Global Medical Device Connectivity Market Research Report: By Product and Service (Medical Device Connectivity Solutions, Medical Device Connectivity Services), By Technology (Wired Technologies, Wireless Technologies, Hybrid Technologies), By Application (Vital signs and patient monitors, Anesthesia machines and Ventilators, Infusion pumps, Others), By End User (Hospitals, Home Healthcare Centers, Diagnostic Centers, Ambulatory Care Centers), and Region (North America, Europe, Asia-Pacific, and Rest of the World) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2024-2032.

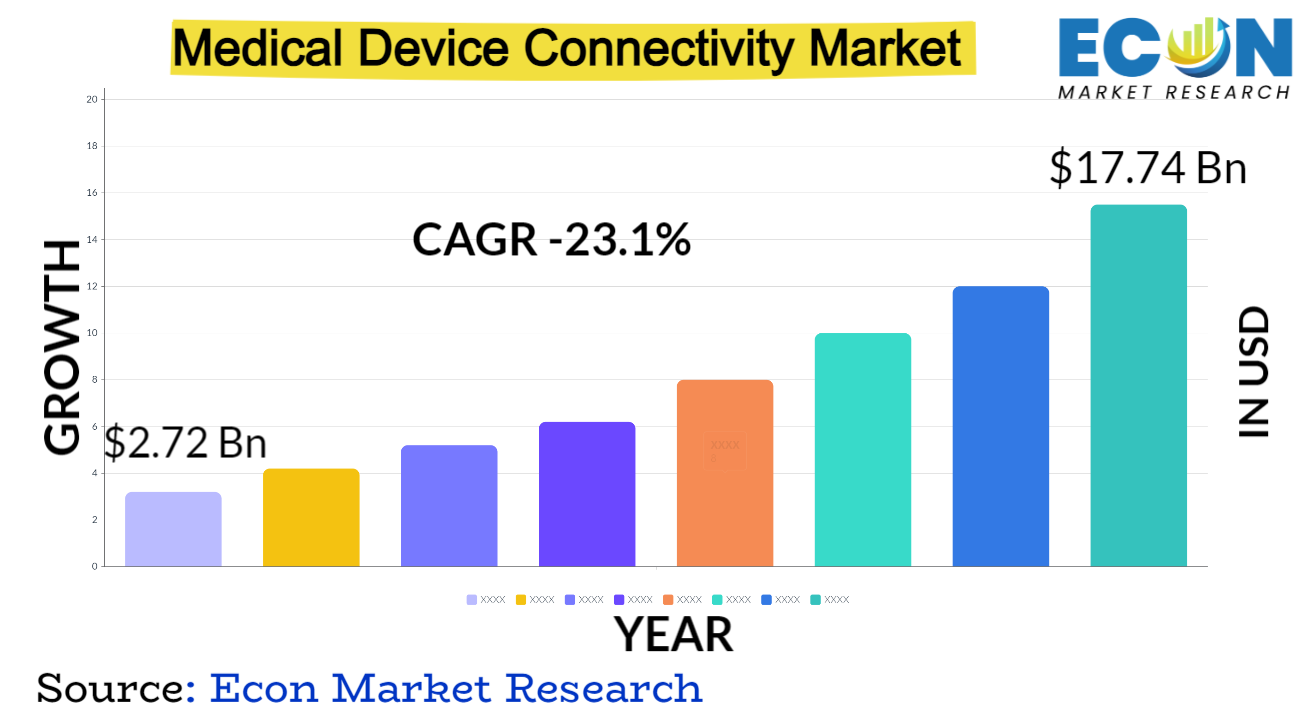

The global medical device connectivity market was valued at USD 2.72 billion in 2023 and is estimated to reach approximately USD 17.74 billion by 2032, at a CAGR of 23.1% from 2024 to 2032.

