Telecom Power Systems Market Research Report: By Product Type (AC power systems, DC power systems, Digital electricity), By Grid Type (On-grid, Off-grid, Bad-grid), By Power Source (Diesel-battery, Diesel-solar, Diesel-wind, Other Sources), and Region (North America, Europe, Asia-Pacific, and Rest of the World) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2024-2032.

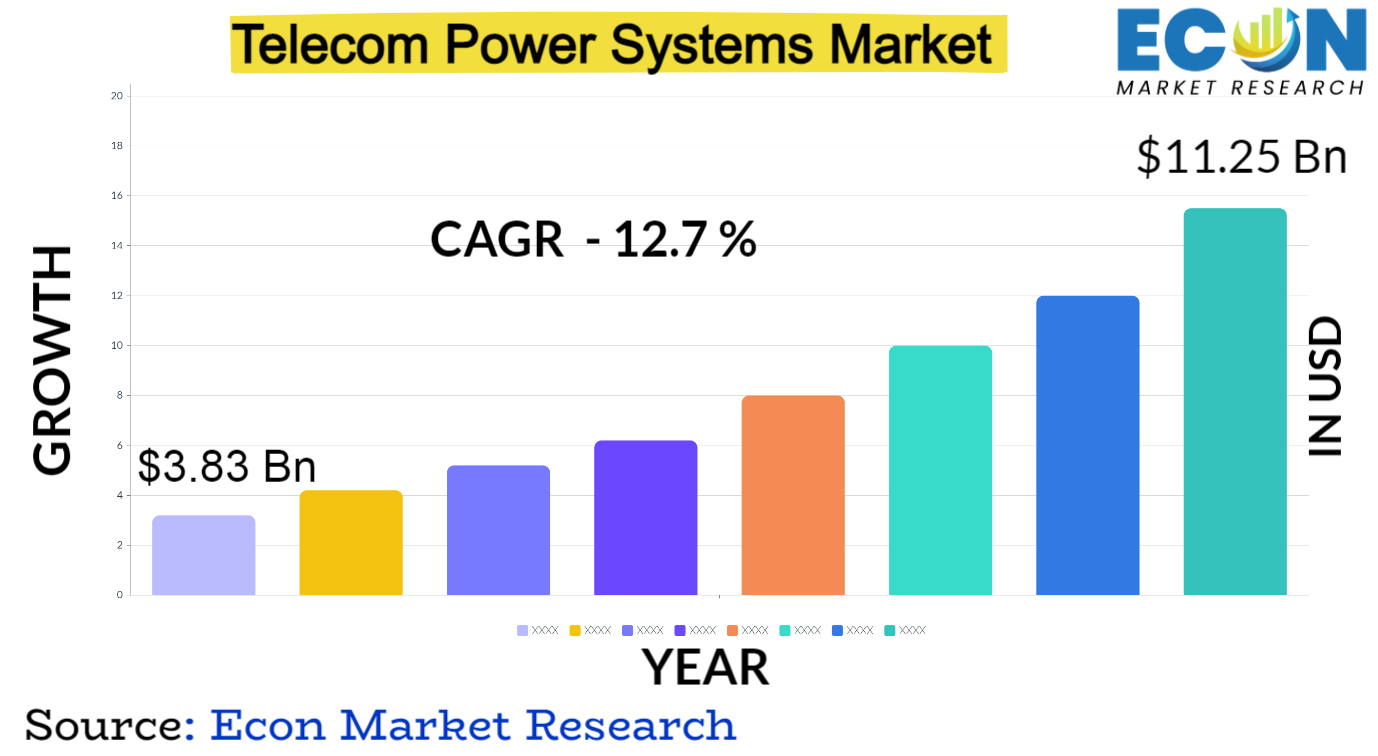

The global telecom power systems market was valued at USD 3.83 billion in 2023 and is estimated to reach approximately USD 11.25 billion by 2032, at a CAGR of 12.7% from 2024 to 2032.

The global communication networks that are dependable and unbroken are made possible by the telecom power systems industry. The massive infrastructure supporting telecommunications, such as cell towers, data centers, and network operations centers, requires reliable and efficient power supply, which is why these systems were created. From backup batteries to hybrid systems that incorporate renewable energy sources like solar and wind power, they cover a wide spectrum of solutions. The industry is constantly driven by innovation because to the ongoing evolution of communications technology, including the deployment of 5G and the growing need for data.

