Global Automotive Powertrain Market Research Report: By Propulsion Type (ICE, Electric Vehicle), By Vehicle Type (Passenger Vehicle, Commercial Vehicle), and Region (North America, Europe, Asia-Pacific, and Rest of the World) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2024-2032.

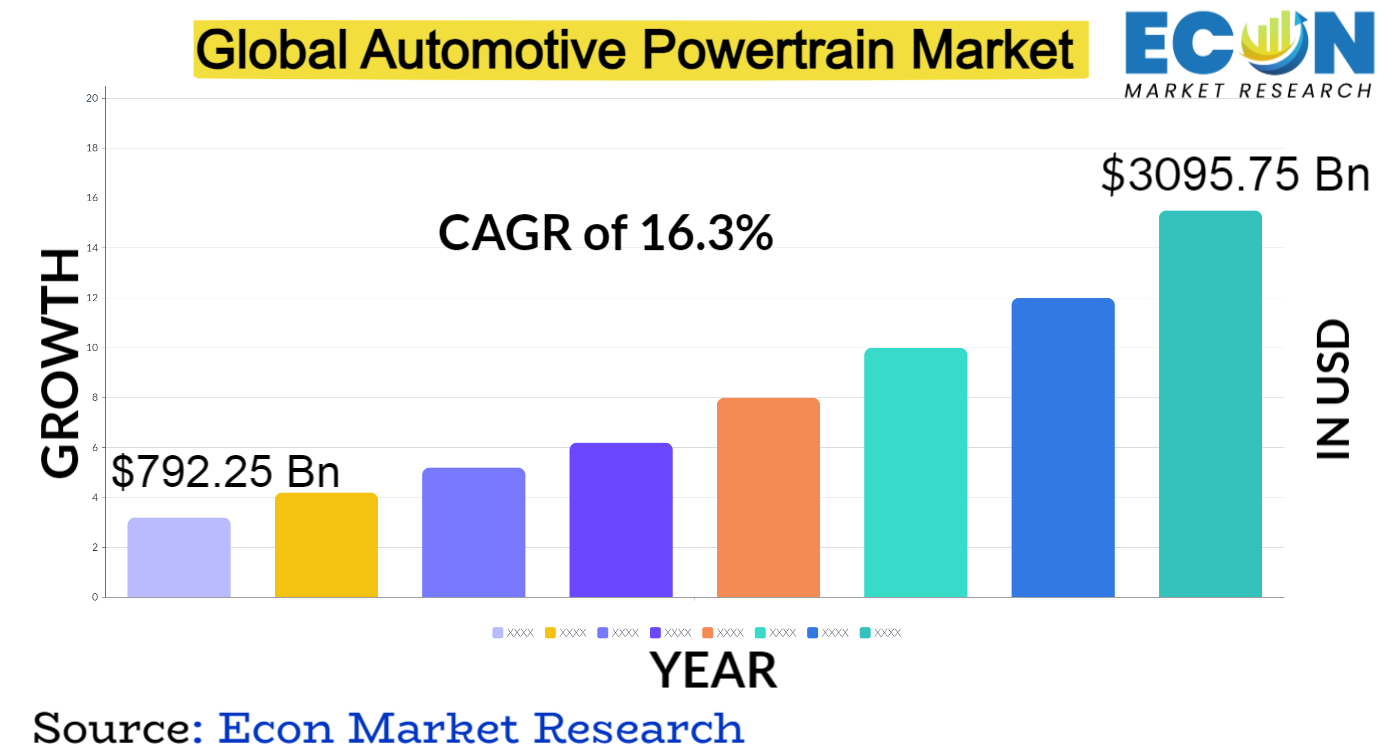

The global automotive powertrain market was valued at USD 792.25 billion in 2023 and is estimated to reach approximately USD 3095.75 billion by 2032, at a CAGR of 16.3% from 2024 to 2032.

