Global Liquid Insulation Material Market Report: By Type (Mineral Insulating Oil, Synthetic Insulating Oil, Vegetable Oil and Silicone Oil), By Application (Electric, Motor, and Others), and Region (North America, Europe, Asia-Pacific, Latin America, Middle-East and Africa) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2024-2032.

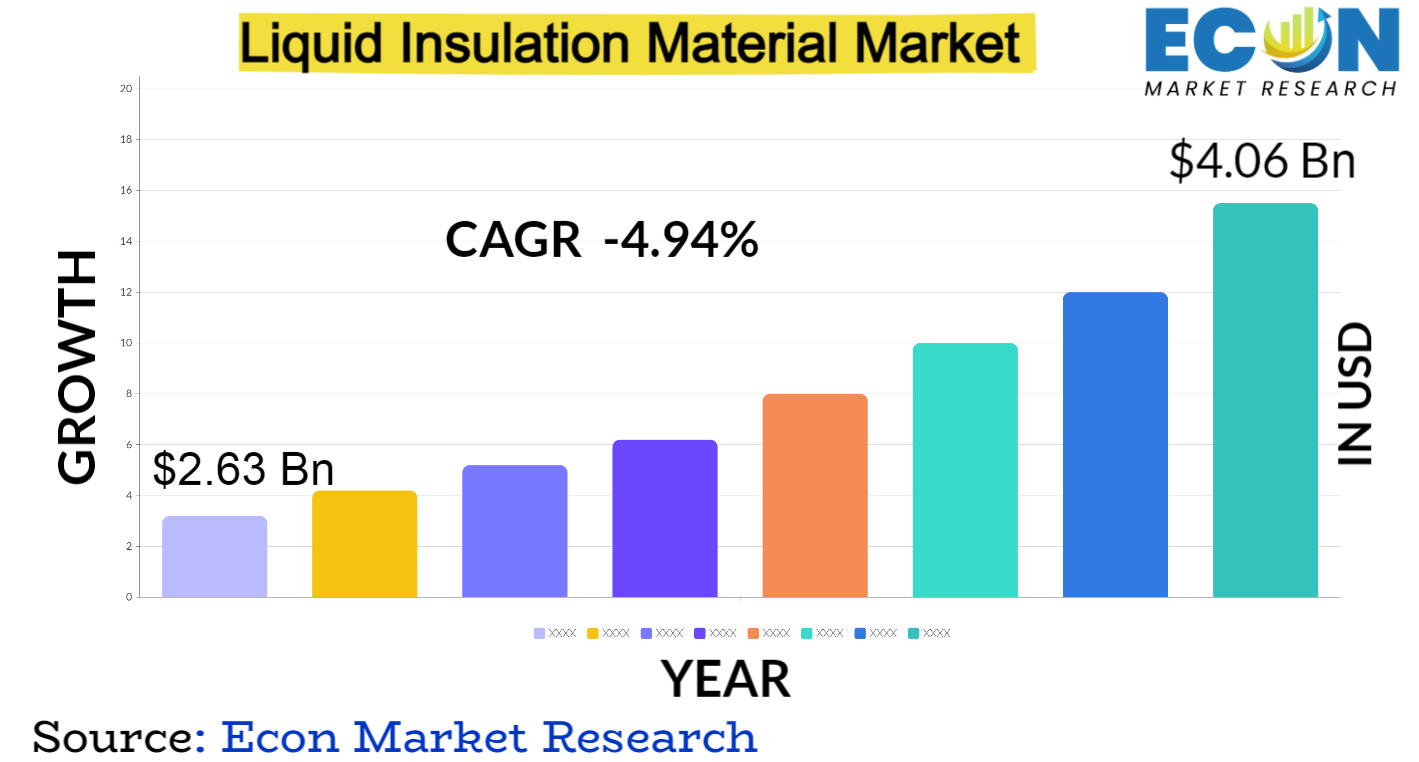

Global Liquid Insulation Material Market is predicted to reach approximately USD 4.06 billion by 2032, at a CAGR of 4.94% from 2024 to 2032.

Liquid insulation materials, sometimes referred to as insulating paints or coatings, are a cutting-edge category of goods that offer surfaces a seamless protective layer that resists corrosion and provides thermal insulation. These materials' remarkable insulating qualities are a result of their composition of ceramic microspheres and sophisticated polymers. Since liquid insulation materials are an affordable and adaptable substitute for conventional insulation techniques, they are widely used in a variety of industries, including electronics, automotive, aerospace, and construction.

|

Report Attribute |

Details |

|

Estimated Market Value (2023) |

USD 2.63 billion |

|

Projected Market Value (2032) |

USD 4.06 billion |

|

Base Year |

2023 |

|

Forecast Years |

2024 – 2032 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- Based on By Type, By Application, & Region. |

|

Segments Covered |

By Type, By Application, & By Region. |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2023 to 2032. |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others. |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Global energy efficiency regulations and growing public awareness are major motivators for industries looking for cutting-edge insulation solutions. Because they offer seamless corrosion resistance and thermal protection, liquid insulation materials are becoming more and more popular in a variety of industries. The demand for these materials is particularly high in the construction sector because they provide a space-saving, lightweight substitute for conventional insulating techniques.

In this market, innovation and ongoing product development are critical factors that shape the dynamics. Producers are allocating significant resources towards research and development in order to launch formulas that not only improve insulation qualities but also address particular industry requirements. The utilisation of liquid insulation materials for heat dissipation management is being encouraged by the automotive industry's growing emphasis on sustainability and fuel efficiency.

