Global Defence Electronic Market Research Report: By Vertical (Navigation, Communication, Display, C4ISR, Electronic Warfare, Radar, Optronics), By Component (Hardware, Software), By System (Airborne, Marine, Land, Space), and Region (North America, Europe, Asia-Pacific, and Rest of the World) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2023-2031.

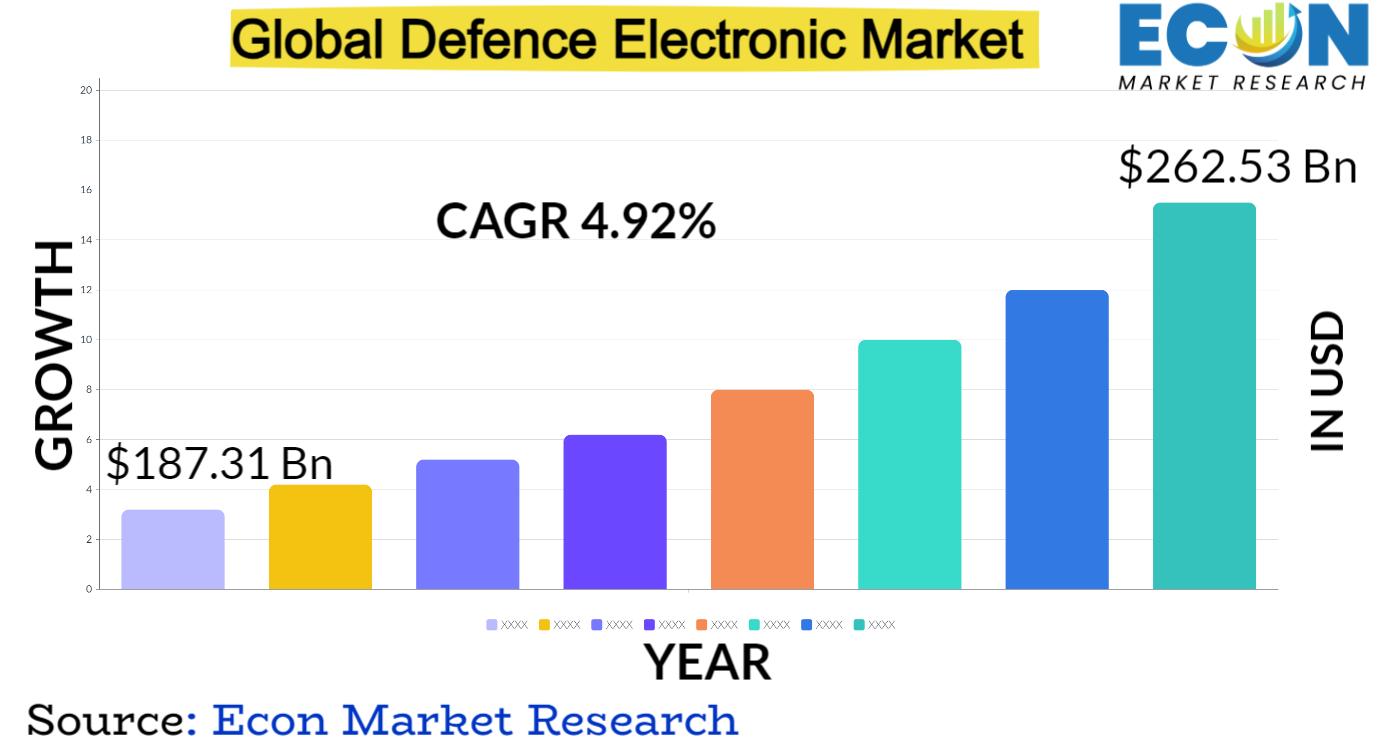

The global defence electronic market was valued at USD 187.31 billion in 2022 and is estimated to reach approximately USD 262.53 billion by 2031, at a CAGR of 4.92% from 2023 to 2031.

Defense electronics refers to electronic components and systems that are specifically designed for technological superiority in defense setup. It provides robust, high performance electronic detection, electronic protection, and electronic attack capabilities to support the success of missions and minimize casualties. Furthermore, the electronic solutions are developed by multi-disciplinary teams of engineers, in collaboration with commercial and academic counterparts.

