Next Generation Advanced Battery Market Report: By Technology (Solid Electrolyte Battery, Magnesium Ion Battery, Next-Generation Flow Battery, Metal-Air Battery, Lithium-Sulfur Battery, and Other Technologies), End User (Consumer Electronics, Transportation, Industrial, Energy Storage, and Other), and Region (North America, Europe, Asia-Pacific, Latin America, Middle-East and Africa) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2024-2032.

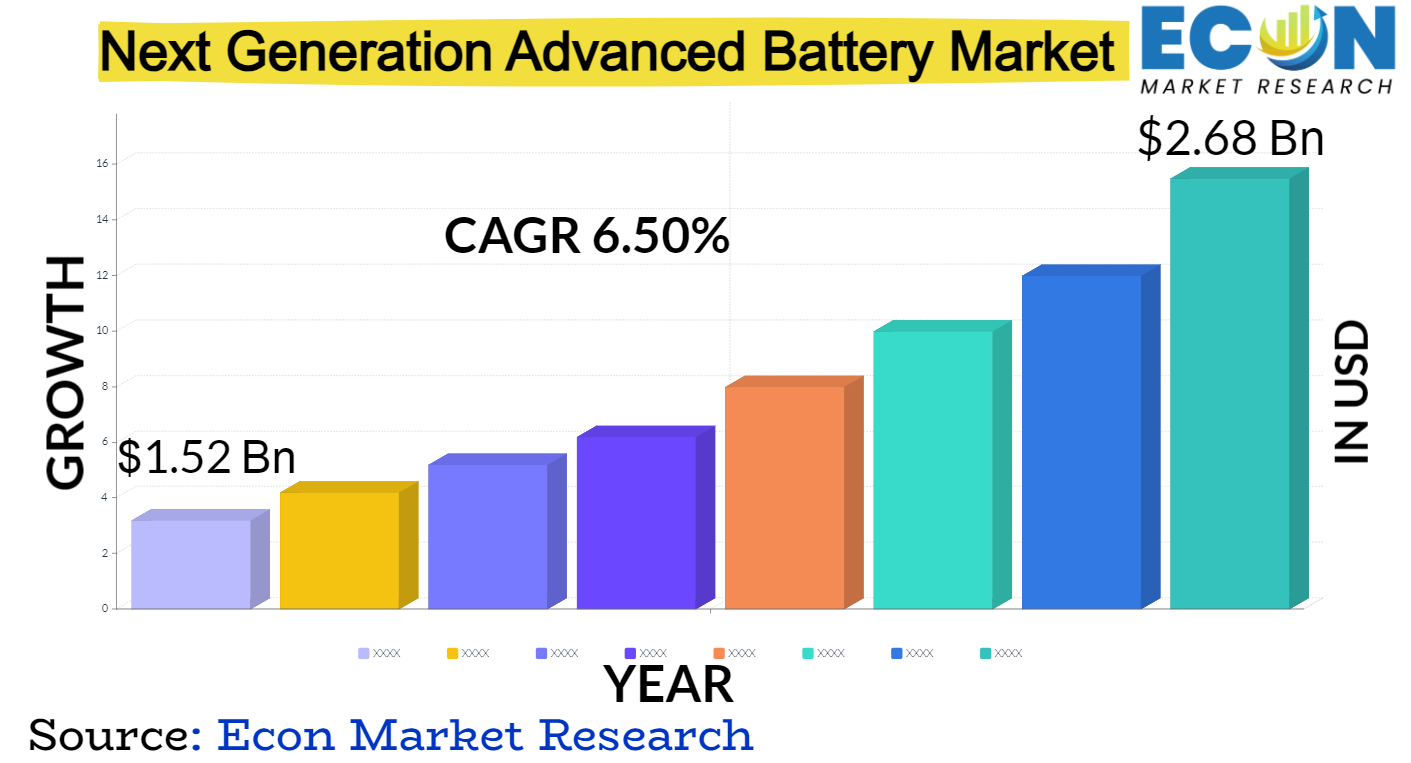

Global Next Generation Advanced Battery market is predicted to reach approximately USD 2.68 billion by 2032, at a CAGR of 6.50% from 2024 to 2032.

The innovative energy storage solutions offered by the global next-generation advanced battery market are tailored to meet the changing needs of different industries and applications. Compared to conventional battery technologies, these batteries offer better performance, a higher energy density, a longer lifespan, and improved safety features. They represent a paradigm shift in energy storage technology. Lithium-ion, solid-state, flow, sodium-ion, and several cutting-edge technologies like lithium-sulfur and lithium-air batteries are examples of next-generation advanced batteries. They are widely used in the grid energy storage, consumer electronics, electric vehicles, renewable energy systems, and aerospace industries, accelerating the shift to a more efficient and sustainable energy ecosystem.

