Wind Turbine Rotor Blade Market Report: By Type (Carbon Fiber, Fiberglass), By Location (Onshore, Offshore), and Region (North America, Europe, Asia-Pacific, Latin America, Middle-East and Africa) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2024-2032.

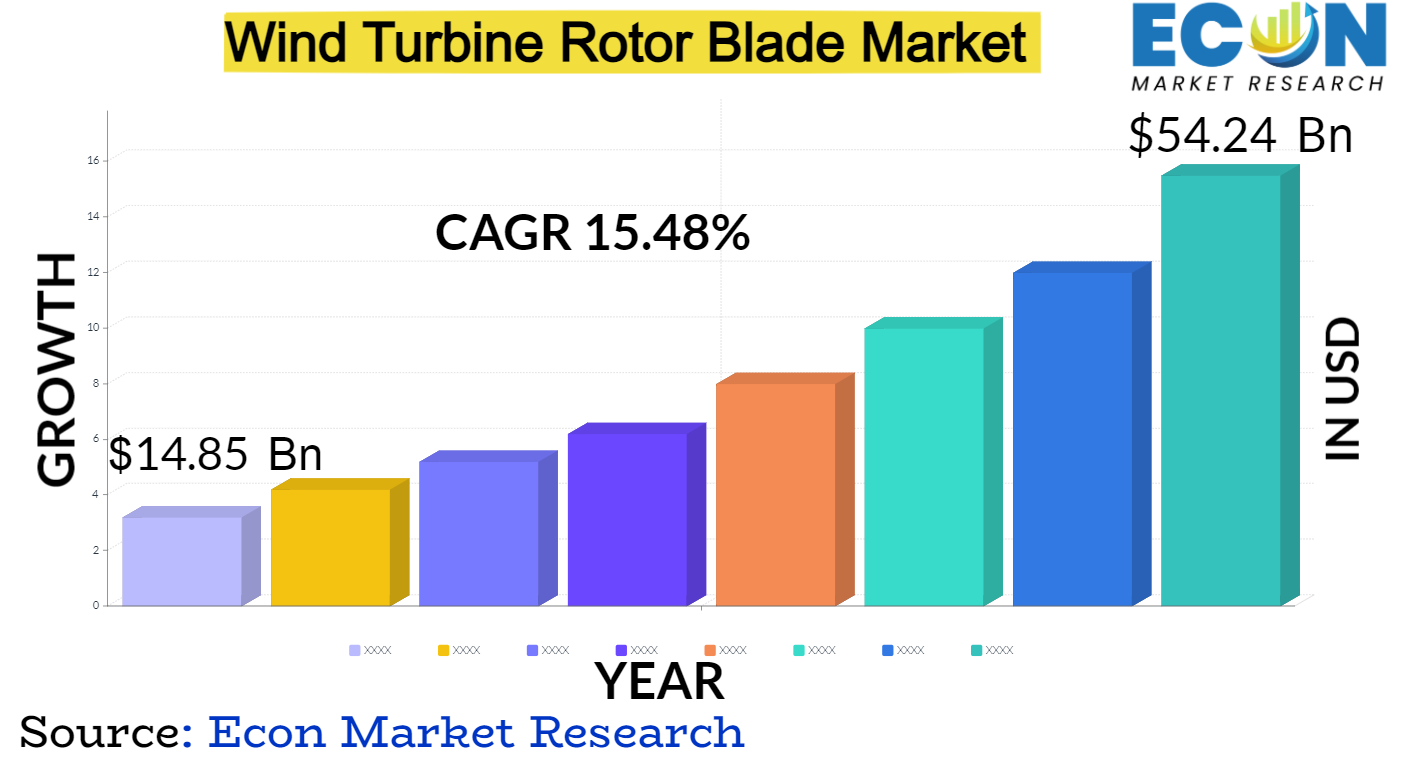

Global Wind Turbine Rotor Blade market is predicted to reach approximately USD 54.24 billion by 2032, at a CAGR of 15.48% from 2024 to 2032.

The Global Wind Turbine Rotor Blade market encompasses the production, distribution, and utilization of rotor blades designed for wind turbines across various geographical regions. These rotor blades are integral components of wind turbines, responsible for capturing wind energy and converting it into rotational mechanical energy to generate electricity. As renewable energy sources gain prominence globally, the demand for efficient, durable, and cost-effective rotor blades continues to surge.

The market is characterized by innovations in blade design, materials, and manufacturing processes aimed at enhancing efficiency, durability, and environmental sustainability. Key market players include industry leaders such as Siemens Gamesa, Vestas, GE Renewable Energy, and Nordex, alongside emerging players contributing to the dynamic landscape of the wind energy sector. Factors driving market growth include increasing investments in renewable energy infrastructure, government initiatives promoting clean energy adoption, and growing environmental awareness among consumers and businesses. Additionally, technological advancements, such as the development of longer blades capable of harnessing wind energy more effectively, are shaping the trajectory of the market.

