Global Data Center RFID Market Research Report: By Component (Hardware, Software, Services), By Hardware (Tags, Reader, Printer, Antenna, Others), By Tags (Active, Passive), By Tag Frequency (LHF, HF, UHF), By Application (Asset Tracking and Management, IT Asset Management, Lifecycle Management, Others), and Region (North America, Europe, Asia-Pacific, and Rest of the World) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2024-2032.

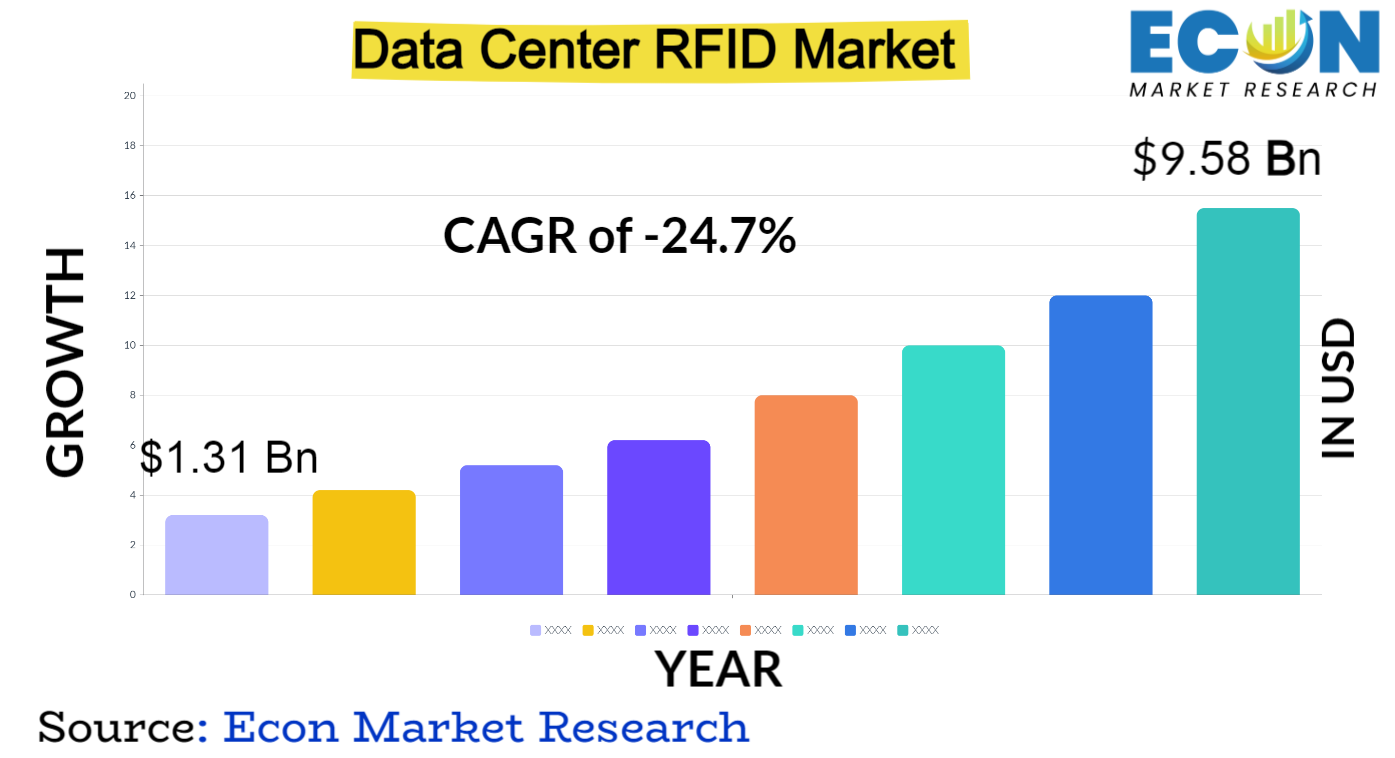

The global data center RFID market was valued at USD 1.31 billion in 2023 and is estimated to reach approximately USD 9.58 billion by 2032, at a CAGR of 24.7% from 2024 to 2032.

