Global Flow Battery Market Report: By Type (Redox and Hybrid), Material (Vanadium, Zinc Bromine, Iron and Others), Storage (Large Scale and Small Scale), Application (Grid/Utility, Commercial & Industrial, EV Charging Stations and Residential), and Region (North America, Europe, Asia-Pacific, Latin America, Middle-East and Africa) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2024-2032.

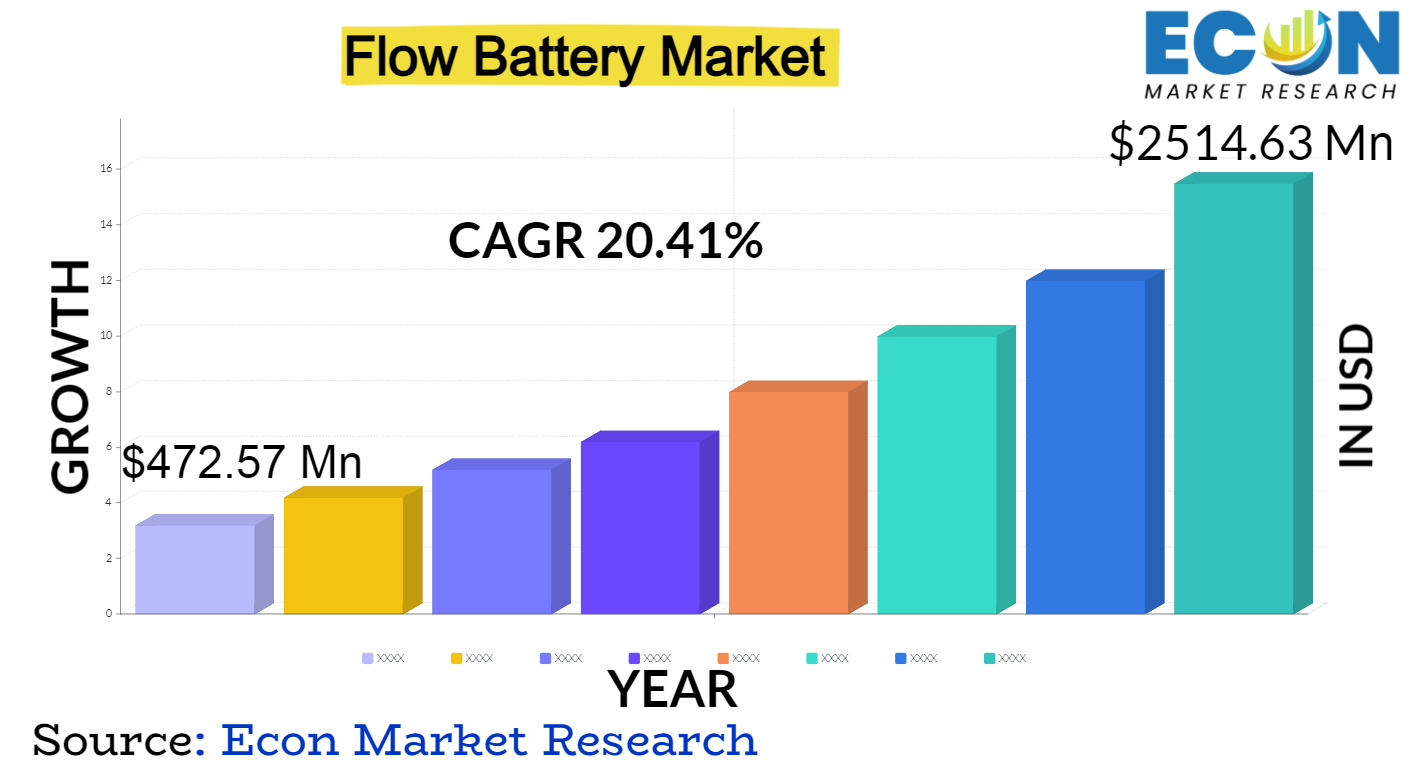

Global Flow Battery market is predicted to reach approximately USD 2,514.63 million by 2032, at a CAGR of 20.41% from 2024 to 2032.

The Global Flow Battery Market is a burgeoning sector within the renewable energy industry characterized by rechargeable batteries that employ a liquid electrolyte to store energy. These batteries store energy through the chemical reaction between two electrolyte solutions, separated by a membrane, which allows for the flow of ions and the release of electricity. With rising concerns about environmental sustainability and the need for reliable energy storage solutions, the global flow battery market has witnessed significant growth and innovation in recent years. The market encompasses various types of flow batteries, including redox flow batteries, vanadium redox flow batteries, and zinc-bromine flow batteries, each with unique advantages and applications.

