Automotive Exhaust Systems Market Research Report: By Component (Exhaust Manifold, Muffler, Catalytic Converter, Oxygen Sensor, Exhaust Pipes), By Fuel Type (Gasoline, Diesel), By Vehicle Type (Passenger Car, Commercial Vehicles), and Region (North America, Europe, Asia-Pacific, and Rest of the World) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2024-2032.

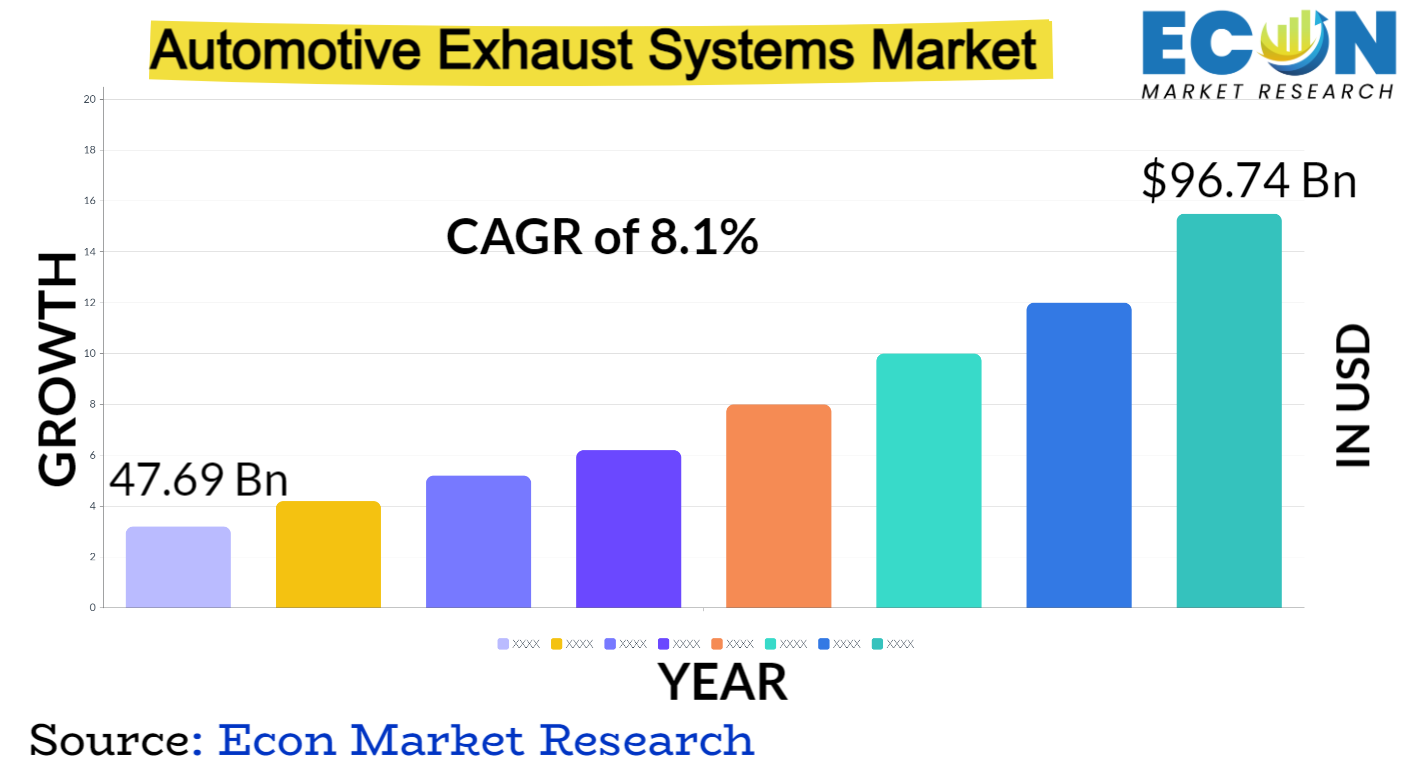

The global automotive exhaust systems market was valued at USD 47.69 billion in 2023 and is estimated to reach approximately USD 96.74 billion by 2032, at a CAGR of 8.1% from 2024 to 2032.

With vital solutions for emissions management and engine performance enhancement, the automotive exhaust systems market has been a key player in the automotive sector. These systems have come a long way since they were first introduced, adapting to stricter environmental laws and new developments in technology. Exhaust systems were originally designed mainly to remove combustion gasses from engines. But once environmental worries surfaced, the market quickly turned its attention to cutting harmful emissions.