The market for automotive powertrains includes all of the essential parts that drive cars, such as engines, transmissions, and related technologies. Acting as the vehicle's nervous system, it transforms energy into motion and sets performance parameters. Advances have caused a significant shift in powertrain technology over time. Hybrid systems, electric motors, and fuel cells have been added to conventional internal combustion engines to improve efficiency, lower emissions, and satisfy changing consumer needs.

The move toward electrification has had a particularly significant effect, encouraging advancements in electric drivetrains and battery technologies. Powertrain manufacturers always work to optimize their products for performance, sustainability, and dependability while also taking into account customer preferences and strict environmental requirements. The automotive powertrain market is ripe for more upheaval as the industry moves farther toward electric and hybrid technologies. This sector will define transportation in the future by fusing efficiency, sustainability, and innovation.

AUTOMOTIVE POWERTRAIN MARKET: REPORT SCOPE & SEGMENTATION

|

Report Attribute |

Details |

|

Estimated Market Value (2023) |

792.25 Bn |

|

Projected Market Value (2032) |

3095.75Bn |

|

Base Year |

2023 |

|

Forecast Years |

2024 - 2032 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- By Propulsion Type, By Vehicle Type, & Region |

|

Segments Covered |

By Propulsion Type, By Vehicle Type, & Region |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2024 to 2032 |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, and the Rest of World |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis, and COVID-19 impact analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Global Automotive Powertrain Market Dynamics

An important shift has occurred as a result of the growing focus on sustainability, which has accelerated the development of electric and hybrid drivetrains. Globally enforced pollution regulations have compelled manufacturers to make significant investments in electrification, resulting in a boom in the development of electric vehicle (EV) technology and infrastructure. At the same time, improvements to internal combustion engines keep improving their performance and efficiency, reaching markets where the adoption of electric vehicles may be more difficult or delayed.

The powertrain environment is also influenced by geopolitical issues, fuel prices, and global economic conditions, which affect industry investments and consumer purchasing patterns. Powertrain development is further influenced by the increasing demand for autonomy and connection, which calls for the integration of sophisticated sensors and control systems. The automotive industry is fiercely competitive, with both new and old giants fighting to innovate and take market share. It is now typical for established automakers, tech firms, and startups to work together, which promotes cross-industry knowledge and creative ideas. Industry participants must constantly adapt and innovate as the automobile powertrain sector is always changing due to shifting legislation and consumer preferences toward sustainability and performance.

Global Automotive Powertrain Market Drivers

The swift progress of electric powertrains can be attributed mainly to a worldwide confluence of variables that prioritize efficiency, sustainability, and technological innovation. The global shift towards electric vehicles (EVs) has been driven by stricter emissions restrictions and more environmental consciousness. This has led to substantial investments and research into developing electric powertrains. This impetus is reinforced by the fact that battery technology is becoming more widely available and efficient, as evidenced by breakthroughs in cost-effectiveness, energy density, and charging infrastructure.

The market's attraction to electric vehicles has increased due to consumer demand for greener, more sustainable modes of transportation, which is driving automakers and tech firms to accelerate the development of electric powertrains. Industry alliances, including those between tech companies and automakers, have created an atmosphere that is favorable to quick invention and has led to advancements in the performance, range, and cost of electric vehicles.

Powertrain design and functionality have undergone revolutionary changes as a result of advances in materials science, computer power, and engineering methods. Advancements such as continuously variable gearboxes, direct fuel injection, variable valve timing, and smaller turbocharged engines have greatly improved internal combustion engine performance and fuel efficiency. Furthermore, the combination of advanced battery management systems, regenerative braking, and electric propulsion in hybrid and electric powertrains has completely changed the game by providing options that are cleaner and more energy-efficient. Smarter powertrains that can analyze data in real-time, do predictive maintenance and maximize performance are other results of developments in software and networking. These developments are fueled by partnerships between IT and automotive businesses, and they have a major impact on the development of improved driver-assistance systems and autonomous cars, both of which depend largely on cutting-edge engine technologies. This ongoing development, spurred by technical advancements, not only satisfies efficiency and emissions regulations but also molds consumer expectations, pushing the car sector toward more environmentally friendly and cutting-edge powertrain options.

