Automotive Infotainment Market by Technology (Human-Machine Interface (HMI) sensing, seamless wireless connectivity and others), Installation (Original Equipment (OE) fitted and aftermarket.), Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, and Forecast 2023-2031.

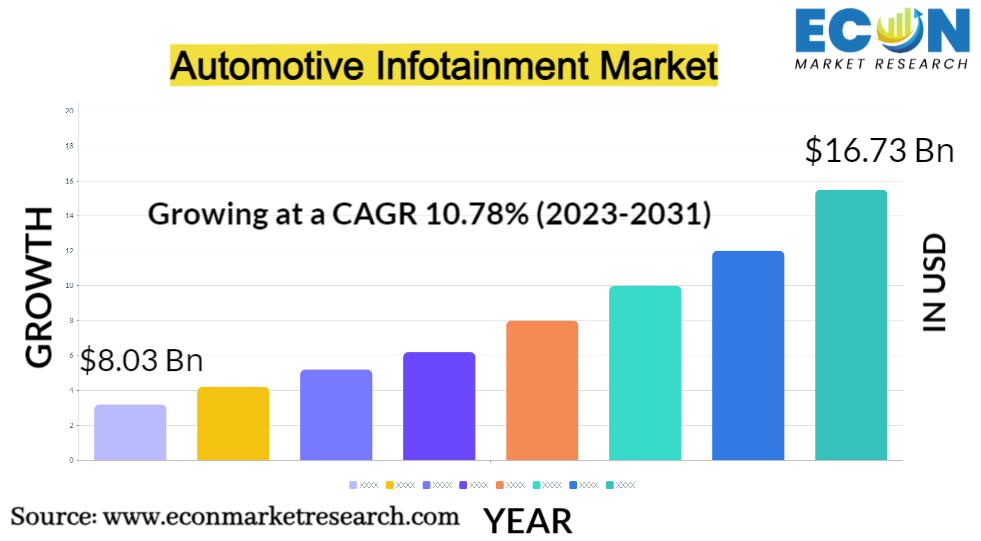

The Global Automotive Infotainment Market was worth USD 8.03 billion in 2022, would rise to USD 16.73 billion by 2031 and it is predicted to grow at a 10.78% CAGR from 2023 to 2031. The global automotive infotainment industry includes the integration of entertainment, information, and connectivity systems in vehicles. It offers a wide range of technologies and functions that improve the driving experience and give passengers alternatives for connectivity, navigation, entertainment, and more. Automotive infotainment systems offer voice control, gesture recognition, touchscreen displays, GPS navigation, hands-free calling, smartphone connectivity, audio and video entertainment, and hands-free calling. They make it possible for users to view media, manage settings, and maintain connectivity while travelling. Technological improvements, rising customer desire for connected features, and the incorporation of sophisticated driver aid systems all drive the industry. Innovative infotainment solutions are provided to the worldwide automobile industry through collaboration between car manufacturers, technology providers, and software developers.

Segments Analysis

Installation type:

Based on installation type global car infotainment market can segmented into two fit categories: aftermarket and Original Equipment (OE) fitted. During the production process, infotainment systems are integrated into automobiles and pre-installed by automakers. These technologies effortlessly integrate with the overall interior design because they are uniquely tailored and optimised for the vehicle's make and model. However, aftermarket entertainment systems are installed in automobiles after the initial purchase and are purchased separately. Users can enhance their current infotainment capabilities owing to their adaptability and interoperability with a variety of vehicle models. Both fit styles cater to distinct consumer preferences, with aftermarket systems offering customization options and flexibility while OE fitted systems offer seamless integration.

Vehicle Type Insights:

Depending on the kind of vehicle, the automotive infotainment industry can be divided into two major categories: Passenger automobiles and commercial vehicles. Sedans, SUVs, and hatchbacks are just a few examples of the diverse types of cars that fall under the category of passenger cars and are mostly utilised for personal transportation.

Due to consumer demand for cutting-edge connection, entertainment, and convenience features, these vehicles present a large market opportunity for infotainment systems. Particularly in terms of providing top-of-the-line infotainment systems with a variety of cutting-edge capabilities, luxury cars shine. High-definition touchscreens, surround sound systems, voice recognition technology, cutting-edge navigation systems, and in-car Wi-Fi access are a few of these. The incorporation of cutting-edge entertainment systems meets the demands of luxury automobile owners for a high-end and immersive in-car experience while also enhancing their comfort and enjoyment. Infotainment systems are also becoming more prevalent in the commercial vehicle category.

Regional analysis:

Asia Pacific is expected to maintain its leadership in the global automotive infotainment market. This projection is based on the anticipation of sustained high sales volume of automobiles in the region and a further rise in the adoption of electric vehicles, particularly in countries like China and Japan. Original Equipment Manufacturers (OEMs) are likely to intensify their efforts to increase production volumes and embrace rapid technological advancements in manufacturing facilities, especially in emerging regions such as China and India.

Europe is anticipated to represent the second-largest share of this market, which is mostly due to the presence of major OEMs in the area and the region's vast vehicle manufacturing, both of which have fueled market expansion in this region.

Market Dynamics

Market Growth Factors:

The popularity of autonomous and electric vehicles is one of the factors driving the automotive infotainment market. The demand for cutting-edge infotainment systems to provide passengers with entertainment, connectivity, and customised experiences is increasing as self-driving and electrified vehicles become more common. Additionally, the incorporation of infotainment elements in autonomous vehicles can improve the overall in-car experience by enabling passengers to partake in a variety of activities while the car handles the driving, which will further fuel the market expansion of automotive infotainment.