The growing demand for electric vehicles, increased investments in renewable energy infrastructure, and consumer preference for portable electronic devices with longer battery lives are driving the market for next-generation advanced batteries to grow at a rapid pace. New developments in materials science, manufacturing techniques, and battery management systems are driving the creation of high-performance batteries that are more environmentally friendly and have better energy efficiency. Market expansion is, however, severely hampered by issues like high production costs, scarce raw material supply, and regulatory restrictions. Industry participants are concentrating on research and development projects, strategic alliances, and collaborations to improve battery performance, scalability, and affordability in order to take advantage of new opportunities and get past these obstacles.

Global Next Generation Advanced Battery Report Scope and Segmentation

|

Report Attribute |

Details |

|

Estimated Market Value (2023) |

USD 1.52 billion |

|

Projected Market Value (2032) |

USD 2.68 billion |

|

Base Year |

2023 |

|

Forecast Years |

2024 – 2032 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- Based on By Technology, By End-Use, & Region. |

|

Segments Covered |

By Technology, By End-Use, & By Region. |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2024 to 2032. |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others. |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Next Generation Advanced Battery Dynamics

The market is driven by the growing global demand for electric vehicles (EVs), which is being fueled by initiatives to lessen dependency on fossil fuels and greenhouse gas emissions. Furthermore, the adoption of next-generation batteries for energy storage applications is being fueled by developments in grid modernization and renewable energy integration, which are assisting in the shift to sustainable power generation and distribution systems. Furthermore, the demand for high-performance batteries with longer lifespans and faster charging capabilities is being fueled by the proliferation of portable electronic devices as well as the growing popularity of wearables, smartphones, and Internet of Things devices.

However, the market faces several challenges that impact its growth trajectory. One significant obstacle is the high production costs associated with next-generation advanced batteries, stemming from the complexity of manufacturing processes and the limited availability of key raw materials such as lithium, cobalt, and nickel. Furthermore, concerns regarding battery safety, including the risk of thermal runaway and fire hazards, pose regulatory and operational challenges for manufacturers and end-users alike. Additionally, geopolitical tensions and supply chain disruptions related to raw material sourcing and trade policies can affect market stability and hinder the scalability of battery production.

Next Generation Advanced Battery Drivers

The rapid adoption of electric vehicles (EVs) globally is a significant driver propelling the next-generation advanced battery market. Governments worldwide are implementing stringent emission regulations and providing incentives to accelerate the transition from internal combustion engine vehicles to electric alternatives. Next-generation batteries, such as lithium-ion and solid-state batteries, offer higher energy densities and longer driving ranges, addressing key concerns regarding EV performance and range anxiety. As automakers invest heavily in EV production and infrastructure development expands, the demand for advanced batteries is expected to soar, driving market growth and innovation in battery technology.

In order to reduce intermittency and enhance grid stability, there is a growing need for energy storage solutions due to the growing use of renewable energy sources like solar and wind power. By storing excess electricity during times of high generation and delivering it when demand peaks or renewable output declines, next-generation advanced batteries are essential to the effective integration and utilisation of renewable energy.

Large-scale energy storage solutions are anticipated to become more in demand as governments and utilities around the world invest in modernising grid infrastructure and increasing renewable energy capacity. This will present profitable opportunities for battery suppliers and manufacturers to take advantage of the expanding renewable energy market.

Restraints:

The high production costs involved in producing advanced battery technologies are one of the main obstacles impeding the market for next-generation advanced batteries. Advanced battery production involves intricate manufacturing processes and substantial investments in R&D, infrastructure, and manufacturing techniques for batteries like lithium-ion and solid-state.

Furthermore, the market is highly reliant on rare raw materials such as nickel, cobalt, and lithium, whose prices are volatile and vulnerable to geopolitical risks. Consequently, producers encounter difficulties in attaining cost competitiveness and maintaining a steady supply chain, potentially impeding market expansion and restricting the extensive integration of cutting-edge battery technologies.

Another significant restraint facing the next-generation advanced battery market is the persistent concern over battery safety and regulatory compliance. High-profile incidents of battery fires and safety recalls have raised public awareness and regulatory scrutiny regarding the safety standards of advanced battery technologies, particularly in applications such as electric vehicles and grid energy storage.

Regulatory agencies are imposing stricter safety requirements and certification processes for battery manufacturers, increasing compliance costs and time-to-market for new products. Moreover, concerns over the environmental impact of battery disposal and recycling further complicate regulatory compliance and sustainability efforts within the industry. Addressing these safety concerns and navigating evolving regulatory landscapes pose significant challenges for market participants, potentially slowing down market expansion and innovation in advanced battery technologies.

Opportunities:

The market for next-generation advanced batteries offers significant chances for innovation and technological breakthroughs in a number of industries. Innovation in materials science, manufacturing processes, and battery management systems is being driven by research and development initiatives aimed at enhancing battery performance, energy density, and lifespan.

New battery technologies with promise for improved safety, sustainability, and efficiency include sodium-ion batteries, solid-state batteries, and advanced electrode materials. New developments in battery technology are anticipated to open doors for market expansion and differentiation as industry players work together and allocate resources towards research-driven innovation. This will facilitate the creation of next-generation energy storage solutions for a variety of applications.

