HVAC Chillers Market Size, Share, Trends, Growth, and Industry Analysis, By Operation Type (Vapor Compression Chillers, Vapor Absorption Chillers), By Condenser Type (Water Cooled, Air Cooled, Evaporative), By Application (Residential, Commercial, Industrial) and Regional Insights and Forecast to 2032

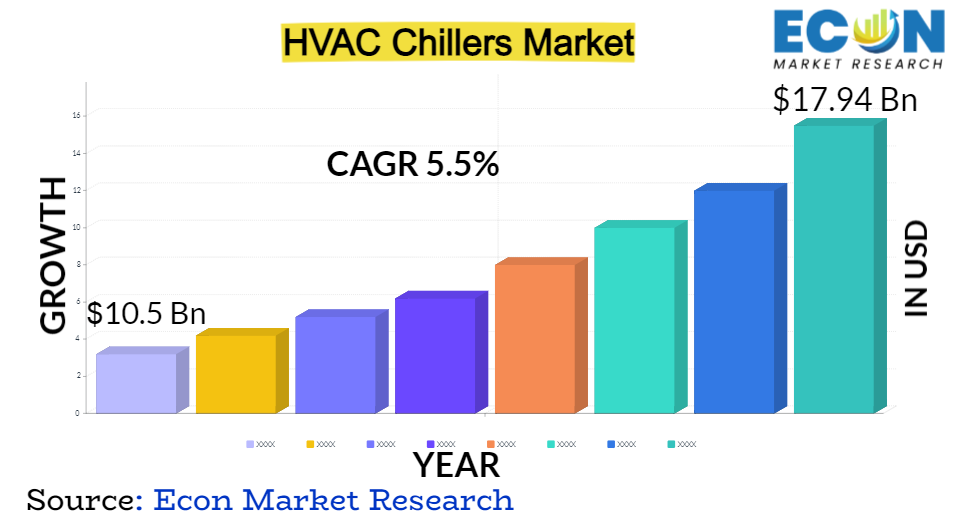

Global HVAC Chillers Market size was USD 10.5 billion in 2022 and is predicted to reach USD 17.94 billion in 2032, exhibiting at a CAGR of 5.5% during the forecast period.

HVAC Chillers play a crucial role in maintaining the required temperature of any space, machinery, equipment, etc. HVAC Chillers remove the heat and transfer it somewhere else, and make it cool. These chillers can be utilized in numerous residential spaces, for example, small to large rooms, garages, basements, and crawlspaces. The popularity of HVAC chillers is increasing due to various advantages such as portability, convenience, and quick and easy maintenance. Moreover, the adoption of HVAC chillers is rising in restaurants, hotels, kitchens, and dining rooms to handle concerns regarding temperature levels. Other industry verticals where these chillers are used are rubber, petrochemicals, medical, plastic, commercial office buildings, industrial, sports venues, etc.

The increase in demand for district cooling systems in many industries and high-rise buildings is expected to boost the HVAC chillers market's growth during the forecast period. District cooling, also known as centralized generation and distribution of cooling energy, replaces traditional air-cooling systems as it is less expensive and more energy efficient. Moreover, developments in the tourism industry boost the construction of hotels and public infrastructure where HVAC chillers can be used on a large scale. Furthermore, as these chillers are widely used in cooling and ventilation of skyscrapers, the growth of skyscrapers is expected to fuel the growth of the HVAC chillers market opportunity.

Chillers from Arctic Chiller Group, Ltd. are installed in high-end residential complexes throughout North America and serve as the primary air-conditioning system. The Arctic Chiller Group also serves skating facilities across the United States and Canada, through direct ice freezing, ice rink cooling, and chiller maintenance. The expanding aviation industry, as well as the growing number of new commercial construction buildings, drive demand for respective chillers. As a result, demand for the respective chillers is expected to rise. Screw chillers are vapour compressor chillers that make use of a screw compressor for transporting the coolant through the system. These chillers are suitable for high-rise buildings considering their quiet operation, compact installation, high energy efficiency, and lower maintenance costs. With a growing real estate sector all over the world, the requirement for screw chillers is forecast to increase remarkably.