Restraints:

Despite impressive progress, there are still gaps in several important domains. As it is difficult to increase the quantity of energy stored per unit weight or volume without appreciably raising prices, energy density is still the key problem. Because recharging batteries takes longer than fueling internal combustion vehicles, there are additional constraints on charging infrastructure and speed that affect consumer acceptance and adoption rates. Another major barrier is cost, as the creation of high-capacity batteries raises the price of EVs by requiring costly components like nickel, cobalt, and lithium. Concerns about sustainability and ethics are also raised by the effects of resource misuse on the environment. Another limitation is longevity and durability; batteries deteriorate with time, affecting both their overall performance and lifespan and requiring expensive replacements. Collectively, these obstacles prevent electric powertrains from being widely used. Therefore, coordinated research and development efforts are needed to address battery technology limitations and optimize battery efficiency, cost, and sustainability for a smoother transition to electric mobility.

Events like flooding, political unrest, or worldwide health emergencies can upend the complex network of suppliers, leading to delays and shortages of vital resources like semiconductors, rare-earth metals, and specialty components. These interruptions have an impact on assembly lines, the production of powertrains, and eventually, the creation of vehicles in the automotive sector. These difficulties are made more difficult by the interconnectedness of global supply chains, which makes providers or certain regions more susceptible to unanticipated events or changes in geopolitics. In an attempt to cut inventory costs, the just-in-time manufacturing paradigm increases the impact of disruptions and provides minimal cushioning against unforeseen delays. These disruptions cause delays in production plans and increase prices because of accelerated shipment, sourcing from other sources, or idle manufacturing lines. To ensure smoother operations and continuity within the automotive powertrain market, mitigating supply chain disruptions requires diversifying suppliers, embracing digitalization for real-time visibility and flexibility, and putting risk management strategies into practice to build resilience against unforeseen disruptions.

Opportunities:

The automobile powertrain area offers significant prospects for software integration and data management, which have the potential to transform vehicle performance, efficiency, and user experience. The amalgamation of sophisticated software skills and automotive engineering presents an array of opportunities. Predictive maintenance is made possible by real-time data analytics, which maximizes engine health and minimizes downtime.

The energy management systems in electric vehicles are made easier by complex algorithms, which increase efficiency and range. Adaptive powertrain controls, which modify performance in response to road conditions or driver preferences, are another feature of software-driven solutions that improve driving experiences. Powertrains are now even more equipped to continuously learn and improve operations, improving economy and performance over time, thanks to the integration of artificial intelligence (AI) and machine learning. Data-driven insights open doors to customized services beyond vehicle-centric apps, such as customized energy usage feedback for drivers to maximize efficiency.

To decrease emissions and increase fuel efficiency, these systems combine electric power and internal combustion engines. Bridging the gap till complete electrification is one important opportunity. Without making the entire switch to an all-electric car, hybrid systems provide users with a stepping stone toward greater efficiency and less environmental effect. This strategy addresses worries about range anxiety and the constraints of pure electric vehicle charging infrastructure while being in line with changing consumer preferences for more environmentally friendly transportation options. Additionally, by offering incremental efficiency increases without the complexity and expense of fully hybrid systems, the development and integration of mild hybrid technologies provide an intermediary answer. Manufacturers may use these technologies to offer consumers real benefits in the form of fuel savings and a smaller carbon footprint, all while complying with the world's stricter emissions rules. Opportunities to further optimize these systems through the use of renewable energy sources, improved energy recuperation, and increased battery efficiency present themselves as technology develops, opening up new avenues for innovation and market expansion in the vehicle powertrain sector.