Global Wind Turbine Rotor Blade Report Scope and Segmentation

|

Report Attribute |

Details |

|

Estimated Market Value (2023) |

USD 14.85 billion |

|

Projected Market Value (2032) |

USD 54.24 billion |

|

Base Year |

2023 |

|

Forecast Years |

2024 – 2032 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- Based on By Type, By Location, & Region. |

|

Segments Covered |

By Type, By Location, & By Region. |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2024 to 2032. |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others. |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Wind Turbine Rotor Blade Dynamics

The evolution of rotor blade designs, materials, and manufacturing processes is driven by technological advancements with the goal of improving cost-effectiveness, durability, and efficiency. Manufacturers continuously invest in R&D as the industry develops in order to maximise blade performance, adjust to changing wind conditions, and lessen environmental effects. Through their effects on investment patterns, project viability, and market competitiveness, government incentives and regulatory policies have a significant impact on market dynamics.

Renewable energy targets, tax credits, and subsidies encourage the use of renewable energy and expand the market. Moreover, evolving regulatory frameworks concerning environmental sustainability, carbon emissions, and renewable energy integration further propel the demand for wind turbine rotor blades. Economic factors such as energy prices, financing costs, and market competition also influence market dynamics. Fluctuations in energy prices, coupled with advancements in renewable energy technologies, impact the competitiveness of wind energy relative to conventional energy sources.

Additionally, market competition among manufacturers drives innovation and cost optimization, resulting in improved product offerings and market differentiation. Environmental considerations, including climate change mitigation and air pollution reduction, increasingly drive the adoption of renewable energy solutions such as wind power. As stakeholders prioritize sustainability goals and environmental stewardship, the demand for wind turbine rotor blades is expected to continue growing, fostering a dynamic and resilient market landscape poised for further expansion and innovation.

Wind Turbine Rotor Blade Drivers

The global push towards renewable energy sources is a significant driver for the wind turbine rotor blade market. Governments worldwide are setting ambitious renewable energy targets to reduce carbon emissions and combat climate change. This transition creates a conducive environment for the adoption of wind energy, thereby increasing the demand for rotor blades. As countries commit to phasing out fossil fuels and invest in clean energy infrastructure, wind power emerges as a key solution due to its scalability, sustainability, and cost-effectiveness.

The efficiency, longevity, and performance of wind turbine rotor blades are continually improved, which propels market expansion. Blade design, material, and manufacturing process innovations allow for the creation of longer, lighter, and more aerodynamic blades that can better harness wind energy. Improved blade designs increase energy output and lower maintenance costs, increasing the competitiveness of wind power compared to other energy sources. Additionally, innovations in technology like smart blades, carbon fibre reinforcement, and predictive maintenance systems raise the overall productivity and dependability of wind turbine installations, spurring additional uptake and market expansion.

Restraints:

The market for wind turbine rotor blades faces difficulties as a result of supply chain disruptions, such as raw material shortages, clogged logistics, and transportation limitations. The reliance of manufacturers on worldwide supply chains for essential components like carbon fibre, fibreglass, and resin exposes them to supply chain vulnerabilities that can cause delays in project completion, escalate expenses, and disturb production schedules. To maintain the rotor blade market's resilience and sustainability, supply chain risks must be mitigated through diversification, localization, and strategic alliances.

Regulatory uncertainties and policy changes pose significant restraints on the wind turbine rotor blade market. Inconsistent regulatory frameworks, evolving subsidy programs, and changing trade policies create uncertainty for manufacturers, investors, and project developers. Political instability and trade tensions between countries can disrupt supply chains, increase costs, and impede market growth. Clear and stable regulatory environments that incentivize renewable energy investment, promote market competition, and ensure a level playing field are essential to fostering confidence and driving sustainable growth in the wind turbine rotor blade market.

Opportunities:

The market for rotor blades has enormous growth potential as offshore wind energy grows. The deployment of offshore wind projects is attractive due to their proximity to densely populated coastal areas, higher wind speeds, and larger installation capacities. Demand for specific rotor blades made for offshore conditions is predicted to rise as offshore wind technology advances and costs come down. There are numerous opportunities for manufacturers to create cutting-edge solutions that are specifically suited to the demands and special difficulties of offshore wind installations, such as bigger rotor diameters, floating turbine platforms, and severe weather.

Segment Overview

Carbon Fiber: Carbon fiber rotor blades are renowned for their exceptional strength-to-weight ratio and stiffness, making them ideal for capturing wind energy efficiently. These blades are lightweight yet durable, allowing for larger blade designs capable of harnessing more wind power. Carbon fiber rotor blades offer superior performance in terms of fatigue resistance and aerodynamic efficiency compared to traditional materials, contributing to increased energy output and reduced maintenance costs over the operational lifespan of wind turbines. However, the high cost of carbon fiber materials presents a significant barrier to widespread adoption, limiting their usage primarily to premium and high-performance wind turbine models.

