Global Semi-Trailer Market Research Report: By Type (Flatbed, Lowboy, Dry Van, Refrigerated, Tanker, Others), By Tonnage Type (Below 25 Ton, 2550 Ton, 51100 Ton, Above 100 Ton), By Number of Axles (Less Than 3 Axles, 34 Axles, More Than 4 Axles), and Region (North America, Europe, Asia-Pacific, and Rest of the World) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2024-2032.

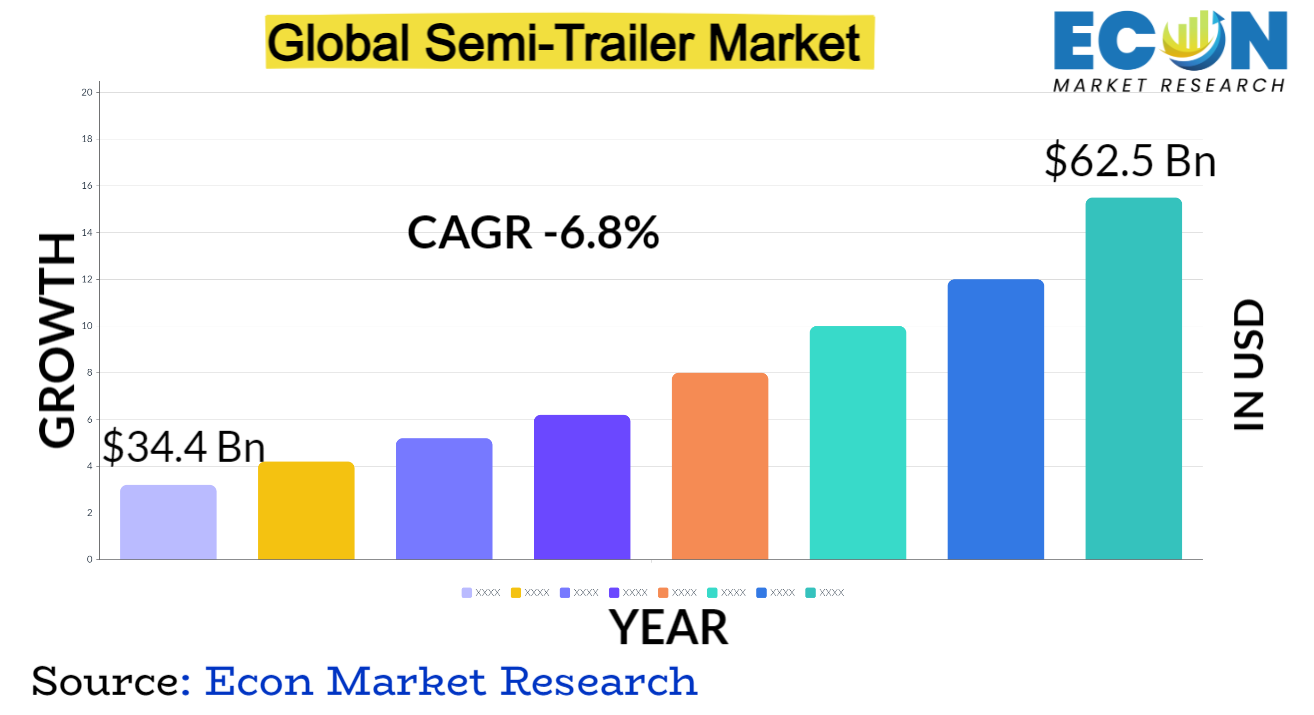

The global semi-trailer market was valued at USD 34.4 billion in 2023 and is estimated to reach approximately USD 62.5 billion by 2032, at a CAGR of 6.8% from 2024 to 2032.

The transportation sector underwent a radical change with the emergence of the semi-trailer market. Although the semi-trailer had its beginnings in the late 19th century, its development picked up speed in the 20th century, especially in the 1920s. Semi-trailer integration transformed freight transportation by providing more capacity and improved efficiency over conventional freight techniques. Its widespread use was reinforced in the 1950s with the important invention of the fifth-wheel coupling system, which made it possible for trucks and trailers to join seamlessly. This invention opened up a huge market by giving long-distance goods transportation a more flexible, economical, and adaptable option. In the second half of the 20th century, the market expanded exponentially as a result of developments in manufacturing and technology. The emergence of computer-aided design (CAD) and manufacturing (CAM) has significantly improved production accuracy and simplified customisation, meeting the demands of various industries. Moreover, the market's attractiveness was increased by the incorporation of strong but lightweight materials like aluminum and sophisticated composites, which improved fuel efficiency and load capacity. With the introduction of smart technologies in the 21st century, such as telematics and autonomous features that optimize safety and logistics, the industry advanced. The semi-trailer industry has established itself as an essential part of global logistics and transportation networks, serving a wide range of industries from manufacturing and retail to agricultural and beyond, because of its constant innovation and adaptability.