The market for medical device connection has expanded quickly, transforming healthcare through the integration of diverse medical devices and systems to improve patient care and expedite data sharing. Connecting various medical equipment, including infusion pumps, ventilators, and patient monitors, to centralized information systems like hospital networks and electronic health records (EHRs) is the main goal of this rapidly expanding industry. Healthcare workers can make faster decisions and provide more individualized treatment by having real-time access to vital patient information through seamless communication and data interchange. The growing need for better patient outcomes, more effective healthcare delivery, and a rise in the use of digital health solutions are driving the market's expansion.Innovation in this field is also being fueled by technical developments such as cloud-based platforms, IoT-enabled devices, and interoperability standards. The medical device connectivity market has the potential to significantly alter and improve the healthcare environment as healthcare systems throughout the globe aim for more interoperability and connectivity.

MEDICAL DEVICE CONNECTIVITY MARKET: REPORT SCOPE & SEGMENTATION

|

Report Attribute |

Details |

|

Estimated Market Value (2023) |

2.72 Bn |

|

Projected Market Value (2032) |

17.74 Bn |

|

Base Year |

2023 |

|

Forecast Years |

2024 - 2032 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- By Product and Service, By Technology, By Application, By End User, & Region |

|

Segments Covered |

By Product and Service, By Technology, By Application, By End User, & Region |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2024 to 2032 |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, and the Rest of World |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis, and COVID-19 impact analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Global Medical Device Connectivity Market Dynamics

The dynamic forces inherent in increasing healthcare requirements, regulatory frameworks, and technological breakthroughs define the medical device connectivity market. The ongoing development of technology, shown by the incorporation of cloud computing, artificial intelligence (AI), and the Internet of Things (IoT) into medical devices, is one important factor. These developments improve patient care by boosting connectivity and facilitating easy data sharing and remote monitoring. The increasing focus on interoperability standards, which promotes the integration of various systems and devices across healthcare environments, is another important driver. Additionally, the market is being pushed by the growing desire to improve clinical decision-making and patient outcomes while lowering healthcare costs, which is driving demand for streamlined workflows and effective data management. The market dynamics are also greatly impacted by regulatory changes and compliance requirements, as healthcare institutions endeavor to adhere to strict data security and privacy regulations. Growth in the market is further accelerated by the rising incidence of chronic illnesses as well as the development of telehealth and remote patient monitoring. All things considered, these interrelated dynamics highlight a quickly changing environment in which healthcare demands, innovation, and legal compliance come together to influence the direction of the medical device connection market.

Global Medical Device Connectivity Market Drivers

Global aging populations have raised healthcare demands, which has put pressure on healthcare delivery systems to be optimized. There are now higher expectations for more connected and data-driven healthcare experiences due to technological improvements, especially in the areas of medical devices and digital health solutions. In order to facilitate real-time monitoring, analysis, and decision-making, patients and healthcare professionals alike need seamless integration between devices, electronic health records, and healthcare networks. Furthermore, the COVID-19 pandemic has expedited the implementation of remote monitoring and telemedicine, underscoring the need for resilient connectivity solutions to provide uninterrupted patient care. This increased demand is a reflection of a move away from reactive and preventative healthcare models. These models rely on simplified connection to enhance patient outcomes, treatments, and diagnostics while cutting costs and inefficiencies in healthcare systems.

The development of advanced, portable medical equipment with continuous data gathering and transmission capabilities has been made possible by technological advancements. This technical advancement promotes proactive rather than reactive care approaches by enabling healthcare personnel to remotely monitor patients' vital signs, chronic illnesses, and post-treatment progress in real-time. The aging population and rising incidence of chronic illnesses are two other important factors that are driving the healthcare industry to look for cutting-edge approaches to long-term condition management. RPM provides a way to improve patient autonomy and engagement by letting people take an active role in their care while still being comfortable in their own homes. Furthermore, the COVID-19 pandemic emphasized the need for scalable and dependable remote monitoring systems and hastened the acceptance and use of telehealth and RPM as respectable substitutes for in-person consultations. The emphasis on RPM as a crucial element of contemporary, patient-centered care paradigms keeps growing as healthcare systems throughout the world strive for cost-effectiveness and better patient outcomes.

