Field Service Management Market Research Report: Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2024-2032: By Component (Solution and Services), By Enterprise Size (Large Enterprise and SMEs), By Deployment Model (On-Premise and Cloud), By End-Use Industry (Manufacturing, Healthcare, BFSI, Transportation & Logistics, Energy & Utilities, Telecom, Construction & Real Estate, and Others), and Region (North America, Europe, Asia-Pacific, and Rest of the World)

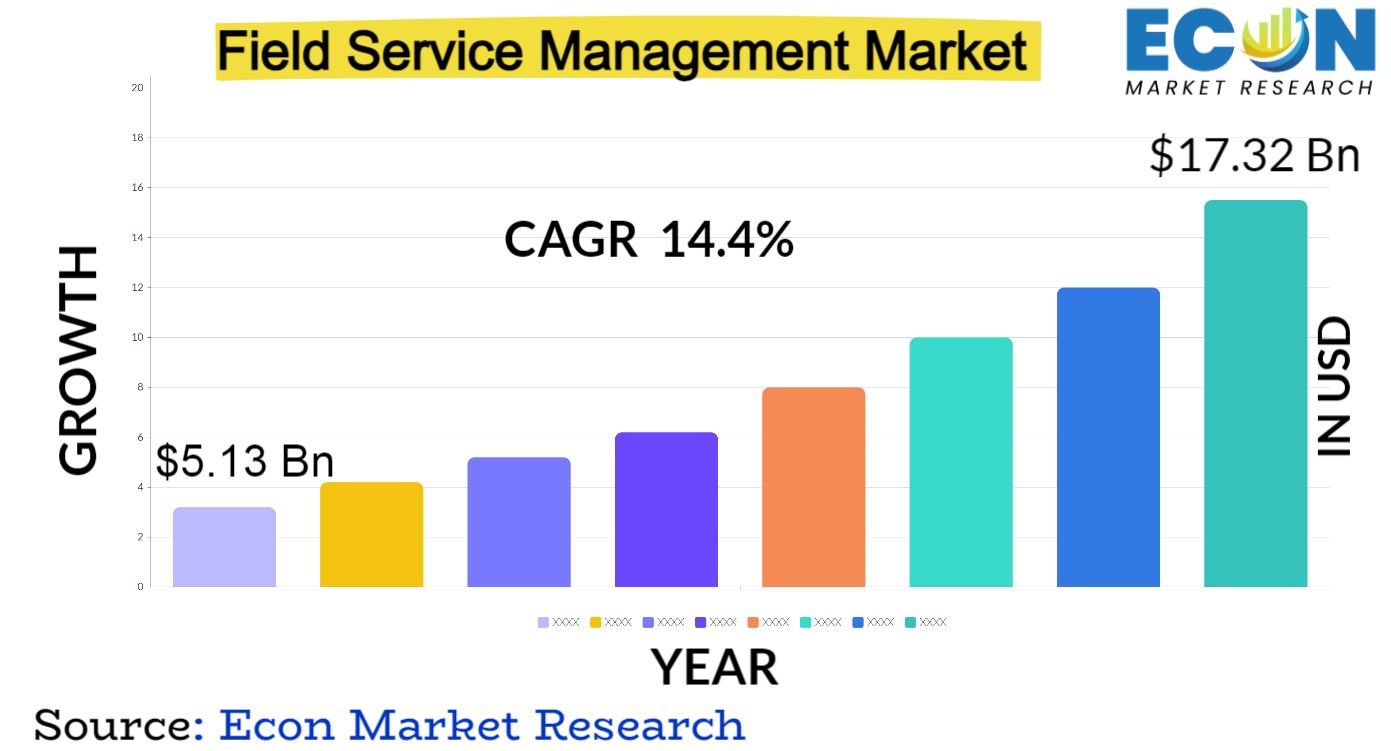

The global field service management market was valued at USD 5.13 billion in 2023 and is estimated to reach approximately USD 17.32 billion by 2032, at a CAGR of 14.4% from 2024 to 2032.

