Global Electric Ship Market Research Report: By Power Output (<75 kW, 75 kW-745kW, 746 kW-7,560 kW, >7,560 kW), By Power Source (Fully Electric, Hybrid), By Type (Semi-autonomous, Fully-autonomous), By Vessel Type (Commercial vessel, Defense vessel, Special vessel), and Region (North America, Europe, Asia-Pacific, and Rest of the World) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2024-2032.

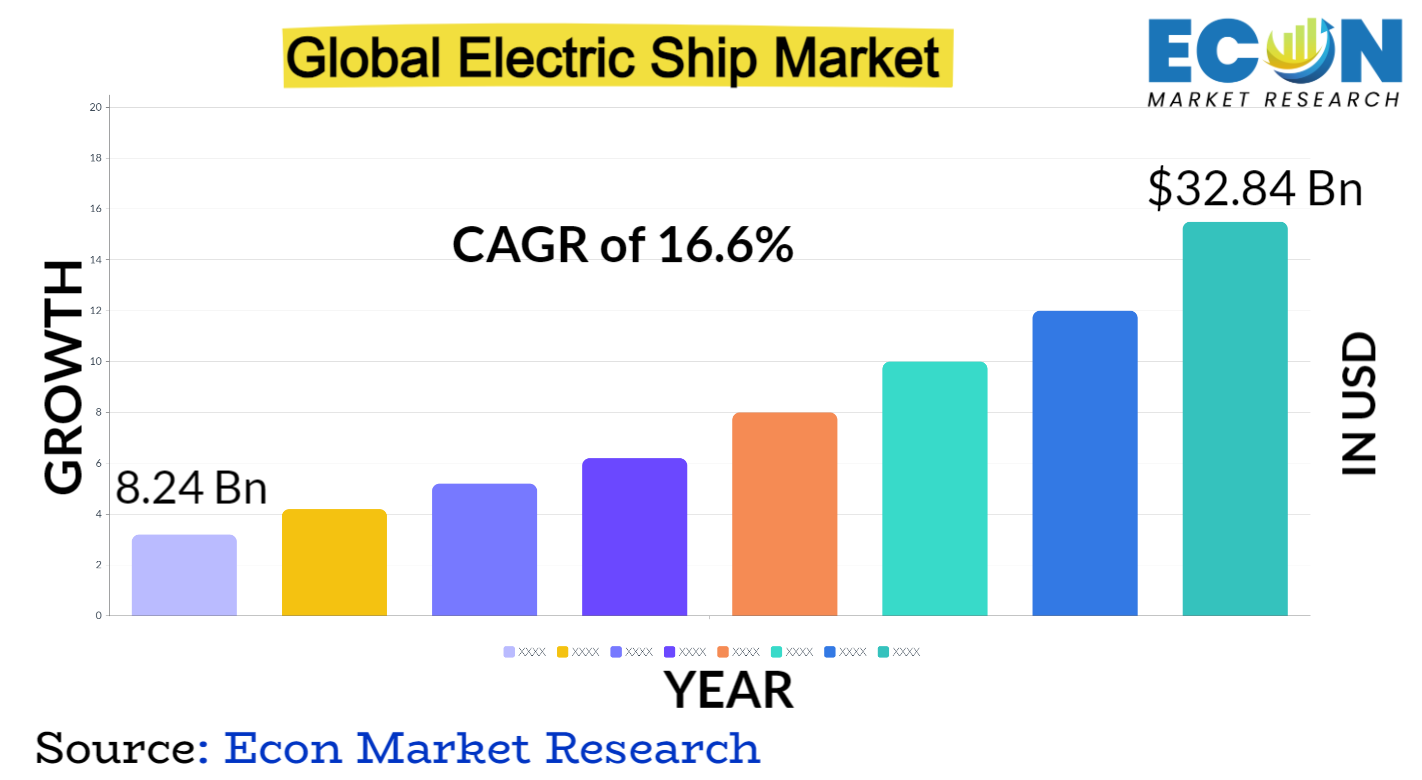

The global electric ship market was valued at USD 8.24 billion in 2023 and is estimated to reach approximately USD 32.84 billion by 2032, at a CAGR of 16.6% from 2024 to 2032.

As a ground-breaking response to environmental issues and technical breakthroughs, the market for electric ships has exploded onto the marine scene. By drastically lowering pollution and dependency on fossil fuels, electric propulsion technologies that run on batteries or fuel cells have completely changed the industry. In the long run, this creative solution is more cost-effective and complies with strict environmental requirements. With multiple competitors making significant investments in the development, testing, and adoption of electric propulsion technologies, the market's growth trajectory indicates a hopeful transition.