Technological Advancements:

Rapid technological advances, such as the incorporation of artificial intelligence, augmented reality, and better networking choices, are propelling the vehicle infotainment market forward. These advancements allow for the development of more modern and feature-rich infotainment systems that provide improved user experiences and extended functionalities.

Increasing Consumer Demand:

Consumer desire for connectivity, entertainment, and comfort elements in cars is rising. Modern drivers and passengers anticipate seamless smartphone integration, streaming service access, voice control functionality, and cutting-edge navigation systems. As a result, automakers are concentrating on implementing sophisticated infotainment systems to suit these demands, which is driving the market's expansion.

Market Opportunities:

The market for car infotainment offers several opportunities for expansion and innovation. The development of cutting-edge connectivity features, such the incorporation of 5G technology, which allows for continuous communication and data interchange between vehicles, infrastructure, and the cloud is major opportunity. Personalised user experiences, predictive analytics, and intelligent voice assistants are also made possible by the combination of artificial intelligence (AI) and machine learning (ML) technologies. An opportunity to create infotainment systems catered to the particular requirements of EV drivers, such as real-time charging station information and energy management systems, is also presented by the expanding demand for electric vehicles. Additionally, by delivering interactive and immersive material, the combination of augmented reality (AR) and virtual reality (VR) technologies can completely change the driving experience.

Market Challenges:

The quick speed of technical improvement and the requirement for constant innovation prove to be a significant challenge for the vehicle infotainment business. Consumer expectations for more complex and powerful infotainment systems rise along with technological advancement. For automakers and developers of infotainment systems, meeting these expectations and providing cutting-edge features and functionality might be difficult. It can be difficult and time-consuming to ensure compatibility and easy integration with different hardware, operating systems, and networking standards. The difficulty facing the vehicle infotainment sector is further increased by the need to integrate new technology while guaranteeing user-friendly interfaces and preventing driver distraction. As part of the design and deployment of vehicle infotainment systems, it is also imperative to handle cybersecurity issues and ensure data privacy and protection.

Technology Landscape:

Systems for automotive infotainment use a range of technologies to provide a connected and immersive experience. For user-friendly interactions, these include intuitive Human-Machine Interface (HMI) sensing, seamless wireless connectivity for integration with mobile devices and online services, secure data access protocols to protect user privacy, dependable high-performance computing and storage for effective data processing, power technologies for optimised power management, and software solutions that follow the trend of software-defined vehicles and centralised system architecture. Automotive infotainment systems make advantage of these technologies to offer cutting-edge features, seamless connectivity, and a customised user experience, improving the overall driving experience.

Competitive Landscape:

The presence of significant players like Pioneer and Harman has influenced the competitive environment in the vehicle infotainment sector. These businesses consistently work to offer novel infotainment solutions, together with other well-known automobile manufacturers and tech firms. Intuitive user interfaces, defining technologies, and seamless connectivity are all priorities for them in their competition. Companies frequently form alliances and collaborations in addition to their own R&D projects to take use of one another's advantages and boost innovation. Companies are competing to provide a variety of applications and services that improve the overall driving experience in the software development and app ecosystems. The competition in the vehicle infotainment business is very fierce and ever-changing due to ongoing technology developments and changing consumer preferences.

Regulatory Environment:

To meet the increasing integration of technology in automobiles, the regulatory framework surrounding automotive infotainment is expanding. Governments and regulatory authorities are recognising the importance of ensuring the safety, privacy, and security of entertainment systems. In the United States, for example, the National Highway Traffic Safety Administration (NHTSA) has established guidelines and rules aimed at reducing driver attention caused by infotainment systems. These standards establish criteria for user interfaces that are safe and accessible, voice command functionalities, and visual display limits. Furthermore, data privacy and security regulations are being enforced in order to protect personal information acquired and transferred by infotainment systems. Regulatory organisations are constantly changing to guarantee that automobile infotainment systems fulfil the appropriate safety and privacy standards as technology improves.

Key Players:

Automotive Infotainment Market Report Segmentation:

|

Report Attribute |

Details |

|

Estimated Market Value (2022) |

USD 8.03 Billion |

|

Projected Market Value (2031) |

USD 16.73 billion |

|

Base Year |

2022 |

|

Forecast Years |

2023- 2031 |

|

Scope of the Report |

Forecast Trends, Industry Drivers and Restraints, Forecast Market Analysis by Segment- By Technology, By Application, By End User & By Region |

|

Segments Covered |

By Installation, By vehicle Type & By Geography |

|

Forecast Units |

Value (USD Billion) |

|

Quantitative Units |

Revenue in USD billion and CAGR from 2023 to 2031 |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, and Rest of World |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others. |

|

Companies covered |

Alpine Electronics, Clarion Co., Ltd., Continental AG, Delphi Automotive PLC, Denso Corporation, Harman International, JVC KENWOOD Corporation, Panasonic Corporation, Pioneer Corporation, and Visteon Corporation. |

|

Report Coverage |

Market growth drivers, restraints, opportunities, PEST analysis, market attractiveness analysis by segments and region, company market share analysis.

|

Recent Developments:

Key Benefits of the Report

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.