A significant advancement in the process of converting poisonous gases into less dangerous molecules was the introduction of catalytic converters. The market has grown over time due to advancements in materials, better catalyst integration, and sensor design and integration. Additionally, the move to hybrid and electric cars has sparked developments in exhaust systems that are compatible with these changing powertrains. Producers are always trying to improve productivity, robustness, and eco-friendliness in order to meet international emission regulations. This market's development is similar to that of the automotive industry, with a focus on performance improvement and sustainability, which keeps it a vital component of vehicle functionality and design.

AUTOMOTIVE EXHAUST SYSTEMS MARKET: REPORT SCOPE & SEGMENTATION

AUTOMOTIVE EXHAUST SYSTEMS MARKET: REPORT SCOPE & SEGMENTATION

|

Report Attribute |

Details |

|

Estimated Market Value (2023) |

47.69 Bn |

|

Projected Market Value (2032) |

96.74 Bn |

|

Base Year |

2023 |

|

Forecast Years |

2024 - 2032 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- By Component, By Fuel Type, By Vehicle Type, & Region |

|

Segments Covered |

By Component, By Fuel Type, By Vehicle Type, & Region |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2024 to 2032 |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, and the Rest of World |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis, and COVID-19 impact analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Automotive Exhaust Systems Market Dynamics

Changes in customer tastes, technological improvements, and regulatory changes all influence the dynamics of the vehicle exhaust systems industry. Globally enforced emission rules have been a major impetus for manufacturers to create advanced exhaust systems that reduce pollutants while maximizing engine efficiency. Ongoing research and development endeavors center on lightweight materials such as titanium, aluminum, and stainless steel to enhance durability and fuel efficiency. Modern technological developments have become essential, such as the incorporation of sensors and selective catalytic reduction (SCR) devices. These developments open the door for predictive maintenance and increased system efficiency in addition to lowering emissions.

The market's requirements have changed as a result of the popularity of hybrid and electric cars. Despite lacking conventional exhaust systems, these cars have inspired the design of emission control systems for range extenders and hybrids with internal combustion engines. Moreover, improvements in exhaust system design to reduce noise and pollutants have been spurred by consumer preferences for cars that are quieter and more environmentally friendly. The market dynamics are changing as the industry moves toward sustainable mobility, underscoring the need for flexible solutions that satisfy consumer demands for high-performance, environmentally friendly cars as well as regulatory requirements.

Automotive Exhaust Systems Market Drivers

The automobile industry's trajectory is being greatly impacted by the shift toward electric and hybrid vehicles, which has a major impact on exhaust system demand, innovation, and development. Growing worries about environmental sustainability and the need to cut greenhouse gas emissions are the main drivers of this shift. Conventional exhaust systems become unnecessary in electric vehicles (EVs) and hybrids, which are powered wholly or partially by electric motors and do away with internal combustion engines. But rather than lessening the importance of exhaust systems, this paradigm change has accelerated their evolution.

Hybrid cars, which run on both electric and internal combustion engines, need complex exhaust systems to control pollutants, particularly when the engine is running. Specialized exhaust solutions are even more necessary because these vehicles frequently use range extenders or additional power sources. The creation of pollution control systems tailored to modern hybrid vehicles has presented exhaust system producers with a chance to reposition their products, emphasizing parts that enhance or supplement electric drivetrains.

These developments cover a wide range of breakthroughs, including improvements to catalytic converters, sensor integration, and material sciences. Exhaust system functioning is optimized and durability is increased by the constant search for innovative materials such as lightweight alloys, premium stainless steel, and advanced ceramics. These materials are needed to increase engine performance, reduce emissions, and enhance efficiency. Exhaust systems have undergone a revolution thanks to the integration of sensors, which allows for real-time emissions and system performance monitoring, predictive maintenance, and emission control.

Moreover, the development of catalytic converters, which now feature advanced catalysts and designs, has proved crucial in reducing dangerous pollutants and guaranteeing adherence to strict emission standards. A paradigm change in emission reduction tactics has been brought about by the development of selective catalytic reduction (SCR) and other emission control technologies. Advancements in technology are also influencing the popularity of hybrid and electric cars, necessitating the need for specific exhaust systems for hybrids and auxiliary parts for electric cars

Restraints:

Manufacturing costs frequently increase when advanced materials, complex catalytic converters, and sophisticated sensors are integrated to meet strict emission standards. These increased expenses may have a direct effect on market penetration and customer affordability. Furthermore, the complicated designs and technology used in contemporary exhaust systems make them more difficult to manufacture, install, and maintain. Adding to the total complexity is the requirement for specialized knowledge and tools for repair or replacement, which may restrict customer and aftermarket service provider accessibility.

