Global Offshore Pipeline Market Research Report: By Diameter (Below 24 Inches, Greater Than 24 Inches), By Product (Oil, Gas, Refined Products), By Line Type (Transport Lines, Export Lines, Other Lines), By Installation Type (S-lay, J-lay, Tow-in), By Depth (Shallow Water, Deepwater), and Region (North America, Europe, Asia-Pacific, and Rest of the World) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2023-2031.

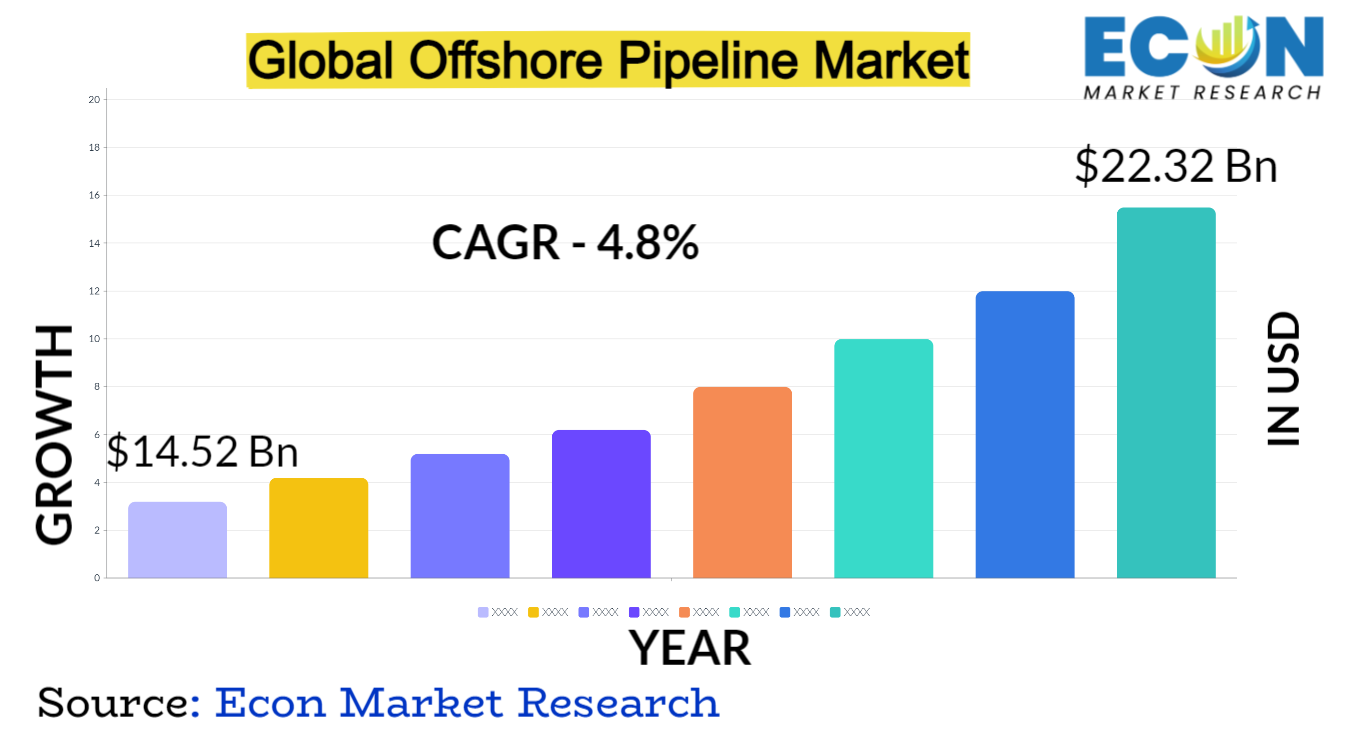

The global offshore pipeline market was valued at USD 14.52 billion in 2022 and is estimated to reach approximately USD 22.32 billion by 2031, at a CAGR of 4.8% from 2023 to 2031.