SEMI-TRAILER MARKET: REPORT SCOPE & SEGMENTATION

|

Report Attribute |

Details |

|

Estimated Market Value (2023) |

34.4 Bn |

|

Projected Market Value (2032) |

62.5 Bn |

|

Base Year |

2023 |

|

Forecast Years |

2024 - 2032 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- By Type, By Tonnage Type, By Number of Axles, & Region |

|

Segments Covered |

By Type, By Tonnage Type, By Number of Axles, & Region |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2024 to 2032 |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, and the Rest of World |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis, and COVID-19 impact analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Global Semi-Trailer Market Dynamics

Economic factors have a fundamental role in shaping market patterns, as variations in international trade, consumer demand, and factory production have a substantial effect on the demand for transportation services. The market environment is greatly influenced by regulatory changes, such as those pertaining to safety and emissions standards, which frequently spur technological and design advancements in order to comply with legal requirements. Furthermore, the dynamics of the business have changed due to technological improvements. Automation, IoT (Internet of Things), and telematics integration have improved logistics and raised operational and safety standards. In addition, the market has been directed toward environmentally friendly solutions by the increased emphasis on sustainability, which has led to the development of electric and hybrid semi-trailers as a way to lower carbon footprints. Many manufacturers fighting for market share define the competitive environment in the semi-trailer industry. Customer choices are greatly influenced by factors like product quality, cost-effectiveness, dependability, and after-sales services. In addition, the industry is always seeing innovations in materials and designs with the goal of optimizing load capacities while reducing weight to increase fuel efficiency—a critical component considering the growing worries about operational costs and environmental effect. All things considered, the dynamics of the semi-trailer market are a complicated combination of technological, economic, regulatory, and competitive elements that are still influencing its development.

Global Semi-Trailer Market Drivers

Automation is a significant technical advancement that has revolutionized operations by improving safety, streamlining routes, maximizing fuel efficiency, and enabling autonomous driving characteristics. Another important development in fleet management is telematics, which combines real-time data monitoring and analysis to provide insights into vehicle performance, maintenance requirements, and route optimization. Additionally, improved connectivity made possible by the integration of Internet of Things (IoT) devices has allowed trailers to communicate vital information like location, temperature (in refrigerated trailers), and cargo status, promoting increased efficiency and transparency throughout the supply chain. With the use of strong, lightweight materials like aluminum alloys, high-strength steel, and sophisticated composites, advances in materials science have produced trailers that optimize cargo capacity while consuming the least amount of gasoline. In addition, the introduction of hybrid and electric semi-trailers signifies a revolutionary turn in the direction of sustainability, tackling environmental issues and cutting carbon emissions. Together, these technical developments spur innovation in the semi-trailer sector, enhancing sustainability, safety, efficiency, and personalization while influencing global logistics and transportation trends.

The industry's dedication to sustainability has accelerated the creation of environmentally friendly products and procedures, as evidenced by the growing popularity of electric and hybrid semi-trailers. By lowering dependency on fossil fuels, these cutting-edge cars mitigate carbon emissions and make a substantial contribution to a greener transportation ecosystem. Furthermore, developments in materials science have made it possible to create strong, lightweight materials that improve fuel economy and lessen the total environmental effect of transportation. Enhancing sustainability efforts, aerodynamics and energy-efficient design initiatives optimize trailers for less drag and more fuel efficiency. Sustainability activities extend beyond technical advancements and include supply chain techniques such as effective route planning, load optimization, and waste reduction tactics. Businesses are embracing the circular economy more and more, placing a focus on material reuse, recycling, and responsible disposal to lessen the environmental impact of their operations. The increasing focus on sustainability reflects a fundamental movement toward ethical and responsible corporate practices rather than just a reaction to regulatory restrictions.

Restraints:

Advanced technology integration necessitates significant upfront costs. Examples of these include telematics systems, autonomous features, and electric/hybrid propulsion. These expenses pay for both the acquisition of state-of-the-art machinery and parts as well as the infrastructural improvements necessary for their efficient use. The costs incurred in maintaining strict adherence to regulatory requirements also add to the strain. Production and operations will incur significant expenses as a result of the research, development, and technology adaption required to assure compliance with changing safety, emissions, and operating laws. Furthermore, although implementing sustainable practices has long-term benefits, it frequently comes with higher initial costs. Some market participants may find it difficult to afford the significant upfront expenses associated with developing and implementing environmentally friendly solutions, such as lightweight materials or alternative propulsion systems like electric powertrains. Due to the high implementation costs, small and medium-sized firms (SMEs) in the industry can find it difficult to enter or grow. Their capacity to compete and innovate on par with larger firms may be limited by the strain on their financial resources caused by having to access funds for technical upgrades, regulatory procedures, or sustainability projects.