Segment Overview

By Propulsion Type

Based on propulsion type, the global automotive powertrain market is divided into ICE, and electric vehicle. The ICE category dominates the market with the largest revenue share in 2023. ICE cars run on conventional combustion engines powered by diesel or gasoline. Internal combustion of fuel produces the power needed to move the car with these engines. ICE vehicles come in a variety of forms, such as hybrid systems that combine internal combustion engines with electric motors, as well as gasoline- and diesel-powered vehicles. A variety of cars that are either fully or partially powered by electricity are referred to as electric vehicles, or EVs. They fall into two categories: Plug-in Hybrid Electric Vehicles (PHEVs), which combine an internal combustion engine and an electric motor and can be charged externally, and Battery Electric Vehicles (BEVs), which run entirely on electricity stored in large-capacity batteries.

By Vehicle Type

Based on the vehicle type, the global automotive powertrain market is categorized into passenger vehicles, and commercial vehicles. The passenger vehicle category leads the global automotive powertrain market with the largest revenue share in 2023. Cars, SUVs, crossovers, and other vehicles primarily intended for passenger transportation fall under this category. Passenger cars are meant for individual or family travel, as well as personal use.

Powertrains in this class come in a wide range of configurations, including plug-in hybrids, conventional internal combustion engines (diesel or gasoline), hybrid systems, and entirely electric powertrains. In order to satisfy the varied demands and tastes of different customers, the passenger car market frequently places a strong emphasis on elements like performance, comfort, fuel economy, and technological innovations. Commercial vehicles, such as trucks, buses, vans, and specialty vehicles used for moving cargo, people, or carrying out particular jobs, are built for business or commercial use. Public services, construction, logistics, and transportation are just a few of the sectors these cars serve. Commercial vehicle powertrains are diverse, meeting a range of purposes. For example, heavy-duty engines are used for freight transportation, more efficient systems are used for urban delivery vans, and environmentally aware fleets might choose electric or hybrid cars.

Global Automotive Powertrain Market Overview by Region

The global automotive powertrain market is categorized into North America, Europe, Asia-Pacific, and the Rest of the World. Asia-Pacific emerged as the leading region, capturing the largest market share in 2023. The popularity of the region has been boosted by its strong automotive industry, significant industrial capabilities, and growing consumer market. China, Japan, South Korea, and India are important nations because they have substantial consumer demand and vast production capacities. Furthermore, policies encouraging the use of electric vehicles and stricter emissions controls have sped up the development of powertrain technologies, positioning Asia-Pacific as the leading region in the global automotive powertrain market and serving as a center for innovation and development in the automotive industry.

The automotive powertrain industry in North America is expected to grow at the highest compound annual growth rate (CAGR) over the predicted timeframe. The use of electric vehicles is booming in the area, fueled by favorable government regulations that encourage electric mobility and rising environmental consciousness. This expansion is further supported by technological advancements, partnerships between tech businesses and manufacturers, and an expanding infrastructure for electric vehicle charging. Furthermore, this predicted quick development is fueled by North America's emphasis on innovation, battery technology research, and a move toward sustainable transportation, which positions the region as a major role in pushing the advancement of automotive powertrains.

Global Automotive Powertrain Market Competitive Landscape

In the global automotive powertrain market, a few major players exert significant market dominance and have established a strong regional presence. These leading companies remain committed to continuous research and development endeavors and actively engage in strategic growth initiatives, including product development, launches, joint ventures, and partnerships. By pursuing these strategies, these companies aim to strengthen their market position, expand their customer base, and capture a substantial share of the market.

Some of the prominent players in the global automotive powertrain market include,

Global Automotive Powertrain Market Recent Developments

Scope of the Global Automotive Powertrain Market Report

Automotive Powertrain Market Report Segmentation

|

ATTRIBUTE |

DETAILS |

|

By Propulsion Type |

|

|

By Vehicle Type |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Objectives of the Study

The objectives of the study are summarized in 5 stages. They are as mentioned below:

Intended Audience

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.