Fiberglass: Fiberglass remains the most widely used material for wind turbine rotor blades due to its affordability, versatility, and ease of manufacturing. Fiberglass blades offer a balance between cost-effectiveness and performance, making them suitable for a broad range of wind energy applications, from small-scale turbines to utility-scale wind farms. These blades are robust, corrosion-resistant, and well-suited to withstand various environmental conditions, making them an attractive choice for onshore and offshore installations alike. While fiberglass blades may not offer the same level of performance as carbon fiber alternatives, ongoing advancements in materials science and manufacturing techniques continue to enhance their efficiency, reliability, and longevity.

Onshore: Onshore wind turbines are situated on land, typically in rural or open areas with favorable wind conditions. Onshore installations are more cost-effective and easier to access for maintenance and infrastructure development compared to offshore sites. Onshore wind farms play a crucial role in global renewable energy generation, providing a reliable source of clean electricity to power homes, businesses, and communities. Despite their widespread deployment, onshore wind projects face challenges related to land availability, permitting, and community acceptance, requiring careful planning and stakeholder engagement to ensure successful implementation and operation.

Offshore: Offshore wind turbines are installed in bodies of water, typically along coastlines or in offshore wind farms situated farther out at sea. Offshore wind offers several advantages, including stronger and more consistent wind speeds, larger installation capacities, and reduced visual and noise impacts compared to onshore projects. Offshore wind farms have the potential to generate significant amounts of clean energy while minimizing land use and environmental footprint. However, offshore installations present unique technical, logistical, and regulatory challenges, including deeper water depths, harsh marine environments, and higher installation and maintenance costs. Despite these challenges, offshore wind power continues to gain momentum globally as technology advances, costs decline, and policymakers prioritize decarbonization and renewable energy development.

Wind Turbine Rotor Blade Overview by Region

Europe stands out as a pioneering region in wind energy adoption, with countries like Germany, Denmark, and the United Kingdom leading the way in offshore wind farm development and technology innovation. The European Union's ambitious renewable energy targets and supportive regulatory frameworks continue to drive investments in wind power infrastructure and stimulate market growth. North America, particularly the United States and Canada, boasts significant onshore wind resources and robust wind energy capacity expansion efforts.

The Production Tax Credit (PTC) and Investment Tax Credit (ITC) schemes in the U.S. incentivize wind power development, fostering a favorable investment environment for wind turbine rotor blade manufacturers. Asia-Pacific emerges as a key growth engine for the wind turbine rotor blade market, driven by rapid industrialization, urbanization, and energy demand in countries such as China and India. Government-led initiatives, technological advancements, and increasing environmental awareness propel the expansion of both onshore and offshore wind power projects across the region. China, in particular, leads the global wind energy market in terms of installed capacity and manufacturing capabilities, offering significant opportunities for domestic and international rotor blade suppliers.

Latin America and the Middle East & Africa regions present untapped potential for wind energy development, with countries like Brazil, Mexico, South Africa, and Egypt investing in wind power infrastructure to diversify their energy mix and reduce reliance on fossil fuels. While each region faces unique challenges and opportunities, the overall outlook for the wind turbine rotor blade market remains positive, driven by the global transition towards clean, renewable energy sources and the continued optimization of wind power generation technologies.

Wind Turbine Rotor Blade Market Competitive Landscape

Established industry leaders such as Siemens Gamesa, Vestas, GE Renewable Energy, and Nordex dominate the global market with their extensive product portfolios, technological expertise, and widespread manufacturing capabilities. These companies leverage their economies of scale, research and development investments, and established customer relationships to maintain their competitive edge and drive innovation in rotor blade design, materials, and manufacturing processes. Additionally, strategic partnerships, mergers, and acquisitions play a pivotal role in shaping the competitive landscape, enabling companies to broaden their geographic reach, access new markets, and enhance their product offerings.

Emerging players and regional manufacturers, including LM Wind Power, Suzlon Energy, TPI Composites, and China Ming Yang Wind Power Group, pose increasing competition by offering specialized solutions, localized services, and competitive pricing strategies. These companies focus on niche market segments, technological differentiation, and customer-centric approaches to gain traction in the highly competitive wind energy sector. Moreover, collaboration with research institutions, universities, and industry associations facilitates knowledge sharing, technology transfer, and capacity building, fostering innovation and driving competitiveness across the wind turbine rotor blade market.

Wind Turbine Rotor Blade Market Leading Companies:

Acciona S.A.

Aeris Energy

EnBW

Enercon GmbH

Gamesa Corporation Technology

Hitachi Power Solutions

MFG Wind

Siemens AG

Suzlon Energy Limited

Vestas Wind Systems A/S

TPI Composites Inc.

Wind Turbine Rotor Blade Recent Developments

Global Wind Turbine Rotor Blade Report Segmentation

|

ATTRIBUTE |

DETAILS |

|

By Type |

|

|

By Location |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.

+1 812 506 4440

+1 812 506 4440

+91 7875074426

+91 7875074426