With more businesses realizing the benefits of efficient operations, the field service management market has experienced rapid expansion. This industry focuses on using data analytics, automation, and cutting-edge technologies to maximize field-based operations. Businesses use field service management solutions to guarantee effective resource allocation, increase worker productivity, and improve customer satisfaction. This market is always changing, with new options for scheduling, dispatching, and real-time communication being offered by the proliferation of mobile devices, IoT, and cloud computing. The field service management market continues to be a key driver of operational excellence in a variety of industries, as companies place an increasing emphasis on smooth field operations.

FIELD SERVICE MANAGEMENT MARKET: REPORT SCOPE & SEGMENTATION

|

Report Attribute |

Details |

|

Estimated Market Value (2023) |

5.13 Bn |

|

Projected Market Value (2032) |

17.32 Bn |

|

Base Year |

2023 |

|

Forecast Years |

2024 - 2032 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- By Component, By Enterprise Size, By Deployment Model, By End-Use Industry, & Region |

|

Segments Covered |

By Component, By Enterprise Size, By Deployment Model, By End-Use Industry, & Region |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2024 to 2032 |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, and the Rest of World |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis, and COVID-19 impact analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Field Service Management Market Dynamics

This industry is driven by innovation because to the growing need for workforce optimization, predictive maintenance, and real-time visibility. Customers are happier and operations are run more efficiently when cloud, IoT, and artificial intelligence are all integrated. Competitors and product innovators are encouraged by market participants' constant adaptation to shifting consumer needs.

Further transforming service delivery paradigms include mobile accessibility and distant connectivity. A rising emphasis on sustainability and environmental concerns also has an impact on market dynamics. Technological innovations, client demands, and industry-specific requirements all interact dynamically to shape the field service management market.

Field Service Management Drivers

Businesses can now improve productivity, efficiency, and customer experiences because to the quick development of technologies like cloud computing, artificial intelligence, and the Internet of Things. Processes are revolutionized by automation, data analytics, and real-time connection, allowing firms to act quickly and decisively. Industries that adopt these developments get a competitive advantage, optimize processes, and investigate novel avenues. In today's dynamic and fast-paced corporate climate, technological advancements guarantee continued growth and relevance by not only promoting immediate benefits but also cultivating a culture of continual innovation.

Real-time communication and data interchange are made possible by the broad adoption of digital technology, cloud computing, and secure networking solutions. With the ability to connect, participate, and access centralized systems from any place, this driver empowers remote workforces. Having more connectivity makes it easier to be flexible, responsive, and maintain operations especially when dealing with major international emergencies like pandemics. The capacity to establish and maintain robust distant connectivity becomes critical to preserving productivity, innovation, and overall business continuity as firms place a higher priority on flexibility and resilience.

Restraints:

For small and medium-sized businesses in particular, the significant upfront cost of deploying solutions which includes software, hardware, and training may be a deterrent. The adoption of technologies that increase efficiency may be impeded by this financial load, which can restrict access to sophisticated instruments. Budgetary restrictions may also cause resources to be diverted from other important business sectors. For a balanced investment approach in the dynamic landscape of changing business technology, overcoming the barrier of high initial costs requires strategic financial planning, potential resistance from stakeholders, and careful assessment of long-term advantages.

The complex process of integrating technology with current operations can cause delays and disruptions in the smooth implementation of solutions. The successful implementation of new techniques may be impeded by employee resistance. It will take careful planning, extensive training programs, and successful change management techniques to overcome these obstacles. Ignoring implementation issues can lead to less-than-ideal system performance, which will negatively impact the effectiveness of the implemented solutions inside the organizational structure as well as overall efficiency.

Opportunities:

Predictive analytics is made possible by these technologies, giving companies the ability to foresee trends, improve decision-making, and optimize operations. AI-driven solutions reduce red tape, boost productivity, and reveal important insights in industries including healthcare, finance, and manufacturing. In addition to increasing efficiency, the capacity to automate repetitive processes and adjust to changing data patterns also promotes innovation. Organizations gain a competitive edge when they use AI and machine learning more and more. This opens up new opportunities for individualized services, cost reductions, and game-changing breakthroughs in a variety of industries.

