Data Center Infrastructure Market by Component Type (Hardware, Software, and Services), by Deployment Type (On-premise, and Cloud), by Organization size (Small & medium enterprise, and large enterprise) and by End Users (BFSI, Retail, IT Telecom, Healthcare, Energy, Government, Manufacturing, and Others): Global Opportunity Analysis and Industry Forecast, 2023-2032.

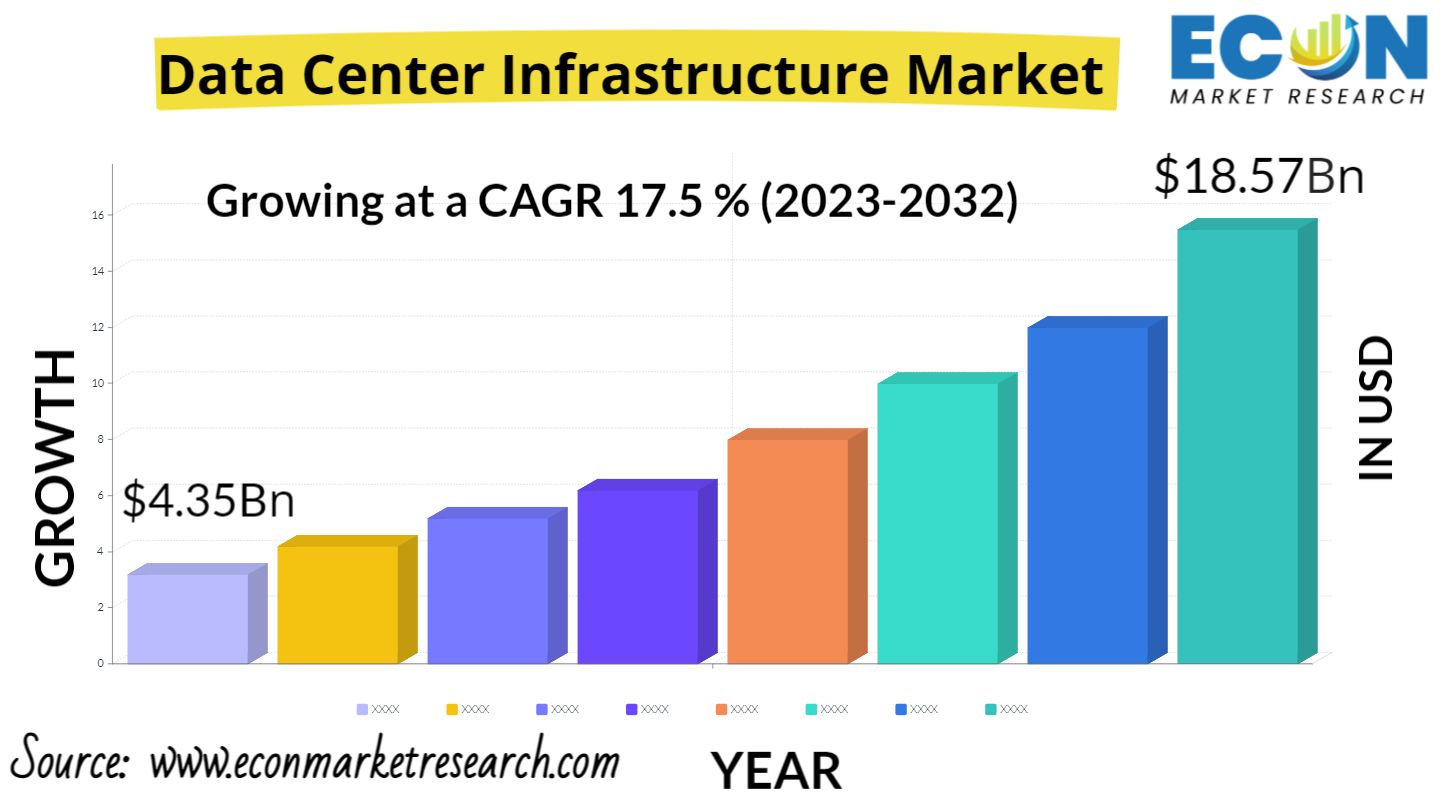

The global data center infrastructure market in 2022 was valued at USD 4.35 billion and is predicted to reach roughly USD 18.57 billion in 2032, rising at a compound annual growth rate (CAGR) of 17.5% between 2023 and 2032.

Data center infrastructure refers to the physical and hardware components that are required to run a data center. It includes all the facilities, equipment, and systems needed to support data processing, transmission, and archiving inside a data center. Servers, power infrastructure, cooling and environmental controls, fire suppression systems, etc. are some of the key elements of data center infrastructure. Data center infrastructure also provides security, which protects business and data.

The growth rate for small and medium-sized data centers and the rapidly expanding array of smaller data centers are the growth factors of data center infrastructure market. This is partly due to the rise of computing at the edge, which requires data processing closer to the end user. Smaller data centers are also more flexible and easier to manage than large ones. They can also be more cost-effective in terms of energy consumption and maintenance. In some cases, companies choose to establish microdata centers in unconventional locations, such as inside shipping containers or modular units. This trend is expected to continue as more data is generated and processed at the edge. However, there is still a significant need for larger data centers to support cloud computing and other centralized computing needs.

