as portable spirometers and nebulizers, assist in monitoring and managing respiratory health. Orthopedics benefit from portable X-ray machines and ultrasound devices for musculoskeletal imaging.

Global Portable Medical Devices Overview by Region

North America stands as a significant player, attributed to its advanced healthcare systems, substantial investment in research and development, and a proactive approach to adopting innovative medical technologies. The region benefits from a strong presence of key market players, fostering a competitive environment. Europe follows suit, leveraging well-established healthcare infrastructure and a growing focus on personalized medicine. The Asia-Pacific region emerges as a hotbed for market growth, fuelled by increasing healthcare expenditure, a large population base, and a rising prevalence of chronic diseases. Countries like China and India are particularly pivotal, witnessing a surge in demand for portable medical devices due to improving healthcare accessibility and a shift towards decentralized healthcare delivery.

Latin America and the Middle East & Africa exhibit untapped potential, with a growing awareness of the benefits of portable medical devices and increasing investments in healthcare infrastructure. However, these regions face challenges related to economic constraints and varying levels of healthcare development. The COVID-19 pandemic has further accelerated the adoption of portable medical devices globally, with an emphasis on rapid and decentralized diagnostics. Regulatory frameworks, reimbursement policies, and cultural factors also play a significant role in shaping regional market dynamics.

Global Portable Medical Devices market competitive landscape

The competitive landscape of the portable medical devices market is characterized by intense competition among key players striving for market dominance through innovation, strategic collaborations, and geographic expansion. North America is home to major players such as General Electric Company, Medtronic plc, and Abbott Laboratories, leveraging their strong presence and substantial R&D investments to introduce cutting-edge portable medical solutions. In Europe, companies like Siemens Healthineers and Philips Healthcare contribute significantly to the competitive environment, capitalizing on well-established healthcare infrastructure and a focus on personalized medicine. The Asia-Pacific region witnesses a surge in competition with notable players including Mindray Medical International Limited and Omron Corporation, responding to the region's rising healthcare expenditure and the increasing demand for portable devices, especially in countries like China and India.

Latin America and the Middle East & Africa represent emerging markets, attracting attention from global players such as F. Hoffmann-La Roche Ltd and Johnson & Johnson, as these regions experience a growing awareness of portable medical devices' benefits. However, smaller regional players are also entering the fray, contributing to market diversity and competition. The COVID-19 pandemic has accelerated strategic partnerships and collaborations, exemplified by companies like BD (Becton, Dickinson and Company) and bioMérieux SA, who joined forces to develop rapid diagnostic solutions. Regulatory compliance and adherence to quality standards are pivotal in this competitive landscape, with companies constantly navigating diverse global regulatory frameworks to ensure market access.

Global Portable Medical Devices Recent Developments

Scope of global Portable Medical Devices report

Global Portable Medical Devices report segmentation

|

ATTRIBUTE |

DETAILS |

|

By Product |

|

|

By Application |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Objectives of the Study

The objectives of the study are summarized in 5 stages. They are as mentioned below:

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.