Global Autonomous Vehicle Market Research Report: By Level of Automation (Level 3, Level 4, Level 5), By Application (Civil, Robo Taxi, Ride Share, Ride Hail, Self-Driving Truck, Self-Driving Bus), By Component (Hardware, Software and Services), and Region (North America, Europe, Asia-Pacific, and Rest of the World) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2024-2032.

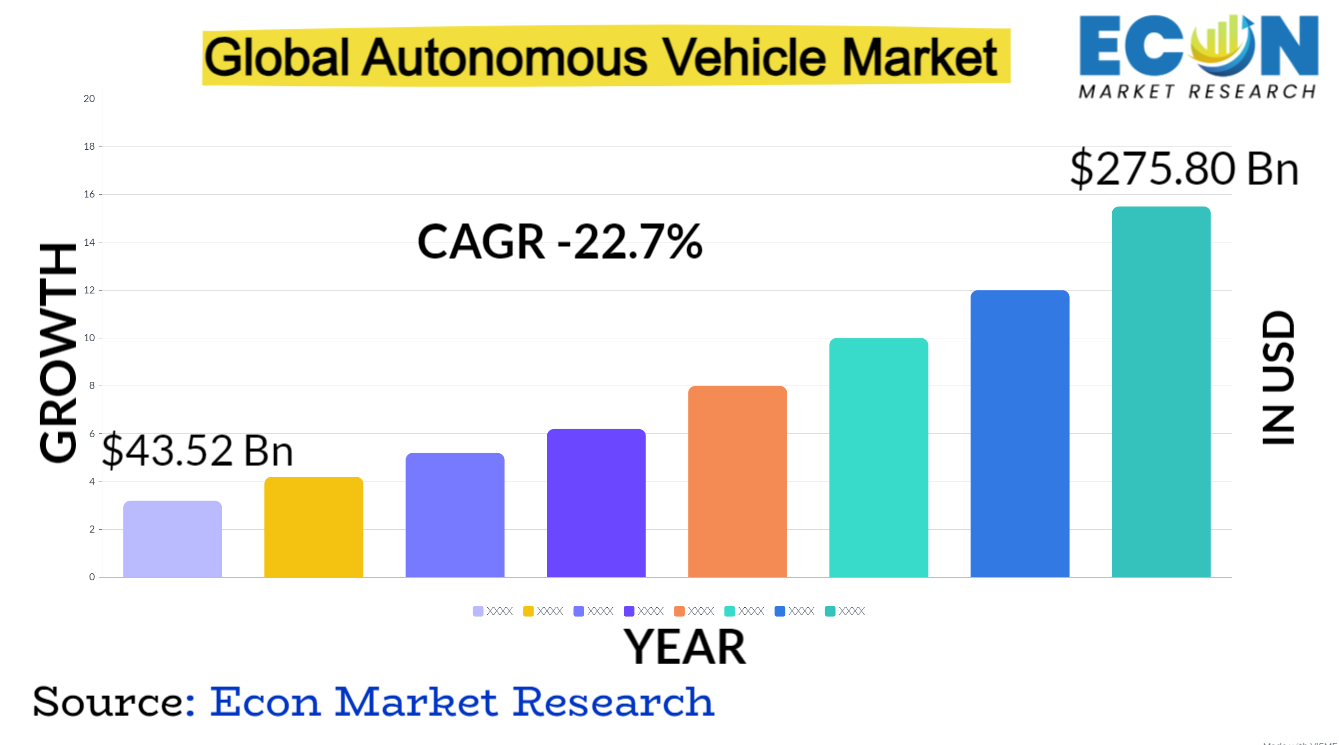

The global autonomous vehicle market was valued at USD 43.52 billion in 2023 and is estimated to reach approximately USD 275.80 billion by 2032, at a CAGR of 22.7% from 2024 to 2032.

Transportation is entering a transformational era with the introduction of autonomous vehicles. This innovative technology, which began to take shape in the early 2000s with prototype advancements by tech behemoths and automakers, sought to redefine mobility through the incorporation of advanced computing systems, artificial intelligence, and sensors into automobiles. Early adoption was conservative, with few trials and feasibility and safety-focused experimental ventures. But when the technology advanced and showed that it might completely transform sectors, funding poured in, driving the market for autonomous vehicles forward. Automakers such as GM and Ford, along with startups like Tesla and Waymo, entered the market and shown different degrees of autonomy, ranging from partially driverless systems to assisted driving. Obstacles included ethical issues, public acceptance, and regulatory concerns; however, advancements in sensor technology, machine learning, and infrastructural development hastened the process. By the middle of the 2010s, public testing and pilot programs had become more widespread, progressively influencing public opinion and opening the door for the incorporation of autonomous vehicles into regular transportation. With this introduction, a new age that would fundamentally alter urban planning, mobility, and transportation itself began.