Government programmes to cut carbon emissions, rising investments in renewable energy projects, and rising demand for off-grid power and grid stabilisation are the main factors propelling the market's expansion. Flow batteries are superior to conventional lithium-ion batteries in several ways, including increased safety features, scalability, and a longer cycle life. For these reasons, they are the best choice for stationary energy storage applications in microgrids, utility-scale energy projects, and the integration of renewable energy sources. Furthermore, improvements in battery technology and manufacturing techniques have lowered costs and increased performance, which has fueled market growth even more.

Key market players are actively investing in research and development to enhance battery efficiency, increase energy density, and reduce manufacturing costs, driving innovation and product differentiation. Additionally, strategic collaborations, partnerships, and acquisitions among industry players are fostering technological advancements and market penetration. However, challenges such as limited energy density, high initial capital investment, and regulatory constraints pose potential barriers to market growth.

Global Flow Battery report scope and segmentation.

|

Report Attribute |

Details |

|

Estimated Market Value (2023) |

USD 472.57 million |

|

Projected Market Value (2032) |

USD 2,514.63 million |

|

Base Year |

2023 |

|

Forecast Years |

2024 – 2032 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- Based on By Type, By Material, By Storage, By Application, & Region. |

|

Segments Covered |

By Type, By Material, By Storage, By Application, & By Region. |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2024 to 2032. |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others. |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Global Flow Battery dynamics

The increasing adoption of renewable energy sources, driven by concerns over climate change and energy security, is a significant driver of market growth. Governments worldwide are implementing policies and incentives to promote the integration of renewable energy into the grid, creating opportunities for flow battery deployment as a means of storing intermittent renewable energy and stabilizing the grid.

Furthermore, the dynamics of the market are being shaped by developments in flow battery technology and technological advancements. The goals of ongoing research and development are to lower manufacturing costs, increase energy density, and improve battery efficiency. These developments are making flow batteries more competitive with respect to conventional lithium-ion batteries, especially in stationary energy storage applications where safety and scalability are critical.

Furthermore, flow batteries are becoming more and more popular as a dependable and adaptable energy storage option due to the growing need for grid modernization and the growth of microgrid networks. Flow batteries are ideal for grid stabilisation and peak shaving applications because of their many benefits, including a long cycle life, quick response times, and the capacity to function in challenging environments.

Global Flow Battery drivers

The global push towards reducing carbon emissions and transitioning to renewable energy sources is a primary driver for the flow battery market. Governments worldwide are implementing ambitious renewable energy targets and incentives to accelerate the adoption of solar, wind, and other renewables. Flow batteries play a crucial role in this transition by offering efficient energy storage solutions that can store excess renewable energy generated during peak production periods and discharge it during periods of high demand or low renewable generation. As renewable energy penetration increases, the demand for reliable and scalable energy storage solutions like flow batteries is expected to grow substantially.

Flow battery costs are declining as a result of ongoing technological advancements, manufacturing innovations, and economies of scale. Efforts in research and development aimed at boosting cycle life, raising energy density, and improving battery efficiency are making flow batteries more competitive with conventional lithium-ion batteries. Furthermore, production is being streamlined and overall system costs are being decreased due to advancements in materials and manufacturing techniques. Flow batteries are being evaluated for a variety of uses, such as off-grid electrification projects, commercial and industrial backup power, and grid-scale energy storage, as they become more affordable and efficient.

Restraints:

Despite recent cost reductions, flow batteries still require significant upfront investment compared to traditional energy storage technologies. The high initial capital costs associated with flow battery systems can be a barrier to adoption, particularly for smaller-scale projects and developing markets with limited access to financing. Additionally, the long payback periods associated with flow battery investments may deter potential investors and project developers, especially in regions with uncertain regulatory environments or volatile energy markets.

The comparatively low energy density of flow batteries is one of their main drawbacks when compared to other energy storage technologies. Flow batteries are superior to lithium-ion batteries in applications that need frequent cycling and long-term energy storage, but they usually have lower specific energy and energy density. Because of this drawback, flow batteries are less appropriate for uses like consumer electronics or electric cars that call for small or high-energy-density storage solutions. Furthermore, there may be logistical and operational difficulties when scaling up flow battery systems to meet the energy storage needs of large-scale grid applications. These difficulties may include supply chain issues, system integration difficulties, and restrictions on land use.

Opportunities:

The increasing need for grid modernization and resilience presents a significant opportunity for the flow battery market. Aging grid infrastructure, coupled with the growing frequency and severity of extreme weather events, has heightened the importance of deploying flexible and resilient energy storage solutions to enhance grid stability and reliability. Flow batteries offer advantages such as rapid response times, long cycle life, and the ability to provide both power and energy services, making them well-suited for supporting grid modernization efforts, integrating renewable energy resources, and enhancing grid resilience against disruptions and blackouts.