Restraints:

Healthcare systems are particularly vulnerable to cyberattacks because of their interconnectedness. The wide variety of devices that frequently run on several protocols and security standards presents a major challenge since it leads to inconsistencies that hackers can take advantage of. Healthcare organizations often use legacy systems, which can not have strong security safeguards in place, making them more vulnerable to hacking. The risk is further increased by the enormous amount of private patient data that is integrated into electronic health records and transferred between devices. Healthcare institutions have to constantly adapt to combat sophisticated cyber threats while navigating strict regulatory compliance requirements, which makes system maintenance more difficult and expensive. Strict encryption and authentication procedures are required due to privacy concerns regarding patient data, especially when it is being transferred between devices and databases. It is difficult to strike a balance between strict security rules and healthcare practitioners' accessibility, as the latter may obstruct prompt access to vital patient data. It is necessary to continuously invest in cybersecurity infrastructure, upgrade device security, train staff on cybersecurity best practices, and adhere to strict regulatory frameworks in order to mitigate these risks. This is a complex task that calls for constant attention and resources.

It is difficult and time-consuming to integrate various devices with different software systems and communication protocols. Modern technologies and historical systems sometimes have compatibility problems that call for careful preparation and frequently major overhauls or infrastructure investments. The wide variety of devices, each with distinct features and data formats, makes it more difficult to exchange and evaluate information across platforms in an efficient manner. Implementation is made more difficult by the workforce's inherent complexity, which calls for extensive training programs for healthcare workers to enable them to navigate complex networks with ease. The provision of patient care and operational effectiveness may be hampered by workflow disruptions that occur during the integration process, including downtime for system updates and modifications. Furthermore, maintaining patient privacy and security throughout the network's interconnections makes implementation even more difficult and necessitates strict safeguards that could make integration even more complex. To surmount these intricacies, one needs to employ a combination of strategic planning, strong interoperability standards, stakeholder participation, continuous staff training, and a phased deployment approach that minimizes interruptions and facilitates a seamless shift to interconnected healthcare ecosystems.

Opportunities:

Wearables and IoT-enabled devices have a significant opportunity to transform patient care through data-driven insights, tailored health management, and continuous monitoring. Wearable health gadgets, such fitness trackers, smartwatches, and specialist medical wearables, let users monitor their activity levels, vital health parameters, and even spot abnormalities in real time. These gadgets make it easier for data to flow smoothly, giving medical practitioners access to continuous, detailed patient data. Furthermore, by facilitating early health issue diagnosis and encouraging proactive actions, the incorporation of smart devices into healthcare ecosystems improves preventative care. By establishing interconnected networks where various devices may communicate, share data, and contribute to a comprehensive picture of an individual's health, IoT technologies enhance this potential.To fully capitalize on this opportunity, wearables must be integrated into remote monitoring programs, advanced analytics must be used to extract meaningful insights, and IoT must be leveraged to create complex healthcare ecosystems. In addition to empowering people to take control of their health, the confluence of wearables and IoT is revolutionizing healthcare delivery by enabling more proactive, individualized, and data-driven approaches to patient care.

From a variety of sources, including wearable technology, genetic data, medical imaging, electronic health records (EHRs), and more, big data analytics have the ability to extract priceless insights. By examining this abundance of data, patterns, trends, and correlations can be found that help with disease knowledge, outcome prediction, and the creation of individualized treatment regimens. Furthermore, by spotting trends in public health and enhancing preventive care tactics, big data facilitates population health management. Big data's potential is further enhanced by integrating artificial intelligence (AI) and machine learning algorithms with it. This allows for predictive analytics for early disease detection, optimal resource allocation, and improved decision-making processes. In addition to improving clinical care and patient outcomes, the capacity to extract meaningful insights from big data stimulates innovation and research, leading to the creation of new treatments and interventions. To fully realize the transformational promise of big data analytics, healthcare providers, academics, and data scientists must collaborate to ensure strong data governance, interoperability, and privacy safeguards.