The market for radio frequency identification (RFID) in data centers has grown to become a key technology in data management and security. RFID systems are the most accurate and efficient solutions available for asset monitoring, inventory management, and general data center optimization. They work by using radio waves to detect and track tags that are remotely affixed to items. This technology was introduced, and since then, its popularity has grown quickly since it can improve operational visibility, optimize workflows, and strengthen security standards in data centers.

By avoiding human error and drastically cutting down on the amount of time needed for inventory audits and asset tracking, the seamless integration of RFID systems has enabled data center operators to monitor and manage assets in real time. Moreover, RFID systems' versatility and scalability have accelerated their acceptance in a variety of industries, promising increased data center management efficiency and cost-effectiveness. The data center RFID market is growing as a result of ongoing developments and innovations, meeting the growing needs of the digital age for accuracy, security, and operational excellence.

DATA CENTER RFID MARKET: REPORT SCOPE & SEGMENTATION

|

Report Attribute |

Details |

|

Estimated Market Value (2023) |

1.31 Bn |

|

Projected Market Value (2032) |

9.58 Bn |

|

Base Year |

2023 |

|

Forecast Years |

2024 - 2032 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- By Component, By Hardware, By Tags, By Tag Frequency, By Application & Region |

|

Segments Covered |

By Component, By Hardware, By Tags, By Tag Frequency, By Application, & Region |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2024 to 2032 |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, and the Rest of World |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis, and COVID-19 impact analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Global Data Center RFID Market Dynamics

Technological developments such as the shrinking of RFID tags, increased read ranges, and better data accuracy have encouraged their broad use in data center infrastructures. One of the main drivers has been the growing requirement for asset management that is efficient, streamlined processes, and strict security measures. Furthermore, the need for reliable RFID solutions has increased due to the growing intricacy of data center ecosystems, which is being driven by cloud, edge, and Internet of Things deployments.

The trend toward automation and digital transformation also has an impact on this sector, and RFID is essential to the development of intelligent and self-sufficient inventory management systems. RFID technology adoption has also been spurred by the need to reduce operational risks and comply with regulatory standards. Furthermore, alliances between suppliers of RFID technology, managers of data centers, and providers of IT solutions have expanded the market and encouraged innovation and specially designed solutions for certain business requirements. The RFID market is expected to increase steadily as the data center landscape changes because of continued technological advancements, growing data complexities, and the constant need for improved security and operational efficiency.

Global Data Center RFID Market Drivers

Improved operational effectiveness is a key factor driving the use of RFID technology in data centers. Data center operators can transform their operations with automated workflows, faster inventory management, and real-time asset tracking by utilizing RFID technology. Without requiring direct line-of-sight contact, RFID provides quick and accurate asset identification, location, and monitoring. This greatly reduces the need for human intervention and the possibility of data entry errors. By using this technology, resource usage is optimized, inventory audits are expedited, and the time and effort required for manual tracking operations is reduced. Additionally, RFID systems speed up data collection and provide instantaneous insight into the movements and statuses of assets, enabling proactive decision-making and more efficient operational workflows. Because labor-intensive processes become automated and operational downtime is reduced, the efficiency gains result in cost savings. In the end, using RFID to improve operational efficiency not only speeds up and improves the accuracy of data center operations, but it also creates the foundation for more competitive, responsive, and agile corporate operations in a fast-changing technology environment.