In addition to being strong and resilient,a manufacturers work hard to create power systems that are long-term economically and environmentally viable. The telecom power systems market is continuing to see developments aimed at balancing sustainability and dependability while meeting the increasing demands of the ever-expanding global communication network. These advancements are motivated by the increased emphasis on energy efficiency and the requirement for resilient infrastructure.

TELECOM POWER SYSTEMS MARKET: REPORT SCOPE & SEGMENTATION

TELECOM POWER SYSTEMS MARKET: REPORT SCOPE & SEGMENTATION

|

Report Attribute |

Details |

|

Estimated Market Value (2023) |

3.83 Bn |

|

Projected Market Value (2032) |

11.25 Bn |

|

Base Year |

2023 |

|

Forecast Years |

2024 - 2032 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- By Product Type, By Grid Type, By Power Source, & Region |

|

Segments Covered |

By Product Type, By Grid Type, By Power Source, & Region |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2024 to 2032 |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, and the Rest of World |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis, and COVID-19 impact analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Telecom Power Systems Market Dynamics

Technological developments, regulatory changes, and changing consumer needs drive dynamic movements in the telecom power systems market. The landscape is constantly changing due to technological advancements, with a focus on energy storage, renewable energy integration, and more effective power management systems. These dynamics have been exacerbated by the emergence of 5G technology, necessitating the use of power systems capable of supporting denser networks and handling higher data loads. Furthermore, the industry is under pressure to lower its carbon footprint, which is encouraging the creation of environmentally friendly power solutions and driving a transition to renewable and hybrid energy sources. Governmental actions and regulatory measures are also crucial.

The market dynamics are influenced by subsidies, incentives, and regulations designed to encourage the adoption of clean energy, which encourages telecom companies to make investments in sustainable power systems. The demand from customers for constant connectivity drives innovation even more. The market is moving toward creating backup power solutions that guarantee continuity during outages or emergencies since reliability and resilience are crucial. Furthermore, the competitive landscape is influenced by market consolidation and alliances between major competitors, which have an effect on pricing policies, technological cooperation, and the launch of new goods and services. The telecom power systems market continues to traverse these dynamic forces as the demand for seamless connectivity rises, evolving and adapting to meet the changing needs of the industry.

Telecom Power Systems Drivers

The global deployment of 5G networks necessitates a substantial change in power system capabilities. The fundamental feature of 5G is its capacity to transfer data at previously unheard-of rates, opening the door to a wide range of applications, including augmented reality and smart cities and driverless cars. The proliferation of connected devices and the exponential rise in data transmission speeds require a denser network infrastructure, which increases the energy requirements and operational complexity for telecom operators.

Therefore, the incorporation of 5G technology acts as a stimulant for creative power structures that can sustain this new era of communication. For these systems to meet the increased demands of 5G networks and maintain uninterrupted service, they need to be resilient, scalable, and energy-efficient. The push to reduce power usage and improve network dependability is increasing as telecom companies adopt 5G, which is propelling the development of innovative power solutions that meet the specific needs of these fast, data-intensive networks.

The integration of renewable energy sources, such as solar, wind, and hydroelectric power, into telecom infrastructure has gained speed due to the global focus on sustainability and lowering carbon footprints. The telecom sector, which uses a lot of energy, understands that using renewable energy sources can reduce its operational costs and environmental impact. In addition to being in line with business sustainability objectives, telecom operators can diversify their energy sources and lessen their reliance on conventional fossil fuels by utilizing renewable energy sources.

Furthermore, recent developments in renewable energy technology have increased their dependability and economic viability. For example, the efficiency and affordability of solar panels have increased, making solar power a viable alternative for telecom towers and other infrastructure, particularly in distant places. Furthermore, even in locations where renewable energy generation is sporadic, continuous power delivery is made possible by the flexibility of integrating renewable sources with energy storage systems. This change is further accelerated by regulatory initiatives supporting clean energy, which provide telecom firms with incentives and obligations to invest in sustainable power solutions.

Restraints:

Adoption of modern and sustainable power solutions is hindered by the high upfront costs associated with their implementation. Significant capital expenditure is needed for the integration of renewable energy sources, energy-efficient infrastructure upgrades, and the implementation of advanced power management systems. These expenses may be exorbitant for telecom operators, particularly when increasing network coverage or in developing nations, which could affect the pace and scope of deployment. Furthermore, these systems' lifespan and return on investment are important considerations while making decisions.