DEFENCE ELECTRONIC MARKET: REPORT SCOPE & SEGMENTATION

|

Report Attribute |

Details |

|

Estimated Market Value (2022) |

187.31 Billion |

|

Projected Market Value (2031) |

262.53 Billion |

|

Base Year |

2022 |

|

Forecast Years |

2023 - 2031 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- By Vertical, By Component, By System& Region |

|

Segments Covered |

By Vertical, By Component, By System & Region |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2023 to 2031 |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, and the Rest of World |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis, and COVID-19 impact analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Global Defence Electronic Drivers:

Increasing adoption of integrated defense electronic technologies

Increasing adoption of integrated defense electronic technologies for the electrical circuit is used by the military and police for defence purposes. In addition, the use of integrated defense electronics products provides multiple advantages, such as real-time decision-making, remote operations, and reprogramming of systems for defense against new and emerging threats. Armies, navies and air forces have conducted radar electronic warfare to deny, protect against and/or exploit the adversary use of radar systems. Thus, driving demand of the global defense electronic market.

Opportunities:

Growing Artificial Intelligence (AI) Investment Activities

Militaries around the world are increasingly viewing AI as a critical component of their long-term tactics and planning. The largest military firms are one of the most important channels for integrating emerging technologies such as AI-enabled technology into defense systems and platforms. With tech behemoths like Amazon and Google at the forefront of AI innovation, big military firms are under pressure to increase their innovation-related operations in order to keep up with the larger commercial sector. In the defense electronics sector, AI investment activities primarily focus on autonomous systems, cybersecurity, data analysis and intelligence, training and simulation, predictive maintenance, and communication and networking. Therefore, will create growth opportunities for the target market.

Restraints:

Effects of Geopolitical Uncertainties on the Defense Electronics Industry

Uncertainties in geopolitics have a direct impact on defense spending, international trade, and technology transfer. They put a pressure on international defense partnership programs. Diverging national interests and concerns about technology sharing provide a variety of problems for international defense cooperation. Trade wars and political sanctions have the potential to disrupt the global supply chain for defense electronics components and supplies. The reliance on suppliers involved in geopolitical crises results in possible supply constraints and increased shortages. This is expected hamper the growth of the target market.

Segment Overview

By Vertical

Based on vertical, the global defence electronic market is divided into navigation, communication, display, c4isr, electronic warfare, radar, and optronics. The communication segment dominated the global defence electronic market in 2022. This is attributed to communication systems include radio communication, satellite communication, and secure data networks, are critical for permitting real-time information sharing between military people and units. It is key for rising awareness about the situation and self-defense. During the forecast period, the radar segment is expected to increase rapidly.

By Component

Based on component, the global defence electronic market is divided into hardware, software. The hardware segment dominated the defence electronic market with the largest revenue share in 2022. This due to the hardware includes several equipment and systems, which are significant to the development & operation of electric defense. The hardware component facilitates the development of advanced defense systems and enable capabilities including commutations, surveillance, detection and control. Therefore, increasing demand of this segment in the global market.

By System

Based on system, the global defence electronic market is fragmented into airborne, marine, land, space. The airborne segment dominated the defence electronic market in 2022, owing to the avionics systems are important components of the segment, which includes flight control systems for aircraft control, navigation, communications and tracking. In addition, the MIL-STD-461 specification is widely used as a general basis for testing defence electronics. Voltage spike tests with 150 ns duration as defined in MIL-STD-461C are still relevant for testing airborne power systems. This is expected to fuel growth of this segment target market.

Global Defence Electronic Overview by Region

North America dominated the defence electronic market in 2022. This is attributed to increasing demand of the US defense electronics in this region. In response to the government and its partners operating in an increasingly complicated security environment, defense technology is rapidly evolving. The defense information systems agency and the department of defense information network are working to repurpose cutting-edge technologies including artificial intelligence, development, security, and operations, as well as zero-trust assets, to defend the Defense Department's global network. These all factor affecting the growth of the defence electronic market in this region.

Global Defence Electronic Competitive Landscape

In the global defence electronic market, a few major players exert significant market dominance and have established a strong regional presence. These leading companies remain committed to continuous research and development endeavors and actively engage in strategic growth initiatives, including product development, launches, joint ventures, and partnerships. By pursuing these strategies, these companies aim to strengthen their market position, expand their customer base, and capture a substantial share of the market.

Some of the prominent players in the global defence electronic market include Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation, Thales Group, BAE Systems plc, General Dynamics Corporation, Saab AB, L3Harris Technologies, Inc., Leonardo S.p.A., Rheinmetall AG, Elbit Systems Ltd., Hensoldt AG, Hanwha Corporation, Mitsubishi Electric Corporation, IndraSistemas S.A., Israel Aerospace Industries Ltd, Rafael Advanced Defense Systems Ltd., CACI International Inc, QinetiQ Group plc. and others.

Global Defence Electronic Recent Developments

Scope of the Global Defence Electronic Market Report

Defence Electronic Market Report Segmentation

|

ATTRIBUTE |

DETAILS |

|

By Vertical |

|

|

By Component |

|

|

By System |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Objectives of the Study

The objectives of the study are summarized in 5 stages. They are as mentioned below:

Intended Audience

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.