RFID solutions offer a strong foundation for enforcing stringent asset monitoring procedures and strengthening security measures. In the context of a data center, these technologies provide an advanced method of authenticating and tracking assets across time. Data center managers can effectively track assets in real time and reduce the risk of theft, unauthorized access, and lost things by utilizing RFID tags and readers. Complete visibility into asset movements, locations, and usage history is made possible by the system, which gives operators the ability to impose strict security procedures and quickly spot any irregularities. Furthermore, RFID's ability to manage inventory automatically lowers the possibility of error in asset tracking, guaranteeing accurate and current inventory records. By displaying a dedication to careful asset management and security procedures in handling sensitive data and infrastructure, this degree of control not only strengthens the security posture of data centers but also fosters a climate of confidence among stakeholders, regulatory agencies, and clients.

Restraints:

The financial ramifications are multifaceted and comprise the acquisition of RFID tags, and readers, changes to the infrastructure, and integration costs. A significant obstacle for numerous data center operators, particularly those operating in smaller or medium-sized facilities, is the initial financial commitment. The significant financial investment necessary for the implementation of RFID systems can put a strain on finances and reduce interest in pursuing new technologies, especially when working solutions appear to be sufficient.

The overall cost is increased by the potential downtime during the integration and training stages as well as the cost of converting current systems to support RFID technology. Some entities may choose to continue with conventional methods or make incremental modifications instead of embracing RFID due to the perceived risk against the immediate return on investment. The initial financial burden of RFID technology remains a primary constraint, despite its long-term benefits in improving operational efficiency and security. This means that careful cost-benefit analysis and consideration of the technology's strategic value in promoting data center optimization and competitive advantage are necessary.

The read range can limit the usefulness of RFID systems, especially in bigger or more complex data center configurations. It is determined by several factors, including tag type, frequency, and interference. RFID signals may be interfered with in situations with a high concentration of liquid or dense metal structures, which could result in a reduction in read ranges and possibly inaccurate data. Furthermore, RFID tags have designated operating ranges. If tags are positioned outside of these ranges, they might not be able to communicate with readers efficiently, which would affect the overall dependability of asset tracking and management. Furthermore, even though improvements have been made to read ranges, it is still difficult to reliably achieve longer ranges in a variety of data center situations. Widespread adoption is further hampered by the ongoing expense and complexity of infrastructure changes required to maximize read ranges and reduce environmental interference. The aforementioned constraints highlight the significance of thorough planning and system design to account for environmental considerations and maximize RFID deployments for dependable operation in data center settings.

Opportunities:

A distributed network of smaller data centers, or nodes, at the edge of networks is created by edge computing, which is characterized by decentralized processing closer to data sources. The increasing number of edge sites need accurate and effective asset tracking and management systems, which is where RFID shines. In these dispersed setups, RFID systems which are skilled at tracking and monitoring assets in real time become indispensable.

The proliferation of edge computing increases the demand for simplified operations across multiple distant sites, necessitating reliable systems that can precisely and autonomously manage assets. RFID is well suited to the requirements of edge computing infrastructure because it can easily track and monitor assets in real-time, regardless of their geographic dispersion. Because RFID technology and edge environment requirements work well together, RFID becomes an essential enabler that lets data center operators keep precise control and visibility over assets dispersed across various edge locations. This allows them to take advantage of this growing opportunity within the changing data center infrastructure landscape.

The data center environment presents an extensive potential for RFID technology due to advancements in healthcare and life sciences. RFID is ideally suited to meet the complex requirements of these sectors, which range from strict regulatory standards to the need for careful inventory management and patient safety. With its ability to precisely track assets, identify patients, and manage inventories in data centers that serve these industries, RFID technology has enormous potential in the healthcare and life sciences sectors.

RFID-enabled healthcare solutions can guarantee precise tracking of pharmaceuticals, medical equipment, and patient data, lowering mistakes, maximizing stock levels, and improving patient care. Furthermore, RFID is essential for ensuring adherence to legal requirements like track-and-trace laws governing drugs and medical equipment. RFID is a cornerstone technology that is driving efficiency and innovation in these vital sectors. Its integration into data center infrastructures serving the healthcare and life sciences not only streamlines operations but also ensures greater patient safety, improved inventory accuracy, and enhanced regulatory adherence.