The exhaust systems must be updated or modified on a regular basis due to the dynamic nature of regulatory regulations, which raises the complexity and expense of the system. Such high costs and complexity may discourage market adoption, particularly in emerging markets or price-sensitive segments where affordability and ease of maintenance are important factors. Because of this, even though technology has led to performance gains and emissions reductions, the high costs and complexity involved provide significant challenges, requiring the automotive exhaust systems business to strike a careful balance between affordability and innovation.

With the increasing popularity of electric vehicles (EVs), particularly in areas with stricter emissions laws and heightened environmental awareness, the need for internal combustion engines decreases, making conventional exhaust systems obsolete. The primary market for exhaust systems is immediately impacted by this disruptive change, which lessens their significance in the changing car industry. As a result, firms who rely significantly on exhaust components and pollution control systems face difficulties due to the decreasing demand for these goods.

The shift to electric vehicles modifies the dynamics of the supply chain, affecting conventional providers of materials and exhaust system components. This change may result in job losses and reorganization in the car manufacturing industry, which would impact the trained workforce needed for the manufacture and upkeep of exhaust systems. In addition, as EVs do not require traditional exhaust system maintenance, there will be a decrease in the aftermarket for exhaust system replacements and repairs. While the popularity of electric vehicles is a positive step toward more environmentally friendly transportation, the disruption it causes presents problems for producers of conventional exhaust systems and calls for their strategic modification to stay competitive in the rapidly changing automotive market.

Opportunities:

In the market for automobile exhaust systems, the emphasis on sustainability and green technology offers a big potential as well as a stage for innovation and uniqueness. Demand for exhaust systems that actively lower automobiles' carbon footprint in addition to meeting strict emission rules is rising as environmental concerns become more pressing. The development of environmentally friendly exhaust systems, which emphasize the use of renewable materials, reusable components, and innovative manufacturing processes that minimize environmental impact, has been sparked by this shift towards sustainability.

The integration of exhaust systems with cutting-edge green technologies like harvesting and employing waste heat or incorporating renewable energy sources into the exhaust system design is becoming more and more important. These developments correspond with the increasing inclination of consumers towards eco-friendly products, providing a chance for producers to set themselves apart from the competition and serve a market segment that is actively looking for sustainable car solutions. In addition, adopting sustainable practices and green technologies not only satisfies legal requirements but also builds brand loyalty and appeals to a growing number of consumers who place a high value on eco-friendliness. As a result, exhaust system manufacturers are positioned at the forefront of sustainable innovation in the automotive sector.

Research on new materials and manufacturing processes is still ongoing and has the potential to completely transform exhaust system design. Advanced alloys, premium stainless steel, titanium, and composite materials are examples of lightweight, strong materials that have the potential to improve engine performance, increase fuel economy, and improve overall vehicle dynamics. Additionally, by helping to reduce vehicle weight, these materials enable the construction of exhaust systems that not only resist challenging working circumstances but also improve energy efficiency and cut emissions.

Furthermore, developments in material science enable the production of components that are resistant to corrosion, prolonging the life of exhaust systems and lowering maintenance needs. Manufacturers may design exhaust systems that meet changing emission regulations and satisfy consumer desires for durable, effective, and eco-friendly car solutions by utilizing these material advancements. This approach pushes the automotive industry as a whole toward sustainability and improved performance in addition to stimulating innovation in the exhaust systems market.

Segment Overview

Based on components, the global automotive exhaust systems market is divided into exhaust manifolds, mufflers, catalytic converters, oxygen sensors, and exhaust pipes. The exhaust manifolds category dominates the market with the largest revenue share in 2023. These parts gather exhaust gasses from several cylinders and direct them into a single exhaust pipe. Cast iron or stainless steel manifolds are commonly used in exhaust systems, and they are essential in directing exhaust gasses toward the remaining components of the exhaust system.

Mufflers, commonly referred to as silencers, are made to lessen engine noise produced during the system's exhaust gas passage. They use a variety of chambers and baffles to absorb or cancel out sound waves, and they frequently include baffles or other sound-deadening materials like fiberglass to lower noise levels. By catalyzing chemical reactions, catalytic converters are essential emissions control devices that lower dangerous particles in exhaust gas. They contain catalysts such as rhodium, palladium, or platinum that change poisonous gasses like hydrocarbons, nitrogen oxides, and carbon monoxide into less dangerous elements like nitrogen, carbon dioxide, and water vapor.