Segment Overview

The market is segmented based on different battery technologies, including solid electrolyte batteries, magnesium-ion batteries, next-generation flow batteries, metal-air batteries, lithium-sulfur batteries, and other emerging technologies. Solid electrolyte batteries utilize solid-state electrolytes instead of liquid or gel electrolytes, offering enhanced safety and energy density. Magnesium-ion batteries, an alternative to lithium-ion batteries, leverage magnesium as the charge carrier, promising higher energy density and lower cost.

Next-generation flow batteries employ redox reactions to store and release energy, making them suitable for grid-scale energy storage applications. Metal-air batteries utilize metal and oxygen reactions for energy conversion, offering high energy densities but facing challenges in rechargeability. Lithium-sulfur batteries offer higher energy densities compared to lithium-ion batteries, with potential applications in electric vehicles and aerospace. Other emerging technologies explore novel materials and chemistries to enhance battery performance, durability, and sustainability, driving innovation and competitiveness in the market.

The market is also segmented based on end-user applications, including consumer electronics, transportation, industrial, energy storage, and other sectors. Consumer electronics represent a significant market segment for next-generation advanced batteries, driven by demand for longer battery life, faster charging, and lightweight solutions for smartphones, laptops, wearables, and other portable devices. Transportation, particularly electric vehicles (EVs), is a key growth segment for advanced batteries, with increasing adoption fueled by environmental regulations and consumer preferences for sustainable mobility solutions.

Industrial applications encompass a wide range of sectors, including aerospace, marine, and robotics, requiring high-performance batteries for power backup, propulsion, and auxiliary systems. Energy storage applications encompass grid-scale installations, residential and commercial systems, and off-grid solutions, supporting renewable energy integration, grid stabilization, and peak load management. Other sectors include niche applications such as military, medical devices, and aerospace, which require specialized battery solutions tailored to unique performance and safety requirements.

Next Generation Advanced Battery Overview by Region

North America stands as a key hub for battery technology development and adoption, driven by robust research and development initiatives, government incentives for electric vehicles and renewable energy, and a strong presence of leading battery manufacturers and automotive companies. The region's focus on sustainability and energy independence further accelerates the demand for advanced battery solutions across diverse applications, including electric transportation, grid-scale energy storage, and consumer electronics.

In Europe, stringent environmental regulations and ambitious clean energy targets propel the adoption of next-generation advanced batteries to support the region's transition towards a low-carbon economy. Government subsidies, favorable policies, and collaborative efforts between industry stakeholders and research institutions foster innovation and investment in battery technology, particularly in electric mobility and renewable energy storage projects. Additionally, the European Union's emphasis on reducing greenhouse gas emissions and promoting sustainable transportation fuels the demand for electric vehicles equipped with advanced battery systems, driving market growth and competitiveness.

Asia-Pacific emerges as a prominent player in the next-generation advanced battery market, fuelled by the region's burgeoning automotive industry, rapid urbanization, and expanding renewable energy sector. Countries like China, Japan, and South Korea lead in battery production, research, and development, leveraging technological expertise, government support, and economies of scale to drive down costs and enhance battery performance. The region's growing population, rising disposable income levels, and increasing awareness of environmental issues stimulate demand for electric vehicles and energy storage solutions, creating lucrative opportunities for battery manufacturers and suppliers to penetrate diverse end-user markets effectively.

Next Generation Advanced Battery Market Competitive Landscape

Established companies such as Panasonic Corporation, LG Chem Ltd., and Samsung SDI Co., Ltd., leverage their technological expertise, manufacturing capabilities, and global presence to maintain leadership positions and drive innovation in lithium-ion batteries for electric vehicles, consumer electronics, and energy storage applications. These industry giants invest heavily in research and development initiatives to enhance battery performance, safety, and sustainability while optimizing production processes to achieve economies of scale and cost competitiveness.

Moreover, emerging players and startups, including QuantumScape Corporation, Solid Power Inc., and Sila Nanotechnologies Inc., are disrupting the market with breakthrough technologies such as solid-state batteries, silicon-based anodes, and advanced electrode materials. These innovators attract substantial investments from venture capitalists, strategic partners, and government agencies, accelerating the commercialization and adoption of next-generation battery solutions across diverse industries and applications. Collaborative partnerships, joint ventures, and strategic alliances are common strategies employed by both established players and startups to expand market reach, access new markets, and leverage complementary capabilities in materials science, manufacturing, and supply chain management.

Next Generation Advanced Battery Market Leading Companies:

GS Yuasa Corporation

Pathion Inc.

PolyPlus Battery Company Inc.

Oxis Energy Ltd

Samsung SDI Co. Ltd.

Sion Power Corporation

LG Chem Ltd.

Saft Groupe SA

Contemporary Amperex Technology Co. Ltd. (CATL)

BrightVolt

GP Batteries International Limited

Ion Storage Systems

NGK Insulators

Next Generation Advanced Battery Recent Developments

Global Next Generation Advanced Battery Report Segmentation

|

ATTRIBUTE |

DETAILS |

|

By Technology |

|

|

By End User |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.

+1 812 506 4440

+1 812 506 4440

+91 7875074426

+91 7875074426