Segment Overview

Based on components, the global data center RFID market is divided into hardware, software, and services. The hardware category dominates the market with the largest revenue share in 2023. This section covers the hardware requirements for implementing RFID in data centers. RFID tags, readers, antennae, and other infrastructure components necessary for data collection and transmission are included. Assets or objects to be tracked have RFID tags attached to them, and the system and tags may communicate with each other thanks to readers and antennae.

The software section consists of the platforms and software programs needed to handle and analyze RFID data. It comprises software programs for asset tracking, inventory control, analytics, real-time monitoring, and interface with current data center management systems. RFID software is essential for processing the data that RFID hardware collects, as it offers insights, generates reports, and facilitates effective decision-making by utilizing the data obtained from RFID tags and readers.

The services section consists of a range of products and services that vendors or other third parties offer to assist with the setup, upkeep, and improvement of RFID systems in data centers. This covers system integration, installation, training, advising, and continuous support services. Service providers support the development of customized RFID solutions, system deployment, employee training, and the seamless integration of RFID technology into data center settings.

Based on the hardware, the global data center RFID market is categorized into tags, readers, printers, antennas, and others. The readers category leads the global data center RFID market with the largest revenue share in 2023. RFID readers, sometimes referred to as interrogators, are gadgets that speak with RFID tags to read the information they contain. To communicate with active tags and get information such as asset location, status, or other pertinent data, they generate radio waves that power passive tags. An essential part of the RFID system is readers, which allow data to be gathered from tags and sent to the RFID software for processing and analysis. RFID tags are tiny electronic devices with an embedded unique identifier that transmits data wirelessly to RFID readers. These tags can be affixed to goods, machinery, or assets inside the data center.

They are available in three different configurations: passive, active, and semi-passive. RFID printers are specialized equipment meant to read data from RFID tags. They make it easier to print and encode data on RFID labels or tags so that it can be used in a data center setting. These printers make sure that tags are correctly configured and have all the information that is required before they are attached to items or assets. RFID readers and antennas collaborate to create communication with RFID tags. They allow the readers to read the data that is stored on the tags by sending out radio waves and receiving signals from the tags. Different types and configurations of antennas are available, each tailored to suit specific read ranges, orientations, and data center climatic conditions.

Based on tags, the global data center RFID market is segmented into active and passive. The passive segment dominates the data center RFID market. RFID systems that are passive in nature consist of tags that lack an internal power supply. When RFID readers are within range, the electromagnetic energy they send powers these tags. Compared to active tags, passive RFID tags are less costly, lighter, and smaller. They are appropriate for a number of data center applications, particularly asset tracking and inventory management. They are perfect for shorter-distance applications, too, as their read ranges are usually less than those of active tags. Active RFID systems make use of tags that include an internal power supply, typically a battery.

These tags may communicate data over greater distances and function independently of the vicinity of a reader because they generate a signal at regular intervals. Extended scan ranges and improved performance in interference- or obstacle-filled settings are provided by active RFID tags. They are frequently used in situations when continuous or real-time tracking is necessary within data centers, like monitoring equipment mobility, tracking high-value assets, or guaranteeing security in larger-scale settings.

Based on tag frequency, the global data center RFID market is divided into LHF, HF, and UHF. The UHF category dominates the market with the largest revenue share in 2023. The frequency band in which UHF RFID operates is roughly 860 to 960 MHz. Compared to LF and HF RFID, UHF systems provide faster data transfer rates and larger scan ranges. They work effectively for applications like supply chain visibility, inventory management, and logistics tracking that call for long-range asset identification and tracking in data centers.

The frequency band in which LF RFID functions is roughly 125 kHz. Lower frequency (LF) tags and readers are well-known for their superior penetration of materials such as metal and water compared to higher frequency devices. They can be used in data centers where objects are near liquids or metals since they are less susceptible to interference and operate dependably in challenging conditions. The frequency band in which HF RFID operates is around 13.56 MHz. HF RFID systems offer an excellent mix between read range and data transfer speed, and they give higher data transfer rates than LF systems. Applications like contactless payment, identity cards, library systems, and healthcare applications like patient tracking or medication authentication are just a few of the uses for them in data centers.