Segment Overview

The segmentation by type distinguishes between different flow battery architectures, namely redox and hybrid flow batteries. Redox flow batteries utilize chemical reactions between two electrolyte solutions separated by a membrane to store and release energy. Hybrid flow batteries combine features of redox flow batteries with other types of energy storage systems to enhance performance and efficiency. The type segmentation allows for tailored solutions catering to diverse energy storage requirements and operational environments.

Segmentation by material highlights the variety of electrolyte compositions used in flow batteries. Common materials include vanadium, zinc bromine, iron, and other proprietary electrolyte formulations. Each material offers unique properties and advantages in terms of energy density, stability, cost-effectiveness, and environmental impact. Material segmentation enables stakeholders to choose the most suitable electrolyte chemistry based on specific project requirements, performance objectives, and economic considerations.

The storage segmentation categorizes flow battery systems based on their storage capacity and application scale, distinguishing between large-scale and small-scale deployments. Large-scale storage solutions are typically deployed in utility-scale energy projects, grid stabilization initiatives, and commercial or industrial applications requiring extensive energy storage capacities. In contrast, small-scale storage systems cater to residential, community-level, and distributed energy storage applications, offering flexibility, modularity, and scalability to meet varying energy demands and operational constraints.

Segmentation by application reflects the diverse use cases and end-user segments driving demand for flow battery technology. Grid/utility applications encompass grid stabilization, peak shaving, load shifting, and renewable energy integration initiatives undertaken by utilities, grid operators, and energy service providers. Commercial and industrial applications include backup power, demand charge management, and facility-wide energy management systems deployed in commercial buildings, manufacturing facilities, and data centers. EV charging stations leverage flow battery technology to support rapid charging infrastructure, optimize grid interactions, and enhance reliability and resilience. Residential applications focus on off-grid electrification, energy self-sufficiency, and backup power solutions for households and small businesses, enabling consumers to reduce electricity costs, enhance energy security, and minimize environmental footprint.

Global Flow Battery Overview by Region

North America stands as a leading market for flow batteries, fuelled by robust investments in renewable energy projects, grid modernization initiatives, and supportive regulatory frameworks promoting energy storage deployment. The region's emphasis on sustainability, coupled with the integration of intermittent renewable energy sources like wind and solar, drives the demand for grid-scale energy storage solutions, positioning flow batteries as a key technology for grid stability and resilience.

In Europe, stringent environmental regulations, ambitious renewable energy targets, and increasing investments in clean energy technologies drive the adoption of flow batteries for renewable energy integration, grid optimization, and ancillary services provision. Government incentives and subsidies further stimulate market growth, fostering collaborations between industry stakeholders and research institutions to drive technological innovation and market expansion.

Asia Pacific emerges as a rapidly growing market for flow batteries, driven by rapid urbanization, industrialization, and escalating energy demand in countries like China, India, and Japan. Government initiatives promoting renewable energy deployment, energy storage incentives, and grid modernization efforts support the adoption of flow batteries in utility-scale projects, microgrids, and off-grid electrification initiatives across the region. Additionally, the presence of leading flow battery manufacturers and suppliers, coupled with advancements in battery technology and manufacturing processes, accelerates market penetration and competitiveness in the Asia Pacific region.

Global Flow Battery market competitive landscape

Key players such as ESS Inc., Vionx Energy Corporation, Redflow Limited, and UniEnergy Technologies dominate the market with their extensive product portfolios, technological expertise, and established market presence. These companies focus on product differentiation, technological innovation, and strategic partnerships to gain a competitive edge and expand their customer base across diverse end-user segments and geographic regions.

In addition to established players, the market witnesses the emergence of innovative startups and niche players, capitalizing on advancements in flow battery technology, manufacturing processes, and business models to address evolving customer needs and market dynamics. Startups like Primus Power, EnSync Energy Systems, and Invinity Energy Systems leverage novel approaches, proprietary electrolyte formulations, and modular system designs to offer cost-effective, high-performance flow battery solutions tailored to specific applications, market niches, and customer requirements.

Furthermore, technology conglomerates and multinational corporations enter the flow battery market through strategic investments, acquisitions, and collaborations, aiming to leverage their financial resources, R&D capabilities, and global distribution networks to capture market share and accelerate market growth. Companies like Siemens AG, Sumitomo Electric Industries, Ltd., and Panasonic Corporation explore opportunities in the flow battery market, driven by increasing demand for energy storage solutions, grid modernization initiatives, and the transition to renewable energy sources worldwide.

Global Flow Battery Recent Developments

Scope of global Flow Battery report

Global Flow Battery report segmentation

|

ATTRIBUTE |

DETAILS |

|

By Type |

|

|

By Material |

|

|

By Storage |

|

|

By Application |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Objectives of the Study

The objectives of the study are summarized in 5 stages. They are as mentioned below:

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.