Electric power adoption is changing the marine industry, drawing interest from both established maritime giants and cutting-edge startups. These changes include cargo vessels and passenger ferries. Though they still exist, issues like limited energy storage capacity and infrastructural development are being aggressively addressed by partnerships and breakthroughs in battery technology. The market for electric ships is growing rapidly as efficiency and sustainability become more and more important. This marks the beginning of a new age in maritime transportation where clean energy and operational excellence are given top priority.

ELECTRIC SHIP MARKET: REPORT SCOPE & SEGMENTATION

|

Report Attribute |

Details |

|

Estimated Market Value (2023) |

8.24 Bn |

|

Projected Market Value (2032) |

32.84 Bn |

|

Base Year |

2023 |

|

Forecast Years |

2024 - 2032 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- By Power Output, By Power Source, By Type, By Vessel Type, & Region |

|

Segments Covered |

By Power Output, By Power Source, By Type, By Vessel Type, & Region |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2024 to 2032 |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, and the Rest of World |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis, and COVID-19 impact analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Global Electric Ship Market Dynamics

The marine industry has been forced to shift toward greener propulsion technologies by environmental imperatives and strict pollution restrictions. The market's progress has been propelled by the need to minimize the ecological imprint and reduce greenhouse gas emissions. This change has been further accelerated by technological developments in energy storage devices, particularly batteries and fuel cells, which provide practical substitutes for conventional fossil fuel-powered ships. Furthermore, the growing activities and investments from public and commercial sectors as well as research institutions impact the dynamics of the industry.

Funding plans, subsidies, and incentives have sped up research and advanced the development of electric propulsion technology, creating an environment that is conducive to market growth. Shipbuilders, technology companies, and energy corporations have partnered to solve infrastructure obstacles and enhance designs for electric ships. Furthermore, changing customer tastes impact the market dynamics, with sustainability and environmental consciousness playing a bigger role in determining decisions about fleet modernization and the purchase of new vessels. Because of this, the market for electric ships is going through a revolutionary period that is being marked by advancements in technology, encouragement from regulators, and a change in the attitude of the industry toward sustainability.

Global Electric Ship Market Drivers

Governments all throughout the world have implemented strict restrictions requiring fewer emissions from maritime transport in response to growing concerns about climate change and air pollution. The industry is forced to look for greener propulsion options by laws like the International Maritime Organization's (IMO) sulfur cap rules and carbon reduction targets. When compared to traditional fossil fuel-powered vessels, electric ships that run on batteries or fuel cells provide a promising answer because they dramatically reduce greenhouse gas emissions and pollutants.

In addition to supporting regulatory compliance, achieving these emission reduction targets is essential to promoting a more widespread transition in the maritime industry towards sustainability. With ever-tighter restrictions, there is an increasing need for environmentally acceptable propulsion technology, which bodes well for the growth of the electric ship market. As such, companies involved in the marine industry such as shipbuilders, operators, and technology companies are compelled to make investments in and implement electric propulsion systems in order to adhere to these rules and establish themselves as ecologically conscious players.

Innovations in fuel cell and battery technology have completely changed how the marine sector approaches power propulsion systems. These developments have overcome earlier constraints and increased the viability and appeal of electric propulsion by dramatically improving the efficiency, capacity, and reliability of energy storage. Concerns over the viability of electric ships for lengthy voyages and a variety of marine tasks have been allayed by improvements in battery energy density, longevity, and charging capabilities, which have increased the range and operational capabilities of these vessels. Moreover, these energy storage breakthroughs are enhanced by developments in smart grid and charging infrastructure, which guarantee effective power distribution and control on electric boats. By enabling cleaner and more sustainable maritime transportation, the development of energy storage systems not only improves the performance of electric ships but also lessens their environmental impact. Consequently, the increasing use and development of electric propulsion systems in the maritime industry is being fueled by these technological advancements in energy storage, which is paving the way for more environmentally friendly and effective transportation methods.

Restraints:

Power distribution networks, appropriate ports, and charging stations are only a few examples of the inadequate and underdeveloped infrastructure needed to accommodate electric warships. Current ports are primarily designed to serve ships that run on conventional fuel and do not have the infrastructure required to meet the specific needs of electric ships with regard to energy supply and charging. Significant obstacles also exist in the form of the expense and difficulty of building or modifying electric vessel charging facilities.

The problem is made worse by the lack of a defined infrastructure or billing system, which impedes scale and interoperability. Infrastructure construction is further complicated by ongoing concerns about the grid's ability to handle the increasing power demands from numerous electric ships charging at the same time. These restrictions reduce the operational adaptability and range of electric ships, hindering their mainstream adoption and turning off prospective operators or investors who are apprehensive about the infrastructure's readiness. To fully realize the potential of electric ships and enable their smooth integration into the marine transportation ecosystem, it is imperative that these infrastructure constraints are addressed.