COVID-19 Impact

The COVID-19 pandemic impact has had a significant impact on the HVAC chillers market. The market for chillers is largely driven by demand from the commercial, industrial, and residential sectors, which were all impacted by the pandemic. In the initial stages of the pandemic, many businesses and industrial operations were shut down or operating at reduced capacities, resulting in lower demand for chillers. The construction industry, which is a significant user of chillers, also experienced a slowdown due to supply chain disruptions and labour shortages.

As businesses and industries started to reopen and resume operations, the demand for chillers began to recover. In particular, there has been an increased demand for HVAC systems that improve indoor air quality, which has become a top priority for many businesses and building owners due to concerns about the spread of the virus. Chillers are a key component of such systems and are used to control the temperature and humidity of indoor spaces. The trend towards remote work and online shopping has increased the demand for data centers, which require large amounts of cooling to prevent equipment from overheating. This has led to an increase in the demand for chillers in the data center industry.

REPORT SCOPE & SEGMENTATION:

|

Report Attribute |

Details |

|

Projected Market Value (2031) |

17.94 Billion |

|

Estimated Market Value (2022) |

10.5 Billion |

|

Base Year |

2023 |

|

Forecast Years |

2024 - 2032 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- Operation, Condenser, Application, Region |

|

Segments Covered |

By Operation Type, By Condenser Type, By Application, and Region |

|

Forecast Units |

Value (USD Billion), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2024 to 2032 |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, and Rest of World |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis, and COVID-19 impact analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Segment Analysis

The hvac chillers market is segmented by Operation Type, Condenser Type, and by Application type.On the basis of operation type, the market is segmented into two categories: vapor compression chillers and vapor absorption chillers. On the basis of condenser type, the market is also segmented into two categories: water-cooled, air-cooled, and evaporative. On the basis of application, the market is classified into residential, commercial, industrial, and other. On the basis of region, the global market analysis is conducted across North America (the U.S., Canada, and Mexico), Europe (UK, France, Germany, Italy, and the Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Indonesia, Thailand, Taiwan, and the Rest of Asia-Pacific), and LAMEA (Latin America, the Middle East, and Africa).

Recent Key Developments

Variable-speed chillers are gaining popularity in the market because they provide greater energy efficiency and control over the cooling process. These chillers can adjust their cooling capacity in response to changing conditions, resulting in energy savings and improved performance.

Natural refrigerants such as ammonia, carbon dioxide, and hydrocarbons are increasingly being used in chillers instead of traditional synthetic refrigerants such as chlorofluorocarbons (CFCs) and hydrofluorocarbons (HFCs). Natural refrigerants have a lower impact on the environment and can help to reduce greenhouse gas emissions.

The chillers are increasingly being integrated with building automation systems to optimize their performance and reduce energy consumption. This enables the regulation of chillers based on real-time building data, such as occupancy levels and exterior temperature, leading to higher energy savings and increased occupant comfort.

The Air-cooled chillers are becoming more popular in the market due to lower installation and maintenance costs compared to water-cooled chillers. They are also more suitable for smaller spaces and buildings, making them a popular choice for the commercial and residential applications.

Smart chillers, which use artificial intelligence (AI) and machine learning algorithms to optimize their performance, are gaining more popularity in the market. These chillers can predict and prevent potential maintenance issues, optimize energy consumption, and improve the overall efficiency of the cooling systems.

Regional Analysis

Asia-Pacific is the largest growing market. China and Japan contribute the most to the HVAC chillers market. Growing focus on the construction of skyscrapers in China and Japan has increased awareness about chilled water-cooled systems and is offering new opportunities to drive demand in the region.

The other regions of the North American chiller market include the US and Canada. As urbanisation and economic growth have increased, so has the building of theatres, hospitals, offices, and massive retail establishments. The development of smart cities and the expansion of airport infrastructure is supported by the governments of the countries in North America. As a result, the need for chillers in the region's residential, commercial, and industrial sectors is being driven by an increase in tourism, smart city initiatives, and construction activities. To increase the bar for energy efficiency, the US Department of Energy (DOE) is investing heavily nationwide.

Competitor Analysis

To increase their consumer base, businesses innovate and offer new products. Also, important businesses are implementing the merger and acquisition strategy to increase their market revenue on a global scale. The following are a few of the leading key players in the HVAC chillers market:

Market Segmentation

Operation Type

Condenser Type

Application

Regions Covered

Customization Scope

Pricing

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.

+1 812 506 4440

+1 812 506 4440

+91 7875074426

+91 7875074426