The initial capital expenditure associated with these technologies may discourage businesses from adopting them, even despite the possible long-term cost advantages of lower operating costs and increased energy efficiency. The perceived risk may also be increased by ambiguity around the swift advances and technological breakthroughs in the field, which could raise questions about the long-term viability and compatibility of the selected solutions. Smaller operators and those with fewer financial resources are also impacted by this constraint, which could lead to differences in the telecom sector's adoption of more economical and environmentally friendly power solutions.

Complex issues might arise when integrating various energy sources, guaranteeing compatibility with existing infrastructure, and implementing sophisticated power management systems. These sophisticated systems need to be implemented with specific knowledge and skills, which frequently calls for qualified personnel with experience negotiating challenging integration procedures. Significant technical obstacles also arise from the need for different components to be compatible and interoperable, particularly when integrating renewable energy sources with traditional power systems.

Furthermore, there is ambiguity regarding the long-term viability and compatibility of current solutions with future improvements due to the rapid evolution of technology. This complexity goes beyond installation to include ongoing upkeep and operation, thus to guarantee peak performance, continual support and training are required. This complexity might be a major obstacle to the adoption and efficient management of these cutting-edge power systems for smaller telecom operators or those without internal technical competence. The complexity of integrating technology also raises the possibility of system malfunctions or failures. As systems get more complicated, it becomes harder to ensure flawless performance and diagnose problems.

Opportunities:

The integration of electrical and telecommunications networks enables the creation of smart grids, which transform energy distribution and administration. Smart grids monitor, regulate, and optimize the flow of power, improving efficiency and dependability. They do this by utilizing cutting-edge communication technology. The foundation for real-time data transmission is provided by telecom infrastructure, which enables utilities to obtain accurate data on grid operation and patterns of energy usage. Through dynamic modifications made possible by this integration, load management is improved, and power networks' overall resilience is increased.

Additionally, smart grids encourage two-way communication between utilities and customers, giving customers more control over how much energy they use. Customers may make educated decisions to optimize energy usage by gaining insights into their usage patterns through smart meters and IoT-enabled devices. Demand response programs, which allow users to modify their use during peak hours and so improve grid stability, are made possible by this interaction. There is a rare chance for telecom businesses to work with utility providers to develop and implement smart grid solutions.

By moving computation closer to the data source, the spread of IoT devices and the use of edge computing designs have completely changed data processing and storage. Strong, distributed computing infrastructure is needed for this transformation, which raises the need for dependable, efficient power systems that can sustain these decentralized networks. Telecom firms have the potential to leverage their infrastructure and expertise to offer customized power solutions that are optimized for edge computing environments and Internet of Things deployments. These systems must be able to handle the particular requirements of remote computing, including changing workloads and shifting data processing requirements, all while guaranteeing a constant power supply. Moreover, cutting-edge applications in a variety of sectors are made possible by the combination of edge computing with IoT, including smart cities, industrial automation, and healthcare. Telecom power systems suppliers can work with a variety of industries by providing specific power solutions that make it possible for these networked devices and edge computer nodes to function seamlessly.

Segment Overview

Based on product type, the global telecom power systems market is divided into AC power systems, DC power systems, and digital electricity. The DC power systems category dominates the market with the largest revenue share in 2023. Because of its built-in efficiency and interoperability with a wide range of electronic devices, direct current (DC) power systems have become more and more popular in telecom applications. In DC systems, AC power is converted into DC via rectifiers and used directly to power telecom equipment.

Better control over power distribution inside telecom facilities, lower transmission power losses, and increased energy efficiency are all frequently provided by these systems. For powering telecom infrastructure, switching to AC power systems has long been the standard. These devices transform alternating current (AC) power from generators or the grid to the voltage levels needed by telecom devices. To control the voltage and provide dependable power distribution, they often include parts like rectifiers, inverters, and transformers.

A new idea called "digital electricity" aims to change the way power is distributed and managed in communication networks. In order to build a more intelligent and effective power infrastructure, it entails the integration of digital technologies, including advanced control systems, power electronics, and sensors. The goal of digital electricity is to improve real-time power usage monitoring, control, and optimization. This will allow for dynamic modifications based on variations in demand and increase overall energy efficiency.

Based on the grid type, the global telecom power systems market is categorized into on-grid, off-grid, and bad-grid. The on-grid category leads the global telecom power systems market with the largest revenue share in 2023. Telecom power configurations that are directly linked to the main electrical grid are referred to as "on-grid" systems. Cell towers, data centers, and network infrastructure are examples of the telecommunications infrastructure that these systems mostly rely on for electricity provided by utilities.