Making the switch from traditional fuel-powered ships to electric ships requires large initial costs. When compared to more conventional propulsion methods, the cost of purchasing and modifying vessels equipped with electric propulsion systems which may need sophisticated batteries or fuel cells—is significantly greater. The initial financial burden is further increased by the cost of constructing charging infrastructure and modernizing ports to handle electric vessels.

The high upfront costs of electric propulsion systems can put off potential investors or fleet operators, especially in an industry where profit margins are tightly monitored, even though they offer long-term operational cost benefits through lower fuel prices and maintenance. Further discouraging the commitment to these greater upfront costs are doubts about the long-term return on investment and the perceived hazards of new technologies. The adoption rate of electric ships is hindered by these financial problems, even though they have advantages for the environment and operations. Accelerating the wider acceptance and integration of electric ships into the marine industry requires finding ways to reduce these upfront costs through incentives, subsidies, or creative financing arrangements.

Opportunities:

The market for electric ships has a lot of potential due to the growing need for environmentally friendly transportation options. Using environmentally friendly transportation options is becoming more and more important as concerns about the environment throughout the world grow. The growing need for environmentally friendly transportation is well matched by electric ships, which are propelled by clean energy sources like fuel cells or batteries. A paradigm shift toward greener techniques has resulted from growing consumer, industry, and government understanding about the environmental impact of old transport systems. This change presents an enormous market opportunity for electric ships, establishing them as a competitive and alluring choice for people looking for environmentally friendly maritime solutions.

It is anticipated that demand for electric ships would increase dramatically as consumers, companies, and legislators increasingly consider sustainability when making decisions. Seizing this chance demonstrates a dedication to adopting eco-friendly practices and lowering carbon footprints in addition to meeting market demand. As a result, the market for electric ships is leading the way in addressing the growing need for environmentally conscious and progressive transportation options, providing a means of reshaping the marine sector.

Governments everywhere are realizing how critical it is to shift to greener modes of transportation in order to slow down global warming and cut down on pollution. Governments are making this promise by implementing laws, grants, subsidies, and tax breaks designed especially to promote the adoption of environmentally friendly technologies in the maritime industry. These programs seek to lessen the financial burden related to the adoption of electric ships while simultaneously hastening the transition towards them.

The initial investment costs for stakeholders are greatly decreased by financial incentives such as grants for R&D, subsidies for buying electric vessels, or tax advantages for businesses engaging in green shipping technologies. Further encouraging the deployment of electric ships are regulatory regimes that support zero-emission shipping and grant them preferred access to ports or lower costs. Accepting these government programs not only promotes a more sustainable maritime sector but also puts interested parties in a position to gain from the tax breaks and edge over competitors provided by government backing.

Segment Overview

By Power Output

Based on power output, the global electric ship market is divided into <75 kW, 75 kW-745kW, 746 kW-7,560 kW, >7,560 kW. The 75 kW-745kW category dominates the market with the largest revenue share in 2023. A wide range of passenger and commercial ships, including ferries, smaller cargo ships, and certain mid-sized boats, are frequently included in this power range. They need a power capacity that is somewhat higher to navigate and meet their operational needs. In general, smaller boats, personal watercraft, and certain smaller commercial vessels fall under the <75 kW group. These vessels can function well with electric propulsion systems that are less than 75 kW in power consumption. Larger ships such as medium-sized cargo ships, passenger ferries, and certain medium-range cruise ships fall into the 746 kW–7,560 kW group. Because of their much higher power requirements, these vessels need more reliable electric propulsion systems to function well. Large cruise ships, big container ships, and other specialty boats like LNG carriers are all included in the >7,560 kW category, which is the highest power category for electric ships. Due to their high power needs, these warships require incredibly powerful electric propulsion systems in order to function.

By Power Source

Based on the power source, the global electric ship market is categorized into fully electric, and hybrid. The hybrid category leads the global electric ship market with the largest revenue share in 2023. Hybrid electric ships combine electric propulsion with conventional propulsion systems, including gas turbines or diesel engines, to combine several power sources. These vessels use a combination of electric systems (batteries or fuel cells) and conventional fuels for power generation. Depending on demand or operational requirements, hybrid ships can operate in a variety of modes, utilizing traditional propulsion in addition to electric propulsion or a combination of the two.

By maximizing power sources and cutting fuel and emissions, they provide flexibility and efficiency improvements. This is especially useful in situations where the electric mode can be used for certain operating phases or lower speeds, which improves overall sustainability. All-electric vessels use fuel cells or batteries as their main power source and only use electric propulsion systems. When propelled, these boats don't release any direct emissions of pollutants or carbon gases into the atmosphere. They use onboard energy storage to power electric motors, which propel the craft and supply power to all essential systems.