Segment Overview

By Product and Service

Based on product and service, the global medical device connectivity market is divided into medical device connectivity solutions, medical device connectivity services. The medical device connectivity solutions category dominates the market with the largest revenue share in 2023. These are technological platforms, software, and systems designed to enable seamless communication and data exchange among various medical devices. These solutions typically involve hardware components, software interfaces, and protocols that facilitate connectivity. They allow medical devices such as patient monitors, infusion pumps, ventilators, and other equipment to communicate with each other and with broader healthcare information systems, such as electronic health records (EHRs) or hospital networks. Medical device connectivity services complement the connectivity solutions by providing support, implementation, maintenance, and consulting expertise to healthcare providers and institutions. Medical device connectivity services encompass a range of offerings, including installation of connectivity solutions, integration with existing systems, troubleshooting, training for healthcare staff, and ongoing technical support.

By Technology

Based on the technology, the global medical device connectivity market is categorized into wired technologies, wireless technologies, hybrid technologies. The wireless technologies category leads the global medical device connectivity market with the largest revenue share in 2023. Wireless connectivity eliminates the need for physical cables, enabling communication between devices via wireless networks. This category includes various wireless protocols such as Wi-Fi, Bluetooth, Zigbee, and cellular networks. Wireless technologies provide flexibility, mobility, and easier scalability compared to wired connections. They are particularly valuable in settings where mobility and real-time data access are essential, allowing healthcare providers to monitor patients remotely and access data from different locations within a healthcare facility. Wired connectivity involves physical connections through cables or wired networks. This method ensures stable and secure connections between medical devices and information systems. It often utilizes ethernet cables, USB connections, or serial ports to establish direct and reliable communication. Wired technologies offer consistent data transmission rates and are generally perceived to be more secure compared to wireless alternatives. Hybrid connectivity combines elements of both wired and wireless approaches to optimize connectivity. It involves a mix of wired and wireless connections to leverage the advantages of both. For instance, critical components might be hardwired for reliability, while less critical devices utilize wireless connections for flexibility. Hybrid technologies aim to achieve a balance between reliability, security, and flexibility, catering to diverse healthcare settings with varying connectivity requirements.

By Application

Based on application, the global medical device connectivity market is segmented into vital signs and patient monitors, anesthesia machines and ventilators, infusion pumps, others. The vital signs and patient monitors segment dominates the medical device connectivity market. This category includes devices used for monitoring crucial patient parameters such as heart rate, blood pressure, temperature, and oxygen saturation. Vital signs monitors and patient monitors gather real-time data, enabling healthcare providers to track a patient's condition continuously. Connectivity solutions allow this data to be transmitted to electronic health records (EHRs) or central monitoring systems, facilitating remote monitoring and quick access to critical patient information. Anesthesia machines and ventilators, these devices are essential in surgical and critical care settings. Anesthesia machines manage a patient's anesthesia dosage during surgery, while ventilators assist patients with breathing difficulties. Connectivity solutions integrated with these machines enable healthcare providers to monitor and regulate parameters remotely, ensuring precise control and immediate response to changes in a patient's condition. Infusion pumps deliver fluids, medications, or nutrients to patients in a controlled manner. Connected infusion pumps can transmit data about infusion rates, medication dosages, and alerts in case of any anomalies. Integration with broader systems allows for automated documentation of medication administration and ensures accurate and safe delivery of treatments.

By End User

Based on end user, the global medical device connectivity market is divided into hospitals, home healthcare centers, diagnostic centers, ambulatory care centers. The hospitals solutions category dominates the market with the largest revenue share in 2023. Hospitals represent the primary segment for medical device connectivity. Within hospital settings, connected medical devices play a pivotal role in various departments such as intensive care units (ICUs), operating rooms, emergency departments, and general wards. Connectivity solutions in hospitals facilitate real-time data transmission from medical devices to centralized systems like electronic health records (EHRs) or hospital information systems (HIS), allowing healthcare professionals immediate access to patient information for timely interventions and comprehensive care coordination. With the rise of home-based care, connected medical devices are increasingly used in home healthcare settings. These devices enable remote monitoring of patients, allowing healthcare providers to track vital signs, medication adherence, and other parameters from a distance. This connectivity fosters greater independence for patients while ensuring continuous monitoring and timely interventions when necessary. Diagnostic centers utilize connected medical devices for various diagnostic purposes such as imaging (like MRI, CT scans), laboratory testing (blood analyzers, diagnostic equipment), and other diagnostic procedures. Connectivity solutions aid in the seamless transmission of diagnostic results to healthcare providers and enable integration with patient records for comprehensive diagnostic analysis. Ambulatory care centers, including clinics, urgent care facilities, and outpatient centers, also benefit from medical device connectivity. Connected devices in these settings help streamline workflows, enhance patient care, and improve efficiency in delivering healthcare services. For instance, connectivity allows for immediate access to patient histories, test results, and treatment plans, optimizing the care provided during short-term visits.