Data Center Infrastructure Market Report Scope & Segmentation

|

Report Attribute |

Details |

|

Estimated Market Value (2022) |

4.35 Bn |

|

Projected Market Value (2032) |

18.57 Bn |

|

Base Year |

2022 |

|

Forecast Years |

2023 – 2032 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- By Component Type, By Deployment Type, By Organization Size, By Application, & By Region |

|

Segments Covered |

By Component Type, By Deployment Type, By Organization Size, By Application, & By Region |

|

Forecast Units |

Value (USD Billion) |

|

Quantitative Units |

Revenue in USD billion and CAGR from 2023 to 2032 |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis, and COVID-19 impact analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Market Drivers

One of the primary drivers of the data center infrastructure market is the growing demand for cloud computing services. Cloud computing providers need to build and operate large data in order to store and process data for their customers. Cloud computing is expected to expand further in the upcoming years. Because cloud computing can help businesses save money on IT expenses. Businesses are not required to buy and maintain their own hardware and software, and they can scale their cloud usage up or down as needed. Cloud computing is more flexible than traditional IT solutions. Businesses can access cloud services from any location and quickly add and remove services as needed. Also cloud providers offer a high level of security, which is important for businesses that handle sensitive data.

According to the InfoWorld survey conducted in June 2020, it has been concluded that currently around 24% of IT applications are hosted on Cloud, but in the next 18 months it is about to grow by 36%, which is a huge rise, and these shifts are going to impact the data center infrastructure.

Market Restraints

The high cost of developing and operating data centers is a significant barrier to the market for data center infrastructure. Smaller businesses can find it more difficult to invest in their own data centers. Another issue is the lack of skilled IT professionals who can plan, build, and manage these complex facilities. The increasing adoption of cloud computing and edge computing solutions can also pose a threat to the data center infrastructure market. Environmental concerns, such as the energy consumption and carbon footprint of data centers, can also limit growth in the industry. Security concerns regarding cyber-attacks and data breaches are also a major challenge, as they can damage a company's reputation and compromise important data.

Market Opportunities

Data center infrastructure providers are developing new technologies to more efficiently and reliably store & process big data. These technologies include new types of storage hardware, data analysis software, and networking solutions. To accommodate the increased demand for big data and AI, data center infrastructure providers are building new data centers. These data centers are typically located in areas with low power costs and cool climates. Data center infrastructure providers are partnering with cloud computing providers to offer big data and AI solutions to businesses. These solutions enable businesses to access big data and artificial intelligence capabilities without having to build and operate their own data centers. Therefore, the rise of big data and artificial intelligence represents a good opportunity for data center infrastructure providers. By developing new technologies and partnering with cloud computing providers.

Segments Analysis:

Component Insights

The global data center infrastructure market segmentation by component includes hardware, software, and service. The market is dominated by the hardware segment, and demand for high-quality hardware equipment will fuel market expansion. The rising popularity of micro, cloud, and edge data centers has increased the requirement for high-quality IT infrastructure that can adapt to changing end-user demands.

Deployment Insights

Deployment insights include on-premise, and cloud. The on-premises segment accounted for the largest share in 2022 and is expected to continue to dominate over the forecast period. On-premises are based on the physical environment and are important for the organization. On-premises deployment makes it possible to monitoring data on power consumption, humidity, airflow, and other aspects of data centers operations. Monitor each of these variables is essential for organizations to avoid downtime, loss of revenue, or loss of data.

End Users Insights

Based on end users, the global data center infrastructure market segmentation includes BFSI, Retail, IT & telecom, healthcare, energy, government, and manufacturing. The IT & telecom category generated the most income because they are essential for the operation of data centers. IT & telecom includes servers, storage devices, networking equipment, and power & cooling systems. Also they provide the foundation on which all other components are built. Without IT and telecom, data centers would not be able to function.

Regional Analysis

North America held more than 40% of the worldwide market for data center infrastructure. The rising use of cloud computing, big data, and artificial intelligence are the growth factors of data centers infrastructure expansion in North America. The United States is the largest market for data center infrastructure in North America, followed by Canada.

Also, Europe is the second-largest market for data center infrastructure. The growth of the market in Europe is driven by the increasing adoption of cloud computing, big data, and artificial intelligence. The United Kingdom is the largest market for data center infrastructure in Europe, followed by Germany and France.

Competitive Landscape:

The data center infrastructure market is fragmented, with many small and large players offering a range of products and services. Dell EMC, Hewlett Packard Enterprise, IBM, and Cisco are some of the major players in this sector. However, there are many smaller companies that specialize in specific parts of data center infrastructure, such as data storage, server hardware, and networking equipment. Due to the rapid growth in demand for data center services, the market is expected to remain highly competitive.

Key Market Players:

Recent Development:

Data Center Infrastructure Market Report Segmentation

|

ATTRIBUTE |

DETAILS |

|

By Component Type |

|

|

By Deployment Type |

|

|

By Organization Size |

|

|

By End Users |

|

|

By Region |

|

|

Customization Scope |

|

|

Pricing |

|

Key Benefits of the Report

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.