Oxygen sensors keep an eye on the amount of oxygen in exhaust gases and are typically found both before and after the catalytic converter. The engine control unit (ECU) uses this data to modify the air-fuel mixture, maximizing combustion efficiency and lowering pollutants. The exhaust pipes facilitate the removal of exhaust gasses from the vehicle by moving them from the manifold to the muffler and catalytic converter. They are essential for diverting exhaust gases away from the engine and cabin while maintaining structural integrity and heat resistance. They are usually composed of stainless steel or aluminized steel.

Based on the fuel type, the global automotive exhaust systems market is categorized into gasoline and diesel. The gasoline category leads the global automotive exhaust systems market with the largest revenue share in 2023. These exhaust systems are made especially for automobiles with gasoline-powered motors. Utilizing spark ignition, gasoline engines burn fuel and air to produce exhaust gases that include nitrogen oxides (NOx), hydrocarbons (HC), and carbon monoxide (CO). To regulate emissions and lessen noise, gasoline engine exhaust systems usually include oxygen sensors, mufflers, exhaust manifolds, exhaust pipes, and catalytic converters.

Gasoline engines need exhaust systems designed specifically to handle the special emissions they produce during combustion because of the way they burn. Diesel engines use compression ignition, as opposed to spark ignition, and work on a distinct theory of combustion. Diesel engines produce higher temperatures and more particulate matter (PM) emissions, which diesel exhaust systems are made to withstand. Mufflers, exhaust manifolds, oxygen sensors, exhaust pipes, diesel particulate filters (DPF), exhaust gas recirculation (EGR), selective catalytic reduction (SCR), and exhaust pipes are some of the parts of these systems. Nitrogen oxides (NOx) and particulate matter emissions are the main targets of diesel exhaust systems, which must adhere to strict emission rules by using specialist parts like DPFs and SCR systems.

Based on vehicle type, the global automotive exhaust systems market is segmented into passenger cars and commercial vehicles. The passenger cars segment dominates the automotive exhaust systems market. Passenger car exhaust systems are made to withstand the rigors of operation in personal transportation vehicles. Efficiency, pollution control, and passenger comfort are usually the three main goals of these systems. Catalytic converters, oxygen sensors, mufflers, exhaust pipes, and exhaust manifolds are some of the parts that they consist of.

Performance and comfort must be balanced in exhaust systems since passenger automobiles frequently place a higher priority on lower noise levels, adherence to pollution rules, and improved driving experiences. Commercial vehicles are a broad category that includes utility vehicles used for business, such as trucks, buses, vans, and others. These cars' exhaust systems are designed to operate in harsher environments with increased workloads and temperatures. Larger exhaust manifolds, selective catalytic reduction (SCR) systems, diesel particulate filters (DPF), mufflers, and sturdy exhaust pipes are some of the parts they include.

Automotive Exhaust Systems Overview by Region

The global automotive exhaust systems market is categorized into North America, Europe, Asia-Pacific, and the Rest of the World. Asia-Pacific emerged as the leading region, capturing the largest market share in 2023. The demand for sophisticated exhaust systems has increased due to the region's expanding automotive industry, which is being driven by fast urbanization, rising disposable incomes, and growing car demand. The need for exhaust systems has increased dramatically due to the enormous rise in automotive manufacturing occurring in nations such as China, India, Japan, and South Korea. This growth is being driven by both local consumption and export requirements.

The implementation of strict emission rules in several Asian nations has served as a driving force behind innovation and technological advancement in the development of exhaust systems. Governments in the area have imposed strict emission limits in response to growing environmental concerns. This has made complex exhaust systems necessary to efficiently reduce pollutants. This legislative drive has created an environment where the market for vehicle exhaust systems is more likely to adopt cutting-edge solutions. Furthermore, the area's strong manufacturing skills, bolstered by a trained labor force and advanced technology infrastructure, have made it possible to produce premium exhaust components at cost-effective costs. Because of this, major industry players have solidified their positions in the Asia-Pacific area through collaborations and local production sites, thus enhancing the region's standing as a leading force in the worldwide automotive exhaust systems market.

Automotive Exhaust Systems Competitive Landscape

In the global automotive exhaust systems market, a few major players exert significant market dominance and have established a strong regional presence. These leading companies remain committed to continuous research and development endeavors and actively engage in strategic growth initiatives, including product development, launches, joint ventures, and partnerships. By pursuing these strategies, these companies aim to strengthen their market position, expand their customer base, and capture a substantial share of the market.

Some of the prominent players in the global automotive exhaust systems market include,

Automotive Exhaust Systems Recent Developments

Automotive Exhaust Systems Market Report Segmentation

|

ATTRIBUTE |

DETAILS |

|

By Component |

|

|

By Fuel Type |

|

|

By Vehicle Type |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.

+1 812 506 4440

+1 812 506 4440

+91 7875074426

+91 7875074426