An essential piece of infrastructure supporting the worldwide oil and gas sector is the offshore pipeline market. These pipelines are engineering marvels that connect offshore drilling sites to onshore facilities and distribution networks while carrying enormous volumes of gas and oil across oceans. They are often built over thousands of miles in difficult maritime settings, requiring state-of-the-art technologies and careful planning. Rising energy demands, particularly from emerging economies, have led to significant expansion in the offshore pipeline business. The longevity and dependability of pipelines have been improved by technological developments in corrosion prevention, pipeline materials, and installation methods. Furthermore, the search for new oil and gas resources as well as the move towards deeper offshore reserves are what keep this market growing. Regulations pertaining to safety standards and environmental factors are becoming more and more important, impacting pipeline operations and design. The offshore pipeline industry is adapting to the changing global energy landscape and providing dependable and efficient solutions for the transfer of hydrocarbons from offshore production sites to refineries and consumers around the globe.

OFFSHORE PIPELINE MARKET: REPORT SCOPE & SEGMENTATION

|

Report Attribute |

Details |

|

Estimated Market Value (2022) |

14.52 Bn |

|

Projected Market Value (2031) |

22.32 Bn |

|

Base Year |

2022 |

|

Forecast Years |

2023 - 2031 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- By Diameter, By Product, By Line Type, By Installation Type, By Depth, & Region |

|

Segments Covered |

By Diameter, By Product, By Line Type, By Installation Type, By Depth, & Region |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2023 to 2031 |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, and the Rest of World |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis, and COVID-19 impact analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Global Offshore Pipeline Market Dynamics

Changes in the world's energy demand, geopolitical unrest, technical breakthroughs, and environmental concerns all impact market dynamics. Investment decisions in offshore pipeline infrastructure are heavily influenced by fluctuations in the price of gas and oil. Variable pricing have a direct impact on the demand for pipelines by either stimulating or discouraging exploration and production activity. International agreements and regional conflicts are examples of geopolitical issues that impact the market. Offshore pipeline design and operations are impacted by regulatory changes and policies pertaining to safety requirements, emissions reduction, and environmental conservation. These changes and policies also spur innovation in these areas. Furthermore, technological developments in monitoring systems, building methods, and pipeline materials continuously reshape the market and make more economical and effective solutions possible. The market dynamics are further shaped by the drive towards environmental programs and renewable energy sources. As a result of this shift, oil and gas firms are compelled to reevaluate their long-term investments in offshore pipelines in order to balance the changing energy mix with their traditional needs for transportation of hydrocarbons. The durability and growth of the offshore pipeline sector hinge on its capacity to adjust to these complex dynamics and harmonize with both market forces and the worldwide movement towards sustainable energy solutions. For stakeholders to prosper in this dynamic industry, they must comprehend and manage these interrelated dynamics.

Global Offshore Pipeline Market Drivers

Energy demand is constantly rising as economies and populations rise. This increase is especially noticeable in developing nations where the demand for dependable energy sources is being driven by fast industrialization and urbanization. Large amounts of gas and oil can be transported from offshore drilling sites to different locations across continents with the help of offshore pipelines, which play an essential role in this process. Because fossil fuels are the main source of energy, we continue to rely on them, which makes pipeline infrastructures more durable and extensive necessary. Additionally, these pipelines support energy security for countries that depend on imported fuels by guaranteeing the reliable and safe supply of energy supplies. But the growing need isn't limited to conventional hydrocarbons alone; it also includes more recent energy forms like hydrogen and liquefied natural gas (LNG), which further broadens the function and possibilities of offshore pipelines. The need for offshore pipeline expansion, modernization, and innovation is driven by this growing demand.