By Type

Based on type, the global electric ship market is segmented into semi-autonomous, and fully-autonomous. The semi-autonomous segment dominates the electric ship market. Electric ships that are semi-autonomous use automation to help and optimize several parts of vessel operations, but crucial decision-making and control still need human monitoring and intervention. Automation technology is utilized by these vessels for specialized purposes such as route optimization, navigation, collision avoidance, and monitoring systems. Even if some jobs can be automated, human operators are still in charge of monitoring and taking action when needed, particularly in challenging or unforeseen circumstances.

During routine operations, fully autonomous electric ships run without direct human involvement or control. These boats can navigate, plan routes, prevent collisions, dock, and conduct all other operations autonomously since they are outfitted with cutting-edge artificial intelligence (AI), sensors, and navigation systems. To make decisions and adapt to shifting sea conditions, they rely on real-time data and algorithms.

By Vessel Type

Based on vessel type, the global electric ship market is divided into commercial vessels, defense vessels, and special vessel. The commercial vessel category dominates the market with the largest revenue share in 2023. The business sector uses commercial electric vessels to meet a variety of maritime transportation demands. These consist of bulk carriers, passenger ships, cargo ships, container ships, tankers, ferries, and other types of vessels used for trade, transit, and passenger services. Commercial vessels with electric propulsion systems can benefit from decreased emissions, longer-term cheaper running costs, adherence to environmental standards, and possibly increased market competitiveness because of their environmentally friendly design. Military and defense vessels are also utilizing electric propulsion technologies. These vessels include coast guard boats, patrol boats, naval ships, and other military craft using electric power. Defense warships using electric propulsion can benefit from lower maintenance costs, enhanced stealth capabilities, less acoustic signatures, and greater operational efficiency.

Global Electric Ship Market Overview by Region

The global electric ship market is categorized into North America, Europe, Asia-Pacific, and the Rest of the World. Europe emerged as the leading region, capturing the market share in 2023. The adoption of electric propulsion systems has been fueled by the region's strong commitment to environmental sustainability and strict rules aimed at decreasing emissions from maritime vessels. To encourage the shift to greener and more effective transportation methods, European governments have implemented financial programs, incentives, and supporting regulations. Furthermore, innovation in electric ship technology has been stimulated by the continent's thriving marine sector, sophisticated technological capabilities, and partnerships between technology companies, research institutes, and shipbuilders. The well-established infrastructure in Europe, which includes charging stations and ports suitable for electric ships, makes it easier to incorporate electric ships into the network of maritime transportation.

In the electric ship market, the Asia-Pacific area is projected to grow at the fastest compound annual growth rate (CAGR) over the projected period. The need for creative and environmentally friendly shipping solutions is fueled by the world's fastest industrialization, expanding trade, and growing need for maritime transportation in nations like China, Japan, South Korea, and Singapore. Additionally, Asia-Pacific is positioned as a major hub for the adoption and advancement of electric ship technologies due to the region's large investments in technology, research, and infrastructure development, as well as government initiatives promoting clean energy and emission reduction. These factors together account for the market segment's predicted high growth rate.

Global Electric Ship Market Competitive Landscape

In the global electric ship market, a few major players exert significant market dominance and have established a strong regional presence. These leading companies remain committed to continuous research and development endeavors and actively engage in strategic growth initiatives, including product development, launches, joint ventures, and partnerships. By pursuing these strategies, these companies aim to strengthen their market position, expand their customer base, and capture a substantial share of the market.

Some of the prominent players in the global electric ship market include,

Global Electric Ship Market Recent Developments

In February 2023, COSCO SHIPPING Development and COSCO SHIPPING supported the official founding of the Electric Ship Innovation Alliance (CESIA). With this action, China solidifies its leadership position in the global electrification of the shipping sector.

In January 2023, The inaugural large next-generation electric propulsion ship in South Korea was put into service by Hyundai Heavy Industries. The ship has two power sources that it can use: LNG fuel, batteries, or a combination of the two. It will be used for both tourist excursions around the Korean coast and demonstrations.

In May 2022, Danfoss Power Solutions' Editron business established a partnership with Baltic Workboats to supply an electric propulsion system for the bicycle ferry and new hybrid passenger ship built by the Estonian shipyard. Up to 50 people and 25 bicycles can be transported simultaneously on the hybrid boat.

Scope of the Global Electric Ship Market Report

Electric Ship Market Report Segmentation

|

ATTRIBUTE |

DETAILS |

|

By Power Output |

|

|

By Power Source |

|

|

By Type |

|

|

By Vessel Type |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Objectives of the Study

The objectives of the study are summarized in 5 stages. They are as mentioned below:

Intended Audience

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.