AUTONOMOUS VEHICLE MARKET: REPORT SCOPE & SEGMENTATION

|

Report Attribute |

Details |

|

Estimated Market Value (2023) |

43.52 Bn |

|

Projected Market Value (2032) |

275.80 Bn |

|

Base Year |

2023 |

|

Forecast Years |

2024 - 2032 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- By Level of Automation, By Application, By Component, & Region |

|

Segments Covered |

By Level of Automation, By Application, By Component, & Region |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2024 to 2032 |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, and the Rest of World |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis, and COVID-19 impact analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Global Autonomous Vehicle Market Dynamics

The limits of autonomous driving are constantly being pushed by developments in data processing, sensor technology, and artificial intelligence. Businesses fight for the top spot, which leads to fierce rivalry and partnerships between tech companies, automakers, and startups. Research and development expenditures are heavily invested in, hastening the transition of semi-autonomous to fully autonomous systems. Governments all across the world navigate safety standards, liability difficulties, and infrastructure preparation through regulatory frameworks, which are crucial. The market's trajectory is shaped by policy modifications and pilot projects, which have an impact on industry participants' testing possibilities and market entry strategies. Market dynamics are also significantly impacted by consumer acceptance and trust. To encourage widespread usage, public awareness campaigns, safety demonstrations, and user experience enhancements are essential. Pricing and market accessibility are influenced by economic variables, such as industrial economies of scale and cost reductions in sensor technology. Collaborations with logistics firms and ride-hailing services propel business applications and mold consumer demand. The constantly changing autonomous vehicle industry is shaped by the interaction of five factors: customer attitude, regulatory frameworks, technology innovation, and economic forces.

Global Autonomous Vehicle Market Drivers

Advances in artificial intelligence, namely in the fields of machine learning and neural networks, have made it possible for cars to comprehend and react to intricate situations in real time. Advanced sensor technologies, such as LiDAR, radar, and cameras, provide enhanced perception skills that enable cars to recognize and traverse a variety of situations more precisely. Improvements in computing power enable quicker data processing and decision-making, which is essential for guaranteeing the effectiveness and safety of autonomous systems. Furthermore, the incorporation of cutting-edge connectivity options, such 5G networks, enables cars to interact with infrastructure and one another, improving navigation and general operational capabilities. The capabilities of autonomous vehicles are greatly enhanced as a result of the convergence and maturation of various technologies, which also push the envelope in terms of safety, dependability, and speeding up the development of completely autonomous transportation systems. The industry's continued rapid advancement, investment, regulatory framework development, and eventual transformation of the transportation landscape are all largely attributed to the unrelenting speed of technology innovation.

Globally, as a result of demographic changes, there are an increasing number of elderly people, necessitating the need for transportation options that meet their unique requirements. For elderly and other people with mobility issues, autonomous cars offer a safe and practical mobility choice. This is a potential answer. These cars can meet a variety of accessibility standards by providing amenities including simple access and departure, movable seats, and support for people with impairments or restricted movement. Furthermore, in underserved or distant places where access to conventional transportation may be limited, autonomous cars solve the issue of transportation availability. Autonomous vehicles can help senior citizens stay independent by allowing them to go to important places, get medical care, and go to social events without having to rely on public transportation or traditional driving. For companies that create and provide services for autonomous vehicles, this shift in demographics offers a substantial business opportunity. In addition to meeting a social need, meeting the demands of an aging population encourages innovation in user interfaces, safety measures, and vehicle design, which eventually makes transportation more inclusive and accessible for all.

Restraints:

Substantial financial investments are necessary for the extensive research and development needed to construct advanced autonomous systems. Significant resources are needed for software development, computer infrastructure, and cutting-edge sensor technology. Moreover, extensive testing raises costs, particularly when it comes to guaranteeing dependability and safety. These expenses are additionally increased by the complexity of optimizing algorithms to manage uncertain real-world situations. There are financial difficulties in scaling up manufacturing to satisfy market needs while upholding high standards of quality. The long-term cost burden is further increased by the requirement for ongoing upgrades and updates to stay up with the rapidly changing state of technology. Due to the entry hurdles created by these high development costs, innovation and market competitiveness are constrained. The autonomous vehicle market requires strategic planning, collaboration, and potential cost-reduction strategies to promote broader accessibility and affordability. This is because the industry's reliance on ongoing technological breakthroughs drives up these prices.