These cutting-edge technologies provide smooth and accurate administration of pipeline operations in demanding maritime conditions. They range from automated control systems to real-time data analytics. Processes are streamlined by automation, which minimizes human error and intervention while maximizing the flow of gas and oil through pipelines. This guarantees continuous and safe resource transportation by reducing downtime and accident risk in addition to improving operational efficiency. Furthermore, advanced monitoring systems are now considered essential to pipeline safety. They make it possible to conduct thorough monitoring and quickly identify anomalies, leaks, or structural problems. These systems include sensors, drones, and satellite technology to offer round-the-clock monitoring. This enables prompt response to any anomalies discovered, thereby averting any environmental risks or accidents. The lifespan of offshore pipelines is extended and operational efficiency and safety requirements are raised by the integration of automation and monitoring systems, which also drastically lowers maintenance costs. These developments also enable proactive interventions to avert possible problems through predictive maintenance, which makes the offshore pipeline system more robust and sustainable.

Restraints:

Keeping up with changing environmental regulations necessitates large infrastructure and technology investments, which drives up operating expenses. Regulatory organizations enforce strict rules due to concerns regarding the ecological impact of pipeline construction, operation, and potential spills. This results in the need for comprehensive environmental impact assessments and mitigation methods. Furthermore, there are particular difficulties while navigating various ecosystems in maritime settings. Because pipelines must pass through delicate environments, stringent rules must be followed to reduce disruption to ecosystems and marine life. Pipeline projects become more complex and expensive due to the requirement for environmentally friendly building methods, monitoring systems, and maintenance procedures. Environmental scrutiny also makes obtaining permits and approvals a time-consuming and complex procedure, which causes delays in projects and higher costs. In order to maintain compliance with environmental regulations while maintaining operating efficiency, there is a continuing need for innovation and investments in eco-conscious technologies. Offshore pipeline projects' viability and profitability are impacted by the need for strategic planning and ongoing adaption in response to changing regulatory requirements.

Many times, offshore pipelines pass through areas where there are geopolitical tensions, conflicts, or instability. Threats from intentional sabotage, piracy, or terrorist activity to disruptions brought on by political unrest or territorial conflicts can be found in such unstable circumstances. The pipeline system is exposed to significant risks due to these uncertainties, which can cause disruptions and hinder the safe and reliable movement of commodities. Project complexity is further increased by the intricate web of international connections and the diverse legal systems that exist across national boundaries. Negotiations, agreements, and investment partnerships that are required for cross-border pipeline projects can be delayed due to competing interests among states or geopolitical alignments. Because of the unpredictability created by this complex geopolitical environment, long-term planning and investment decisions are difficult. A complex strategy including increased security, risk reduction techniques, and diplomatic diplomacy is required to address these geopolitical constraints. For offshore pipeline operations to remain stable and secure while navigating geopolitical concerns, cooperation between governments, international organizations, and industry actors is essential.

Opportunities:

In order to support offshore wind energy projects or enable the transportation of renewable energy sources like hydrogen, offshore pipelines which have historically been used to carry fossil fuels can be converted or upgraded. This integration has two benefits. it makes the most of the current pipeline networks and promotes the expansion of the renewable energy markets. For example, converting pipelines to carry hydrogen meets the demand for sustainable energy sources and facilitates the shift to a low-carbon economy. Hydrogen is a renewable energy source that complements decarbonization efforts and provides a competitive substitute for conventional fossil fuels. Furthermore, by combining offshore wind farms with already-existing pipeline systems, clean energy may be used more widely and efficiently by transmitting power from these renewable energy sources to onshore networks. This is a chance to maximize the potential of offshore pipelines in achieving renewable energy targets by repurposing existing infrastructure and taking advantage of their strategic location.

