Global Blood Group Typing Market Report: By Product (Instruments, Consumables, and Services), Technique (PCR-based and Microarray, Assay-based, Massively Parallel Sequencing, and Other), Test type (Antibody Screening, HLA Typing, Cross-matching Tests, ABO blood Tests and Other) End-user (Hospitals, Blood Banks and Others), and Region (North America, Europe, Asia-Pacific, Latin America, Middle-East and Africa) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2024-2032.

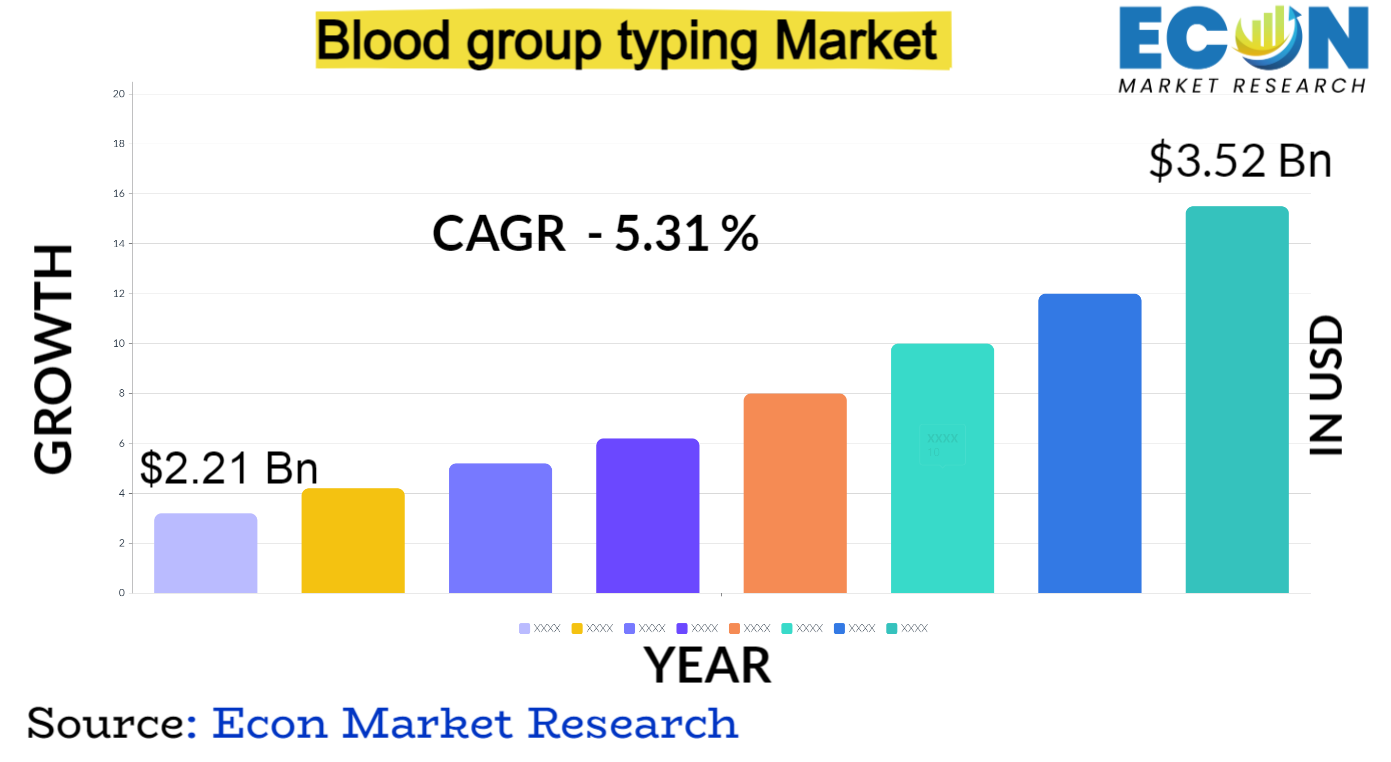

Global Blood group typing market is predicted to reach approximately USD 3.52 billion by 2032, at a CAGR of 5.31% from 2024 to 2032.