An important factor propelling the worldwide market for liquid insulation materials is the growing emphasis on sustainability and energy efficiency. Innovative insulation solutions are being adopted by industries due to stringent regulations and initiatives to reduce carbon footprints. A viable option for improving thermal efficiency in industrial processes, vehicles, and buildings is to use liquid insulation materials. The ability of liquid insulation materials to support environmental sustainability and energy conservation is expected to drive demand for these materials as governments around the world continue to tighten energy performance standards.

Innovations in liquid insulation materials and ongoing technological advancements are driving the market. In order to enhance these materials' performance attributes—such as increased heat conductivity, durability, and application ease—manufacturers are spending in R&D. The market's reach is further increased by the continuous efforts to develop bio-based liquid insulation materials, which are in line with consumers' increasing desire for environmentally friendly and sustainable solutions. Formulations that are innovative and tailored to industry needs—like those in the automotive and construction sectors—are important forces behind market dynamics and increased adoption in a variety of applications.

The comparatively higher initial costs of these advanced materials are one of the main obstacles to the market for liquid insulation materials. Even though there will be significant long-term energy savings, the initial costs could be prohibitive, particularly for small businesses and cost-sensitive markets. Furthermore, the application of liquid insulation materials requires expertise, which may raise the project's overall cost. Expanding market penetration requires removing these financial obstacles and attending to the requirement for specialised training.

Market expansion is hampered by a lack of knowledge about the uses and advantages of liquid insulation materials. It's possible that many end users are unaware of the benefits these materials provide in terms of sustainability, corrosion resistance, and thermal insulation. To overcome this obstacle, raising awareness through focused marketing and educational programmes is crucial. Furthermore, it might take coordinated efforts to highlight the better performance and adaptability of liquid insulation materials in areas where there are well-established preferences for traditional insulation techniques in order to achieve market penetration in those areas.

The growing emphasis on fuel economy and sustainability in the automotive industry presents liquid insulation materials with a bright future. The use of cutting-edge insulation solutions becomes essential as automakers work to lighten vehicles and increase energy efficiency. Because they are compact and lightweight, liquid insulation materials can help automobiles regulate their heat better. Developing customised solutions in partnership with automakers and taking part in the expanding electric vehicle market further expands the opportunities for growth in this industry.

The liquid insulation material market is segmented based on the type of insulation oil, encompassing mineral insulating oil, synthetic insulating oil, vegetable oil, and silicone oil. Mineral insulating oil, derived from petroleum, has been a traditional choice due to its good dielectric properties and cost-effectiveness. Synthetic insulating oil, on the other hand, is a result of advanced chemical processes, offering improved performance characteristics such as higher thermal stability and reduced environmental impact. Vegetable oil, often sourced from renewable plant-based materials, represents a growing trend towards eco-friendly insulation options, appealing to industries emphasizing sustainability. Silicone oil, with its excellent electrical insulation properties and resistance to temperature extremes, is gaining traction as a high-performance alternative in various applications. The diverse range of liquid insulation types caters to different industry needs, providing a spectrum of choices based on performance, environmental considerations, and specific use cases.

The application segment of the liquid insulation material market encompasses electric, motor, and other uses. In the electric sector, these materials play a vital role in insulating electrical components, ensuring the safety and efficiency of power transmission and distribution systems. The motor application involves the use of liquid insulation materials to enhance the performance and reliability of electric motors, reducing heat dissipation and improving overall efficiency. The "other" category encompasses a wide array of applications across industries, including but not limited to transformers, capacitors, and electronic devices. The versatility of liquid insulation materials allows for their application in diverse settings, contributing to thermal management and preventing electrical breakdown. As industries continue to seek energy-efficient solutions, the adoption of liquid insulation materials across these varied applications is driven by the need for effective thermal protection, durability, and adherence to sustainability goals. The segmentation by application reflects the adaptability of liquid insulation materials to a broad spectrum of electrical and mechanical systems, positioning them as integral components in the pursuit of enhanced performance and energy efficiency across industries.

North America has been a major player in the market thanks to its sophisticated infrastructure and emphasis on energy efficiency. Liquid insulation materials are becoming more widely used, particularly in the building and automotive industries, thanks to the region's dedication to sustainable practices. Europe follows suit, with stricter environmental laws and a rising preference for environmentally friendly products helping to drive market growth. The market for liquid insulation materials is further driven by the European Union's aggressive climate goals and emphasis on lowering carbon emissions, especially for materials made from renewable resources like vegetable oil.

In the Asia-Pacific region, rapid industrialization, urbanization, and the need for modernized infrastructure are fuelling the market growth. Countries such as China and India are witnessing increased investments in construction and energy-efficient technologies, providing significant opportunities for liquid insulation material manufacturers. Additionally, the rising automotive production in the region, coupled with a growing awareness of sustainable practices, is boosting the adoption of these materials.

The market is dominated by well-known corporations like Cargill, ABB, Hitachi, and JOOYN, which place a high priority on R&D to bring innovative formulations and technologies. These leaders in the field concentrate on improving the performance attributes of liquid insulation materials, like increased heat conductivity, decreased environmental impact, and application versatility.

The market also witnesses the active participation of niche and emerging players, contributing to the overall competitiveness. These companies often specialize in specific types of liquid insulation materials or cater to niche applications within industries. The competitive dynamics are further intensified by collaborations and partnerships between manufacturers and end-users, aiming to develop customized solutions that meet specific industry requirements. Additionally, a growing trend in the market is the incorporation of bio-based liquid insulation materials, with companies like Cargill and Nynas AB leading the charge towards environmentally friendly alternatives.

|

ATTRIBUTE |

DETAILS |

|

By Type |

|

|

By Application |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

The objectives of the study are summarized in 5 stages. They are as mentioned below:

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.