There is a lack of consistency among jurisdictions and regions in the constantly changing legislation and policies concerning infrastructure readiness, liability, and safety standards. Manufacturers and developers striving for uniform testing and deployment procedures face difficulties due to differing regulatory regimes. The legal complexity resulting from uncertainties regarding culpability in the event of accidents involving autonomous vehicles impede the advancement of the business. Furthermore, the rate of technical progress frequently surpasses the rate at which regulatory frameworks are developed, resulting in a delay in the adaptation of laws to new capacities and challenges. One of the biggest challenges facing policymakers is continuing to strike a balance between protecting public safety and promoting innovation. It is imperative that uniform laws address cybersecurity, safety, and moral issues while encouraging innovation and commercial expansion. Governments, industry players, and advocacy organizations must work together to create comprehensive, flexible, and uniform regulatory frameworks that support the responsible development of autonomous vehicle technology in order to overcome these regulatory obstacles.

Opportunities:

The seamless integration of autonomous cars into urban environments, which would revolutionize transportation networks and urban planning, is made possible by smart city integration. Cities can improve overall mobility, lessen gridlock, and optimize traffic flow by integrating autonomous cars into smart city efforts. These cars can interact with smart infrastructure, such traffic lights and road sensors, thanks to their sophisticated sensors and connectivity, which makes for safer and more effective navigation. Furthermore, by lowering the dependency on private vehicles and alleviating urban traffic congestion, autonomous ridesharing and public transportation services may provide more adaptable, practical, and environmentally responsible mobility options. Furthermore, autonomous vehicle data can be used by smart cities to plan infrastructure improvements, evaluate traffic patterns, and optimize transit routes. The goals of a smart city, which include efficiency, sustainability, and better quality of life, are all in line with this integration. To fully utilize autonomous cars inside smart city frameworks and create more livable, accessible, and sustainable urban settings, cooperation between city planners, technology developers, and transportation authorities is crucial.

People can access a network of linked mobility alternatives by integrating autonomous vehicles into MaaS platforms. This allows autonomous vehicles, ridesharing, and public transportation to be smoothly integrated into a single, user-centric system. This connection lessens the need for personal vehicles and eases urban traffic congestion by enabling optimal, customized, and on-demand mobility solutions. MaaS frameworks with autonomous cars provide efficient and adaptable travel experiences. Through mobile apps, users may plan complete trips involving a variety of smoothly connected means of transportation. To improve accessibility to public transportation hubs, autonomous shuttles or ride-hailing services, for example, could offer first- and last-mile connection. Furthermore, by optimizing routes and resource use, MaaS platforms that deploy autonomous vehicles may save users money. In order to promote sustainability and lessen its impact on the environment, this model pushes people to switch from owning cars to mobility subscriptions or pay-per-use services. Realizing the full potential of MaaS with autonomous vehicles, improving urban mobility, lowering traffic congestion, and creating a more effective, sustainable, and user-friendly transportation ecosystem all depend on partnerships between IT companies, transportation providers, and local authorities.

Segment Overview

By Level of Automation

Based on level of automation, the global autonomous vehicle market is divided into level 3, level 4, level 5. The level 5 category dominates the market with the largest revenue share in 2023. Level 5 represents the highest degree of autonomy, where vehicles can operate in all conditions and environments without human intervention. These vehicles are designed to perform all driving tasks, from navigating complex city streets to handling challenging weather conditions, without the need for human input. Level 5 vehicles lack traditional driving controls like steering wheels and pedals, as they are entirely self-driving and don't require human oversight. Vehicles at Level 3 are capable of automated driving in certain conditions but still require human intervention and oversight. The system manages most aspects of driving, such as acceleration, braking, and steering, in specific situations like highway driving. However, the driver must remain alert and be ready to take control when prompted by the system, particularly in complex or unpredictable scenarios. At Level 4, vehicles can operate autonomously in predefined or limited environments without human intervention. These vehicles can manage the entire driving task within specific geographic areas or under certain conditions, such as controlled city zones or highways. However, they might still have the option for a human driver to take over if necessary, but it's not a requirement for normal operation.

By Application

Based on the application, the global autonomous vehicle market is categorized into civil, robo taxi, ride share, ride hail, self-driving truck, self-driving bus. The self-driving truck category leads the global autonomous vehicle market with the largest revenue share in 2023. Autonomous trucks are designed for freight transportation and logistics, capable of operating without human intervention. These vehicles have applications in long-haul shipping, local delivery services, and logistics operations, aiming to increase efficiency and reduce human-related errors in transportation. Autonomous buses operate without a human driver, providing public transportation services within predefined routes or areas. These vehicles cater to urban and suburban transit needs, offering environmentally friendly and efficient mass transit options. Civil autonomous vehicles category encompasses autonomous vehicles used for civilian purposes, including personal cars, minivans, and other vehicles designed for individual or family transportation. These vehicles are envisioned for everyday commuting, leisure travel, and general transportation needs. Robo-taxis refer to autonomous vehicles deployed in taxi or ride-hailing services without human drivers. These vehicles can be hailed or summoned via an app, providing on-demand transportation services to passengers within a defined area or city. Ride-sharing involves autonomous vehicles utilized in shared transportation services where multiple passengers heading in similar directions share a vehicle. These services optimize routes and vehicle occupancy, reducing congestion and providing cost-effective transportation options. Similar to ride-share services, ride-hail autonomous vehicles operate on an on-demand basis, but they are hailed individually by passengers through apps or other means for point-to-point transportation.