Supply chain disruptions resulting from natural catastrophes, geopolitical tensions, or worldwide events such as the COVID-19 pandemic can lead to delays in the acquisition of vital components, resources, or completed parts required for the construction of semi-trailers. These disruptions impair production plans, creating bottlenecks, longer lead times, and even possible production stoppages, which reduces the industry's capacity to satisfy consumer demand. Furthermore, production costs and viability are significantly impacted by the cost and availability of raw materials, including steel, aluminum, composite materials, and specialty components. Price fluctuations for raw materials, supply shortages brought on by rising demand, or problems with the extraction or production process can all result in higher material costs and supply constraints, which have an immediate effect on the semi-trailer manufacturing industry's entire cost structure. Because the business depends on international supply networks to source raw materials, it is more vulnerable to disruptions from geopolitical tensions, trade conflicts, and logistical difficulties. In addition to affecting semi-trailer manufacturing volume and cost-effectiveness, these limitations force producers to reevaluate the robustness of their supply chains and look into alternate sourcing techniques in order to reduce these risks.

Opportunities:

The need for effective and specialized transportation solutions to handle the last leg of delivery from distribution centers to customers' doorsteps has increased due to the exponential growth in online shopping. Due to the increase in last-mile logistics, semi-trailers that are adaptive and versatile enough to manage a variety of cargo, maximize available space, and maneuver through cities with ease are needed. Semi-trailers with features like lift gates or adjustable compartments, or those that are smaller in size and designed specifically for last-mile deliveries, are in high demand. These trailers are designed to meet the demands of consumer-direct package delivery, improving speed and convenience in both urban and suburban environments. Moreover, telematics and route optimization systems two developments in semi-trailer technology offer chances to optimize last-mile delivery processes. Delivery times can be shortened, deliveries can be made more precisely and economically because to these technologies' real-time tracking, effective route planning, and improved fleet management capabilities.

Companies are under increasing pressure to replace their older, less fuel-efficient trailers with newer versions that have advanced capabilities due to technical improvements and regulatory changes. Modern semi-trailers are in high demand because to factors like lower environmental effect, enhanced safety regulations, and higher operating efficiency. Modern features like autonomous functions, telematics, and aerodynamic designs that maximize fuel economy, save maintenance costs, and improve overall performance are frequently seen in newer models. Moreover, older trailers might need to be replaced in order to comply with the most recent rules as laws change, particularly those pertaining to safety standards and emissions. This combination opens up a sizable market for suppliers and manufacturers who provide technologically sophisticated, compliant semi-trailers. Enterprises seeking to maintain their competitiveness and satisfy changing customer needs are more likely to make fleet modernization investments. Because of this, the semi-trailer industry has a tremendous chance to serve this market segment by offering creative, sustainable, and effective trailers that meet the needs of businesses wishing to update their fleets in order to become more competitive and efficient.

Segment Overview

By Type

Based on type, the global semi-trailer market is divided into flatbed, lowboy, dry van, refrigerated, tanker, others. The lowboy category dominates the market with the largest revenue share in 2023. Lowboy trailers have a lower deck height closer to the ground, often with two drops in deck height, allowing them to transport taller and heavier loads, such as heavy machinery, industrial equipment, or oversized vehicles like bulldozers or excavators. Flatbed trailers have a flat, open design without sides or a roof, offering easy loading and unloading of goods from the sides or above. They're versatile, suitable for transporting large or irregularly shaped cargo like machinery, construction materials, or oversized goods. Enclosed and fully covered, dry van trailers protect cargo from weather conditions and theft. They're versatile and commonly used for transporting a wide range of dry goods, including consumer goods, electronics, clothing, and non-perishable items. Refrigerated trailers are equipped with refrigeration units to maintain specific temperature conditions, ideal for transporting perishable goods such as food, pharmaceuticals, or chemicals that require controlled temperature environments to preserve their quality. Tanker trailers designed specifically for transporting liquids or gases, tanker trailers come in various forms, including those for transporting water, chemicals, fuel, or gases like oxygen or nitrogen. They're built with specialized compartments and materials to ensure safe transportation.