Global Medical Device Connectivity Market Overview by Region

The global medical device connectivity market is categorized into North America, Europe, Asia-Pacific, and the Rest of the World. North America emerged as the leading region, capturing the largest market share in 2023. The area leads the way in healthcare technology innovation and has a strong technological infrastructure. North America is a leader in the development and uptake of cutting-edge medical device connectivity solutions due to its concentration of top IT firms and healthcare facilities. The implementation of linked medical devices is made possible by the region's well-established healthcare systems and high rate of acceptance of digital health solutions. North American clinics, hospitals, and other healthcare organizations are eager to implement these technologies in order to improve patient care and operational effectiveness. The strict yet encouraging regulatory frameworks in North America encourage the use of standardized connectivity protocols and protect patient privacy and data security. Adherence to laws like the Health Insurance Portability and Accountability Act (HIPAA) encourages the use of secure networking solutions. The continual advancement and acceptance of medical device connectivity technologies are facilitated by significant financial support for research and development, as well as substantial investments in healthcare IT and digital health efforts. Numerous major participants in the industry are based in the region, which encourages partnerships and collaborations between technology businesses, healthcare providers, and device manufacturers. These partnerships foster creativity and make it easier to create integrated, interoperable solutions.

Global Medical Device Connectivity Market Competitive Landscape

In the global medical device connectivity market, a few major players exert significant market dominance and have established a strong regional presence. These leading companies remain committed to continuous research and development endeavors and actively engage in strategic growth initiatives, including product development, launches, joint ventures, and partnerships. By pursuing these strategies, these companies aim to strengthen their market position, expand their customer base, and capture a substantial share of the market.

Some of the prominent players in the global medical device connectivity market include Cerner Corporation, Medtronic, Masimo, Koninklijke Philips N.V., General Electric, Stryker, iHealth Labs Inc., Cisco Systems, Inc, Lantronix Inc., Infosys Limited, Silicon & Software Systems Ltd., Hill-Rom Services Inc, Silex Technology America, Inc, Digi International Inc, Baxter, TE Connectivity, Bridge-Tech, and MediCollector, and various other key players.

Global Medical Device Connectivity Market Recent Developments

In January 2021, The $2.8 billion deal to acquire BioTelemetry, a remote cardiac care company, has been finalized by health tech giant Royal Philips. The company also revealed plans to acquire Capsule Technologies for a $635 million cash consideration.

Scope of the Global Medical Device Connectivity Market Report

Medical Device Connectivity Market Report Segmentation

|

ATTRIBUTE |

DETAILS |

|

By Product and Service |

|

|

By Technology |

|

|

By Application |

|

|

By End User |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Objectives of the Study

The objectives of the study are summarized in 5 stages. They are as mentioned below:

To identify and estimate the market size for the global medical device connectivity market segmented by product and service, by technology, by application, by end user, region and by value (in U.S. dollars). Also, to understand the consumption/ demand created by consumers of medical device connectivity between 2019 and 2032.

To identify and infer the drivers, restraints, opportunities, and challenges for the global medical device connectivity market

To find out the factors which are affecting the sales of medical device connectivity among consumers

To identify and understand the various factors involved in the global medical device connectivity market affected by the pandemic

To provide a detailed insight into the major companies operating in the market. The profiling will include the financial health of the company's past 2-3 years with segmental and regional revenue breakup, product offering, recent developments, SWOT analysis, and key strategies.

Intended Audience

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.