Exploring new oil and gas fields and delving into deeper offshore deposits is becoming more popular as technology develops and energy demands rise. The building of vast and effective pipeline networks is required to move these priceless resources from isolated offshore regions to onshore facilities as a result of this expansion. A strong pipeline infrastructure is required to link these isolated locations to processing centers and distribution networks as a result of the finding of new reserves and the growing emphasis on deepwater exploration. In addition to requiring additional pipelines, expanding offshore production presents opportunity for pipeline upgrading and modifications to handle larger quantities and more demanding environments. Pipeline firms' prospects are further enhanced by the discovery of untapped resources in previously inaccessible places and the progress of extraction processes. Because they guarantee dependable pathways for the transportation of recently discovered oil and gas deposits, these advancements increase energy security by stimulating investments in pipeline infrastructure and promoting technological innovation and job creation.

Segment Overview

By Diameter

Based on diameter, the global offshore pipeline market is divided into below 24 inches, greater than 24 inches. The greater than 24 inches category dominates the market with the largest revenue share in 2022. Pipelines with diameters exceeding 24 inches are larger and primarily used for transporting higher volumes of oil or gas over longer distances. They form the backbone of offshore energy transportation, connecting major production sites in deep-sea locations to onshore refineries, processing plants, and distribution networks. These larger pipelines are crucial for meeting significant energy demands across regions and countries, facilitating the movement of substantial quantities of resources. Below 24 inches, these pipelines typically have smaller diameters and are commonly used for transporting natural gas, refined petroleum products, or other smaller volume substances. They might serve purposes such as supplying gas to nearby regions or connecting smaller offshore production facilities to onshore processing plants. Their smaller size often makes them more cost-effective for shorter distances or lower-volume transportation needs.

By Product

Based on the product, the global offshore pipeline market is categorized into oil, gas, refined products. The gas category leads the global offshore pipeline market with the largest revenue share in 2022. Gas pipelines transport natural gas extracted from offshore reserves to onshore processing facilities, storage sites, or distribution networks. They facilitate the movement of natural gas used for heating, electricity generation, industrial processes, and as a feedstock for various chemical productions. Oil pipelines are dedicated to transporting crude oil extracted from offshore drilling sites to onshore refineries or distribution centers. Oil pipelines play a crucial role in the energy supply chain, facilitating the movement of crude oil for processing into various petroleum products such as gasoline, diesel, and jet fuel. Refined products pipelines are designed to transport processed petroleum products from refineries to distribution centers, terminals, or end-users. These pipelines transport products like gasoline, diesel, jet fuel, and various petrochemicals derived from the refining process to meet consumer demands across regions.

By Line Type

Based on line type, the global offshore pipeline market is segmented into transport lines, export lines, other lines. The transport lines segment dominates the offshore pipeline market. Transport lines primarily serve to move extracted oil or gas from offshore production platforms or drilling sites to onshore facilities or processing centers. These pipelines are the backbone of the offshore energy infrastructure, facilitating the transportation of raw oil or gas over long distances across the seabed to onshore refineries or distribution hubs. Export lines are specifically dedicated to transporting oil or gas from offshore production sites to other countries or distant markets. These pipelines often traverse international waters, enabling the export of oil or gas produced in one country to be transported to refineries or markets in other nations.

By Installation Type

Based on installation type, the global offshore pipeline market is divided into S-lay, J-lay, tow-in. The tow-in category dominates the market with the largest revenue share in 2022. The tow-in method involves towing pre-assembled pipelines from an onshore location or fabrication yard to the offshore installation site. Pipelines are fabricated onshore, floated, and then towed to the installation site using specialized vessels or tugboats. Once at the site, the pipelines are submerged and installed on the seabed. The S-lay method involves laying the pipeline onto the seabed in a continuous 'S' shape from the vessel. A specialized vessel, equipped with a stinger (an inclined structure), lowers the pipeline from the stern of the vessel onto the seabed. As the vessel moves forward, the pipeline forms an 'S' shape before settling on the seabed. The J-lay method involves constructing the pipeline in an upright 'J' shape on a specialized vessel before lowering it onto the seabed. This method utilizes a tower on the vessel's deck to fabricate the pipeline vertically. Once the pipeline is constructed, it is lowered or 'laid' onto the seabed in a near-vertical position.