Since on-grid systems get their electricity from the centralized grid network, they have the advantage of a steady and reliable power supply. They are frequently used in populated, urban regions with dependable grid infrastructure. Off-grid electrical systems function apart from the main power grid. They are intended to supply electricity to telecom infrastructure in isolated or rural locations with spotty or nonexistent grid connectivity. These systems frequently combine energy storage devices like batteries with renewable energy sources like solar panels, wind turbines, or fuel-powered generators.

Regions with an intermittent or unreliable grid infrastructure are served by bad-grid solutions. Frequent power outages, voltage fluctuations, or low-quality electrical supplies are problems for these systems. To make up for grid weaknesses, bad-grid solutions incorporate components of both on- and off-grid systems, making use of the current grid infrastructure and adding energy storage and backup power sources.

Based on the power source, the global telecom power systems market is segmented into diesel-battery, diesel-solar, diesel-wind, and other sources. The diesel-battery systems dominate the telecom power systems market. Usually, these systems include battery storage options along with diesel generators. The main power source for telecom infrastructure is diesel generators, which supply constant electricity, particularly in places with spotty or restricted grid connectivity. In the event of fuel shortages or generator maintenance, the batteries serve as a backup or supplemental power source, guaranteeing a continuous power supply. These systems use batteries for load balancing and low-demand power generation in an effort to minimize fuel usage and generator runtime.

Diesel-solar systems combine solar panels and diesel generators to power communication devices. By acting as a backup and renewable power supply, solar energy lowers operating expenses and the need for diesel generators. Solar panels use sunshine to create electricity during the day, which helps to balance off or supplement the energy that diesel generators are usually used to produce. This combo seeks to increase energy efficiency, reduce carbon emissions, and decrease fuel usage.

Diesel-wind systems work similarly to diesel-solar systems in that they combine diesel generators and wind turbines to provide electricity for telecommunications infrastructure. By using wind energy to create electricity, diesel-generated electricity is supplemented by wind energy. By adding to the power supply and providing a renewable energy source, wind turbines lessen the need for diesel generators. These systems offer a sustainable substitute for fossil fuel-based power generation and are beneficial in windy areas.

Telecom Power Systems Overview by Region

The global telecom power systems market is categorized into North America, Europe, Asia-Pacific, and the Rest of the World. Asia-Pacific emerged as the leading region, capturing the largest market share in 2023. The region's telecommunications industry has grown dramatically due to rapid urbanization, substantial population increase, and the growing adoption of digital technology across industries.

The increase in the development of telecommunications infrastructure, encompassing data centers, broadband connection, and mobile networks, has increased the need for dependable and effective power systems. Furthermore, the Asia-Pacific region's geographical diversity poses a variety of difficulties, from heavily populated urban areas to isolated and underdeveloped rural areas. This diversity has encouraged innovation in power solutions, resulting in a range of implementations from off-grid and hybrid solutions in remote locations to sophisticated grid-connected systems in metropolitan centers. Throughout the forecast period, North America is anticipated to post a significant CAGR.

The need for modernized and effective power systems is driven by the region's rapid technical breakthroughs and early adoption of next-generation communication technologies, such as 5G networks. Furthermore, the demand for dependable power solutions is increased by the growing digitization of all industries, the expansion of data centers, and the Internet of Things (IoT). The incorporation of renewable energy into sophisticated telecom power systems is further supported by regulatory initiatives that promote sustainability and energy efficiency. Furthermore, the consistent expansion of the market in North America is facilitated by the strategic investments made by telecom operators and technology companies in enhancing network coverage and boosting connectivity.

Telecom Power Systems Competitive Landscape

In the global telecom power systems market, a few major players exert significant market dominance and have established a strong regional presence. These leading companies remain committed to continuous research and development endeavors and actively engage in strategic growth initiatives, including product development, launches, joint ventures, and partnerships. By pursuing these strategies, these companies aim to strengthen their market position, expand their customer base, and capture a substantial share of the market.

Telecom Power Systems Market Leading Companies

Telecom Power Systems Recent Developments

Telecom Power Systems Market Report Segmentation

|

ATTRIBUTE |

DETAILS |

|

By Product Type |

|

|

By Grid Type |

|

|

By Power Source |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.

+1 812 506 4440

+1 812 506 4440

+91 7875074426

+91 7875074426