Blood group typing, sometimes referred to as blood grouping or blood typing, is an essential diagnostic process that establishes a person's blood type and Rh factor. For a number of medical procedures, such as organ transplants, blood transfusions, and prenatal care, this classification is essential. The market includes a broad range of methods and goods intended to reliably and quickly identify blood types, including RhD and ABO, as well as extra subtyping for more thorough compatibility evaluations.

Global Blood group typing report scope and segmentation.

|

Report Attribute |

Details |

|

Estimated Market Value (2023) |

USD 2.21 billion |

|

Projected Market Value (2032) |

USD 3.52 billion |

|

Base Year |

2023 |

|

Forecast Years |

2024 – 2032 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- Based on By Product, Technique, Test type, End-User & Region. |

|

Segments Covered |

By Product, Technique, Test type, End-User & By Region. |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2023 to 2032. |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others. |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Global Blood group typing dynamics

Increasing demand for blood transfusions, driven by a rising incidence of surgeries, trauma cases, and chronic diseases, is a key driver fuelling market expansion. The significance of blood group typing in modern healthcare practices is further underscored by its crucial role in guaranteeing safe and compatible organ transplants and transfusions. Furthermore, there is a growing awareness in the market about the significance of precise blood group identification for routine medical care, prenatal testing, and personalised medicine applications, in addition to emergency scenarios.

The dynamics of the market are significantly shaped by technological developments, with continuous improvements in automation and molecular techniques improving the speed, accuracy, and efficiency of blood typing procedures. Healthcare workers can now perform high-throughput blood group typing, which streamlines clinical workflows and cuts down on turnaround times, thanks to the integration of advanced technologies. Increased research and development efforts aimed at broadening the spectrum of blood typing techniques and taking into account the subtleties of varied populations also benefit the market.

Global Blood group typing drivers

The global prevalence of chronic illnesses, surgical procedures, and trauma cases, among other factors, are major factors driving the blood group typing market. Blood transfusions are frequently required after surgical procedures, which has increased demand for precise blood group identification in order to guarantee safe and appropriate transfusions. As healthcare infrastructure advances and access to medical services expands, the market will grow as a result of the growing healthcare needs, especially in emerging economies. This driver highlights the vital role that the market plays in facilitating a range of medical interventions and the significance of blood group typing in the process of making healthcare decisions.

Rapid advancements in blood typing technologies, including molecular techniques and automation, significantly drive market growth. Automation streamlines blood typing processes, reducing turnaround times and enhancing overall efficiency. The integration of molecular methods provides higher precision and expands the capabilities of blood group typing, allowing for more comprehensive compatibility assessments. These technological innovations not only improve the accuracy of results but also contribute to the scalability of blood typing procedures, making them more accessible in various healthcare settings. The continuous evolution of these technologies positions the market at the forefront of diagnostic innovations, reinforcing its relevance in modern healthcare practices.

Restraints:

The high costs associated with advanced blood typing technologies, like automated systems and molecular methods, are impeding their adoption. These technologies can come with hefty initial and ongoing maintenance costs, especially for healthcare facilities in areas with limited resources. This financial barrier prevents advanced blood typing techniques from being widely used, which affects market penetration and makes it more difficult for some healthcare settings to upgrade their blood typing capabilities.

Although the market for blood group typing has room to grow, there are obstacles in emerging economies. These difficulties include a lack of knowledge regarding the significance of blood group typing, a deficiency in the infrastructure of healthcare, and a lack of funding for medical expenses. To overcome these obstacles, focused initiatives are needed to increase awareness, enhance healthcare accessibility, and offer affordable solutions that are suited to the unique requirements of these areas. The uniform advancement of the blood group typing market globally is impeded by the disparities in healthcare development among different economies.

Opportunities:

The growing emphasis on personalized medicine presents a significant opportunity for the blood group typing market. As healthcare practices increasingly focus on tailoring treatments to individual characteristics, accurate blood group identification becomes crucial for personalized therapeutic strategies. This trend opens avenues for the integration of blood group typing into precision medicine approaches, creating opportunities for market players to develop and offer specialized solutions catering to personalized healthcare needs.