By Tonnage Type

Based on the tonnage type, the global semi-trailer market is categorized into below 25 ton, 25–50 ton, 51–100 ton, above 100 ton. The 25–50 ton category leads the global semi-trailer market with the largest revenue share in 2023. This segment covers a moderate weight capacity range, catering to a broad spectrum of cargo transportation needs. These semi-trailers are versatile and can handle a variety of goods, including construction materials, medium-sized machinery, or goods with moderate weight. Below 25 tons semi-trailers typically have a lower weight capacity, making them suitable for lighter cargo and smaller loads. They might be used for transporting smaller machinery, construction materials, or goods that don't require heavy-duty hauling. 51–100 tons semi-trailers range are designed for heavier loads and larger cargo. They're commonly used in industries requiring substantial hauling capacity, such as transporting heavy machinery, bulk materials, or oversized items that demand a higher weight limit. Above 100 tons category encompasses the heavy-duty segment of the market, reserved for specialized trailers capable of transporting extremely heavy loads. They're utilized for transporting massive industrial equipment, oversized machinery, or exceptionally heavy goods that necessitate significant weight-bearing capacity.

By Number of Axles

Based on number of axles, the global semi-trailer market is segmented into less than 3 axles, 3–4 axles, more than 4 axles. The 3–4 axles segment dominates the semi-trailer market. This segment covers a moderate range of axles, offering a balance between load capacity and maneuverability. Trailers within this category can handle a broader range of cargo and weight capacities compared to those with fewer axles. They strike a balance between weight distribution and ease of maneuvering. Less than 3 axles semi-trailers typically have fewer axles, making them suitable for lighter loads and offering greater maneuverability. These trailers might be used for transporting smaller cargo, goods with lower weight requirements, or in situations where navigating tighter spaces is necessary. Semi-trailers with more than four axles are typically designed for heavier loads and higher weight capacities. These trailers distribute weight more evenly, allowing for the transportation of significantly heavier cargo. They offer greater stability and support for hauling larger loads.

Global Semi-Trailer Market Overview by Region

The global semi-trailer market is categorized into North America, Europe, Asia-Pacific, and the Rest of the World. Asia-Pacific emerged as the leading region, capturing the largest market share in 2023. China, India, Japan, South Korea, and Southeast Asian countries are among the growing economies in the region that have experienced fast industrialization, urbanization, and infrastructure development. Due to the increase in demand for effective transportation options brought about by this economic upsurge, semi-trucks are becoming more and more necessary in a variety of industries. Furthermore, the region's strategic location and status as a hub for global industry have increased demand for freight transport and logistics. The transportation of commodities, both domestically and internationally, has increased due to vast trade networks and rising cross-border trade. This has increased demand for a variety of semi-trailer designs to meet varying cargo needs. The need for semi-trailers has also been boosted by government programs that support the construction of strong transportation networks, trade facilitation, and infrastructure development. The rise of the logistics and transportation industries has been facilitated by investments in ports, highways, and intermodal transportation systems, which has increased demand for semi-trailers. The dynamic market in the region, which is defined by a wide range of sectors and changing customer needs, has prompted semi-trailer manufacture to become more innovative and customized in order to suit industry requirements. The Asia-Pacific area's leadership in the global semi-trailer market has been solidified by its flexibility and responsiveness to market demands.

Global Semi-Trailer Market Competitive Landscape

In the global semi-trailer market, a few major players exert significant market dominance and have established a strong regional presence. These leading companies remain committed to continuous research and development endeavors and actively engage in strategic growth initiatives, including product development, launches, joint ventures, and partnerships. By pursuing these strategies, these companies aim to strengthen their market position, expand their customer base, and capture a substantial share of the market.

Some of the prominent players in the global semi-trailer market include Qingdao CIMC Special Vehicles Co., Ltd; Fontaine Trailer; Great Dane A Division of Great Dane LLC.; Kögel; KRONE Trailer; LAMBERET SAS; Polar Tank Trailer.; Schmitz Cargobull.; Utility Trailer Manufacturing Company; Wabash National Corporation.; HYUNDAI TRANSLEAD, and various other key players.

Global Semi-Trailer Market Recent Developments

Scope of the Global Semi-Trailer Market Report

Semi-Trailer Market Report Segmentation

|

ATTRIBUTE |

DETAILS |

|

By Type |

|

|

By Tonnage Type |

|

|

By Number of Axles |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Objectives of the Study

The objectives of the study are summarized in 5 stages. They are as mentioned below:

To identify and estimate the market size for the global semi-trailer market segmented by type, by tonnage type, by number of axles, region and by value (in U.S. dollars). Also, to understand the consumption/ demand created by consumers of semi-trailer between 2019 and 2032.

To identify and infer the drivers, restraints, opportunities, and challenges for the global semi-trailer market.

To find out the factors which are affecting the sales of semi-trailer among consumers.

To identify and understand the various factors involved in the global semi-trailer market affected by the pandemic.

To provide a detailed insight into the major companies operating in the market. The profiling will include the financial health of the company's past 2-3 years with segmental and regional revenue breakup, product offering, recent developments, SWOT analysis, and key strategies.

Intended Audience

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.