By Depth

Based on the depth, the global offshore pipeline market is categorized into shallow water, deepwater. Shallow water pipelines are typically installed in water depths up to around 200 meters (approximately 656 feet). These pipelines are often situated closer to the coastline or continental shelves, where the water depth allows for easier installation and maintenance. Deepwater pipelines are installed in water depths greater than 200 meters (656 feet) and can extend to thousands of meters deep. These pipelines are situated in more remote offshore regions, far from the coastline, and often require more complex engineering and installation techniques due to the challenging depths and environmental conditions.

Global Offshore Pipeline Market Overview by Region

The global offshore pipeline market is categorized into North America, Europe, Asia-Pacific, and the Rest of the World. Europe emerged as the leading region, capturing the largest market share in 2022. The North Sea's substantial offshore oil and gas deposits, which serve as a hub for offshore energy extraction, are one of the main factors contributing to Europe's leadership. Large-scale offshore fields are found in nations like Norway, the UK, and the Netherlands, which motivates significant expenditures in pipeline infrastructure. A well-established network of pipelines links these offshore resources to onshore processing facilities and distribution networks, making the North Sea region a key player in the production of offshore energy. Additionally, pipeline improvements have been affected by Europe's strict environmental legislation and dedication to sustainability, which have encouraged the use of cutting-edge technologies and environmentally benign practices in pipeline construction and operation. In addition to raising safety standards, this emphasis on environmental stewardship has strengthened the area's standing for sustainable energy development. Furthermore, Europe's leadership in offshore pipeline projects may be attributed in large part to its advanced engineering know-how, technical innovation, and industry participants' combined efforts. Because of their combined knowledge, innovative techniques like J-lay and sophisticated subsea technologies have been put into practice, further establishing Europe as a leader in the offshore pipeline industry worldwide.

Global Offshore Pipeline Market Competitive Landscape

In the global offshore pipeline market, a few major players exert significant market dominance and have established a strong regional presence. These leading companies remain committed to continuous research and development endeavors and actively engage in strategic growth initiatives, including product development, launches, joint ventures, and partnerships. By pursuing these strategies, these companies aim to strengthen their market position, expand their customer base, and capture a substantial share of the market.

Some of the prominent players in the global offshore pipeline market include Saipem SpA, Enbridge Inc., Energy Transfer LP, TechnipFMC plc, McDermott International, Ltd, Sapura Energy Berhad, Atteris Pty Ltd, John Wood Group PLC, Fugro Group, and various other key players.

Global Offshore Pipeline Market Recent Developments

In November 2022, Sable Offshore Corp. is being represented by Bracewell LLP in relation to the acquisition of the Santa Ynez field in federal waters offshore California by Exxon Mobil Corporation, along with related onshore processing and pipeline assets, including pipeline assets that Exxon Mobil previously acquired from Plains Pipeline L.P.

Offshore Pipeline Market Report Segmentation

|

ATTRIBUTE |

DETAILS |

|

By Diameter |

|

|

By Product |

|

|

By Line Type |

|

|

By Installation Type |

|

|

By Depth |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Objectives of the Study

The objectives of the study are summarized in 5 stages. They are as mentioned below:

To identify and estimate the market size for the global offshore pipeline market segmented by diameter, by product, by line type, by installation type, by depth, region and by value (in U.S. dollars). Also, to understand the consumption/ demand created by consumers of offshore pipeline between 2019 and 2031.

To identify and infer the drivers, restraints, opportunities, and challenges for the global offshore pipeline market

To find out the factors which are affecting the sales of offshore pipeline among consumers

To identify and understand the various factors involved in the global offshore pipeline market affected by the pandemic

To provide a detailed insight into the major companies operating in the market. The profiling will include the financial health of the company's past 2-3 years with segmental and regional revenue breakup, product offering, recent developments, SWOT analysis, and key strategies.

Intended Audience

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.