Segment Overview

The blood group typing market is segmented by product into instruments, consumables, and services. Instruments encompass the machinery and devices utilized for blood group typing procedures, including automated analyzers and testing platforms. Consumables refer to the disposable components and reagents required for blood typing tests, such as blood grouping reagents and test cards. Services involve the professional expertise and support provided by healthcare institutions or specialized laboratories in conducting blood group typing tests. This segmentation reflects the diverse components and resources involved in delivering accurate and reliable blood typing results.

The market is categorized by technique, encompassing PCR-based and Microarray methods, assay-based techniques, massively parallel sequencing, and other emerging technologies. PCR-based and Microarray techniques utilize polymerase chain reaction and microarray platforms for efficient and high-throughput blood group typing. Assay-based methods involve specific assays for identifying blood group antigens. Massively Parallel Sequencing leverages advanced sequencing technologies for comprehensive and detailed blood group analysis. The "other" category encompasses innovative techniques contributing to the continuous evolution of blood group typing methodologies. This segmentation highlights the diverse technological approaches employed to enhance the precision and efficiency of blood typing processes.

Blood group typing is further classified by test type, including antibody screening, HLA typing, cross-matching tests, ABO blood tests, and other specialized tests. Antibody screening identifies antibodies in the blood that may cause adverse reactions during transfusions. HLA typing determines the compatibility of human leukocyte antigens for organ transplantation. Cross-matching tests assess the compatibility between donor and recipient blood samples. ABO blood tests classify individuals into different blood groups based on the presence or absence of A and B antigens. The "other" category comprises additional specific blood group tests, reflecting the diversity of diagnostic applications within this segment.

The end-user segment encompasses healthcare entities and institutions utilizing blood group typing services, including hospitals, diagnostic laboratories, blood banks, and research institutions. The end-user segmentation reflects the diverse settings where blood group typing is essential for various medical interventions. This includes routine blood typing for healthcare procedures in hospitals, compatibility assessments in blood banks for transfusions, and specialized research applications in research institutions. The diversity in end-users underscores the broad scope and critical role of blood group typing across different facets of the healthcare ecosystem.

Global Blood group typing Overview by Region

In developed regions such as North America and Europe, the market experiences a robust presence due to well-established healthcare systems and a higher adoption rate of advanced blood typing technologies. North America, particularly the United States, holds a significant share, driven by the increasing prevalence of chronic diseases, a sophisticated healthcare infrastructure, and a strong emphasis on technological innovation.

Growing older populations and an increasing need for blood products are driving market growth in Europe, where nations like France, Germany, and the United Kingdom play a major role. Collaborative research and development efforts benefit the region as well, promoting improvements in blood typing techniques. Due to increased healthcare spending, bettering healthcare infrastructure, and growing recognition of the significance of blood group typing, the Asia-Pacific market is growing quickly. Leading the way in this expansion are nations like China and India, where blood typing services are in high demand amidst a changing healthcare environment.

Global Blood group typing market competitive landscape

Major companies such as Bio-Rad Laboratories, Inc., Grifols S.A., Ortho Clinical Diagnostics, Immucor, Inc., and Quotient Limited dominate the market, leveraging their extensive product portfolios and widespread geographic presence. These companies focus on research and development activities to introduce innovative blood typing solutions, including advanced instruments and consumables, enhancing the efficiency and accuracy of blood group identification.

Collaborations, mergers, and acquisitions are prevalent strategies within the competitive landscape as companies seek to expand their market share and strengthen their technological capabilities. For instance, strategic partnerships between diagnostic laboratories and blood banks facilitate the integration of blood group typing services into broader healthcare networks. Moreover, continuous efforts are made by market players to comply with regulatory standards and certifications, ensuring the reliability and safety of their blood typing products.

Global Blood group typing Recent Developments

Scope of global Blood group typing report

Global Blood group typing report segmentation

|

ATTRIBUTE |

DETAILS |

|

By Product |

|

|

By Technique |

|

|

By Test Type |

|

|

By End-user |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Objectives of the Study

The objectives of the study are summarized in 5 stages. They are as mentioned below:

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.