AR transforms the way technicians carry out their work by superimposing digital information onto the real world. AR makes it possible for personnel to troubleshoot, acquire contextual information, and interact easily in a variety of sectors, including maintenance, training, and remote assistance. The utilization of immersive technology leads to increased production, decreased downtime, and improved operational efficiency. As augmented reality develops, companies can take advantage of this chance to improve field operations, offer engaging training, and present creative solutions that transform how teams interact with their workspaces and usher in a new era of productivity.

Segment Overview

Based on components, the global field service management market is divided into solutions and services. The solutions category dominates the market with the largest revenue share in 2023. Solutions for managing field services include software programs or systems that are intended to automate, simplify, and improve many facets of field service operations. These systems include a number of features, including real-time tracking, work order management, inventory control, scheduling, and dispatching. Complementing technological solutions, field service management services handle the operational and human elements of setting up and keeping an efficient field service management system.

Based on the enterprise size, the global field service management market is categorized into large enterprises and SMEs. The large enterprises category leads the global field service management market with the largest revenue share in 2023. Large enterprises are often defined as businesses with a sizable workforce, a wide range of resources, and a significant operational size. These companies operate in a variety of industries and can have a regional or worldwide presence. SMEs are companies that operate on a smaller scale than huge corporations. This category encompasses a wide range of businesses, from small startups to medium-sized enterprises.

Based on deployment mode, the global field service management market is divided into on-premise and cloud. The cloud category dominates the market with the largest revenue share in 2023. One benefit of cloud FSM systems is that they may be accessed from any location with an internet connection. They also offer scalability, which lets companies modify their resource allocation in response to demand. Organizations can have more control over their infrastructure and data with on-premise solutions, which is beneficial for sectors with strict security and compliance regulations.

Based on the end-use industry, the global field service management market is segmented into manufacturing, healthcare, BFSI, transportation & logistics, energy & utilities, telecom, construction & real estate, and others. The telecom segment dominates the field service management market. To increase service reliability, field service management (FSM) is used in the telecom sector for activities including network maintenance, field service scheduling, and quick service outage response.

For effective project delivery and property management, personnel optimization, equipment maintenance, and project management are made easier in the construction and real estate industries by FSM. BFSI employs field support management (FSM) to optimize field operations for tasks including asset management and customer support, manage financial equipment maintenance, and handle service requests.

Field Service Management Market Overview by Region

The global field service management market is categorized into North America, Europe, Asia-Pacific, and the Rest of the World. North America emerged as the leading region, capturing the largest market share in 2023. The region's businesses place a high value on innovation, customer happiness, and operational efficiency, which propels the broad use of FSM solutions.

North American businesses in a variety of industries, including manufacturing, healthcare, finance, and more, use FSM because of the developed market ecosystem to maximize field operations. North America is positioned as a leader in adopting and propelling the growth of the FSM market due to the existence of significant industry players and a high knowledge of cutting-edge technology. Throughout the forecast period, Asia-Pacific is anticipated to post a significant CAGR.

The region's growing economy, fast industrialization, and rising use of cutting-edge technologies in a variety of industries are driving this progress. The need for FSM solutions is growing as companies in the Asia-Pacific region place a higher priority on customer service and operational efficiency. The area is well-positioned for continued market expansion as a result of the changing technological landscape and rising consumer awareness of the advantages of FSM.

Field Service Management Competitive Landscape

In the global field service management market, a few major players exert significant market dominance and have established a strong regional presence. These leading companies remain committed to continuous research and development endeavors and actively engage in strategic growth initiatives, including product development, launches, joint ventures, and partnerships. By pursuing these strategies, these companies aim to strengthen their market position, expand their customer base, and capture a substantial share of the market.

Field Service Management Market Leading Companies:

Field Service Management Recent Developments

Field Service Management Market Report Segmentation

|

ATTRIBUTE |

DETAILS |

|

By Component |

|

|

By Enterprise Size |

|

|

By Deployment Mode |

|

|

By End-Use Industry |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.

+1 812 506 4440

+1 812 506 4440

+91 7875074426

+91 7875074426