Based on the application, the global data center RFID market is categorized into asset tracking and management, IT asset management, lifecycle management, and others. The asset tracking and management category leads the global data center RFID market with the largest revenue share in 2023. The use of RFID technology to track and manage different physical assets in data centers is the main topic of this category. Equipment, tools, inventory, and other tangible assets must all be identified, tracked in real time, and monitored. Data center operators can find assets, control inventory levels, and maximize asset usage with the use of RFID tags affixed to assets that provide accurate and efficient tracking.

RFID-based asset tracking and management improves overall efficiency in data center environments by streamlining operations and minimizing inventory inconsistencies. In data centers, RFID technology is essential to IT asset management. It entails managing and tracking computer hardware, servers, networking devices, and other IT assets with RFID tags. Data center managers can use RFID to manage asset lifecycles, track equipment location, check asset status, conduct audits, and make sure asset management regulations are being followed. RFID makes lifecycle management easier by giving data centers insight and control over their assets at every stage of their lifecycle. This covers asset monitoring from the time of purchase through deployment, use, upkeep, and decommissioning. RFID technology helps with asset condition monitoring, determining maintenance requirements, and guaranteeing appropriate recycling or disposal at the end of an asset's lifecycle.

Global Data Center RFID Market Overview by Region

The global data center RFID market is categorized into North America, Europe, Asia-Pacific, and the Rest of the World. North America emerged as the leading region, capturing the largest market share in 2023. Strong technology infrastructure in the area encourages early adoption and data center integration of RFID technologies. North American businesses have adopted RFID for improved operational efficiency, accurate asset monitoring, and strict security measures due to the region's high concentration of well-established data center facilities and proactive attitude toward technology improvements. Additionally, a number of the region's varied business verticals, such as retail, logistics, and healthcare, have made significant use of RFID technology, propelling market expansion. North America's leadership in the data center RFID market has been further cemented by the existence of significant RFID solution providers, research and development expenditures, and innovation that have stimulated the customization of RFID applications.

Throughout the forecast period, Asia-Pacific is anticipated to post a significant CAGR. There is a strong need for advanced data management solutions in the region because of the swift digital transformation taking place in a number of industries. The developing economies of Asia-Pacific, especially those of China, India, and the countries of Southeast Asia, are experiencing a great deal of industrialization and infrastructure development, which is causing a rise in the construction of data centers. RFID integration benefits greatly from the boom in data center deployments brought about by the expansion of e-commerce, the acceptance of cloud computing, and the proliferation of IoT devices. In addition, the region's technology adoption strategy, when combined with encouraging government programs and funding, accelerates the use of RFID technologies in data centers. The need for RFID technology is higher in a variety of industries, including manufacturing, retail, and logistics, due to the necessity of effective inventory management, supply chain optimization, and strict security measures.

Global Data Center RFID Competitive Landscape

In the global data center RFID market, a few major players exert significant market dominance and have established a strong regional presence. These leading companies remain committed to continuous research and development endeavors and actively engage in strategic growth initiatives, including product development, launches, joint ventures, and partnerships. By pursuing these strategies, these companies aim to strengthen their market position, expand their customer base, and capture a substantial share of the market.

Some of the prominent players in the global data center RFID market include,

Global Data Center RFID Recent Developments

Scope of the Global Data Center RFID Market Report

Data Center RFID Market Report Segmentation

|

ATTRIBUTE |

DETAILS |

|

By Component |

|

|

By Hardware |

|

|

By Tags |

|

|

By Tag Frequency |

|

|

By Application |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Objectives of the Study

The objectives of the study are summarized in 5 stages. They are as mentioned below:

Intended Audience

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.