By Component

Based on component, the global autonomous vehicle market is segmented into hardware, software and services. The hardware segment dominates the autonomous vehicle market. This segment includes the physical components and equipment required for autonomous vehicles to function. It encompasses various sensors (such as LiDAR, radar, cameras), onboard computing systems (central processing units, GPUs), connectivity hardware (communication modules, antennas), and other tangible components like actuators, control systems, and vehicle platforms. Hardware is crucial for gathering data, processing information, and executing actions necessary for autonomous driving. The software segment comprises the programming, algorithms, and operating systems that enable autonomous vehicles to perceive their environment, make decisions, and control their movements. This includes sensor fusion software that integrates data from multiple sensors, mapping and localization algorithms, artificial intelligence (AI) and machine learning for decision-making, and safety-critical software responsible for managing vehicle functions. Software development is essential for ensuring the vehicle's perception, navigation, decision-making, and control systems operate effectively and safely. Services segment involves the various ancillary offerings and support systems around autonomous vehicles. It encompasses a wide array of services, including but not limited to, data analytics, cybersecurity solutions, vehicle maintenance and repair, fleet management, mapping and geospatial services, remote monitoring and assistance, and customer support.

Global Autonomous Vehicle Market Overview by Region

The global autonomous vehicle market is categorized into North America, Europe, Asia-Pacific, and the Rest of the World. North America emerged as the leading region, capturing the largest market share in 2023. The area is home to a strong market for autonomous vehicles, significant investment, technological innovation, and favorable regulatory frameworks. A vibrant startup culture, major automakers, and tech behemoths have created a dynamic atmosphere that is conducive to innovation. large strides in autonomous car technology are being made by businesses with headquarters or large operations in North America, such as Waymo, Tesla, GM, and others. Furthermore, the region has seen significant expenditures in R&D, with governments, corporate investors, and venture capitalists funding projects involving autonomous vehicles. The rate of invention and commercialization of autonomous technology has increased as a result of these investments. Autonomous vehicle testing and deployment in controlled environments have been made easier by regulatory measures and pilot programs implemented in several states and provinces. Initiatives in states like Michigan, California, and Arizona have played a key role in developing testing sites and establishing rules for the use of autonomous vehicles. North America's leadership in autonomous vehicles is also a result of its consumers' acceptance of new technology and their preparation for the market. The infrastructure of the area, which consists of cutting-edge communication networks and encouraging laws, further establishes the region's leadership in influencing the direction of autonomous vehicles.

Global Autonomous Vehicle Market Competitive Landscape

In the global autonomous vehicle market, a few major players exert significant market dominance and have established a strong regional presence. These leading companies remain committed to continuous research and development endeavors and actively engage in strategic growth initiatives, including product development, launches, joint ventures, and partnerships. By pursuing these strategies, these companies aim to strengthen their market position, expand their customer base, and capture a substantial share of the market.

Some of the prominent players in the global autonomous vehicle market include AB Volvo; Bayerische Motoren Werke AG; Ford Motor Company; General Motors; Hyundai Motor Group; Mercedes-Benz AG; Renault SA; Tesla,Inc; Toyota Motor Corporation; Volkswagen Group, and various other key players.

Global Autonomous Vehicle Market Recent Developments

Autonomous Vehicle Market Report Segmentation

|

ATTRIBUTE |

DETAILS |

|

By Level of Automation |

|

|

By Application |

|

|

By Component |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Objectives of the Study

The objectives of the study are summarized in 5 stages. They are as mentioned below:

To identify and estimate the market size for the global autonomous vehicle market segmented by level of automation, by application, by component, region and by value (in U.S. dollars). Also, to understand the consumption/ demand created by consumers of autonomous vehicle between 2019 and 2032.

To identify and infer the drivers, restraints, opportunities, and challenges for the global autonomous vehicle market

To find out the factors which are affecting the sales of autonomous vehicle among consumers

To identify and understand the various factors involved in the global autonomous vehicle market affected by the pandemic

To provide a detailed insight into the major companies operating in the market. The profiling will include the financial health of the company's past 2-3 years with segmental and regional revenue breakup, product offering, recent developments, SWOT analysis, and key strategies.

Intended Audience

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.