Global Aseptic Packaging Market Report: By Product (Cartons (Tetrapak, Combibloc), Bags and Pouches, Cans, Bottles)), Application (Beverages (Ready-to-drink, Dairy-based Beverages), Food (Processed Foods, Fruits and Vegetables, Dairy Food), Pharmaceutical)), and Region (North America, Europe, Asia-Pacific, Latin America, Middle-East and Africa) Global Industry Analysis, Size, Share, Growth, Trends, Regional Analysis, Competitor Analysis and Forecast 2024-2032.

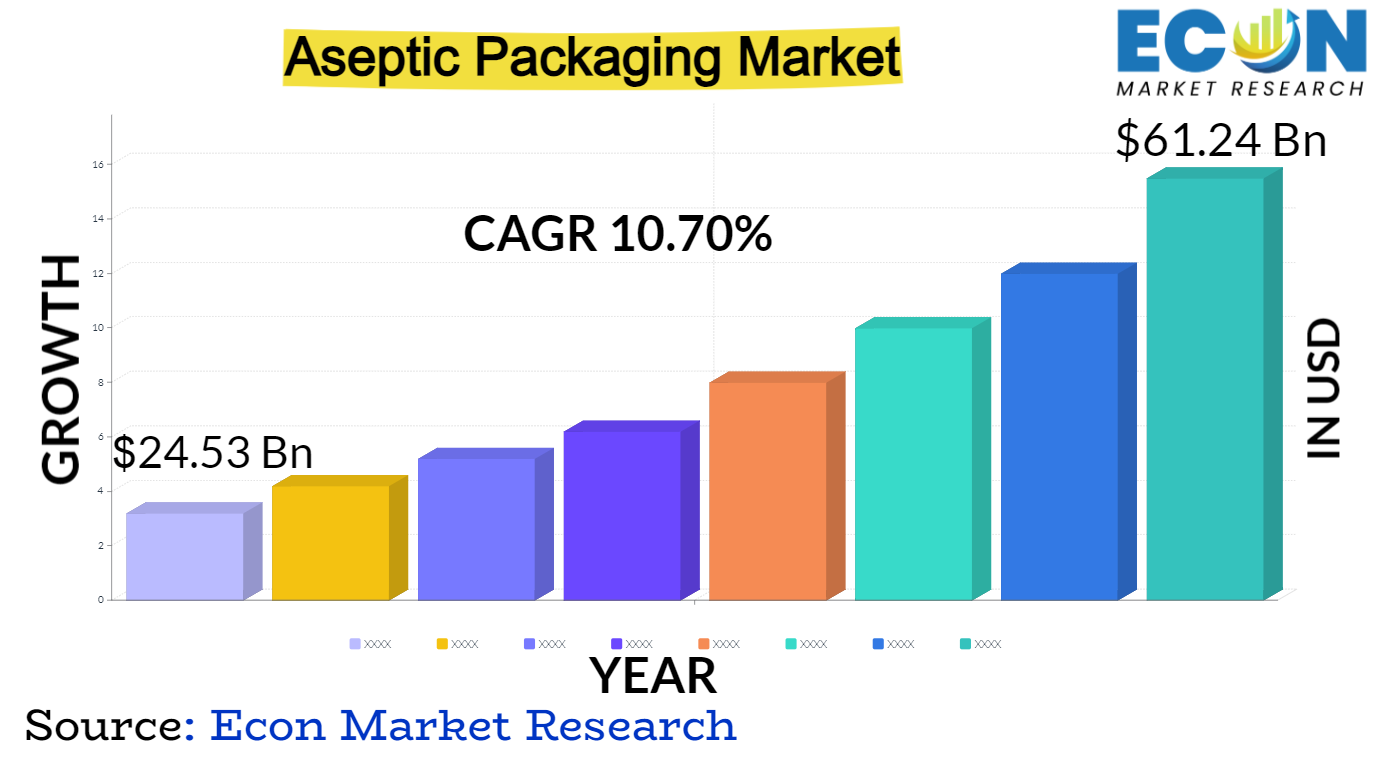

Global Aseptic Packaging market is predicted to reach approximately USD 61.24 billion by 2032, at a CAGR of 10.70% from 2024 to 2032.

Aseptic packaging refers to the method of filling sterile products into sterile containers in a sterile environment to maintain their shelf life without refrigeration or chemical preservatives. The global aseptic packaging market is experiencing significant growth attributed to the increasing demand for convenient and safe packaging solutions across various industries such as food and beverage, pharmaceuticals, and healthcare.

The market is driven by factors such as the growing preference for convenient and ready-to-eat food products, rising concerns regarding food safety and hygiene, and advancements in packaging technology. Moreover, the expanding urban population, changing lifestyle patterns, and increasing disposable incomes further contribute to the market's expansion. Aseptic packaging offers several advantages including prolonged shelf life, reduced transportation costs, enhanced product safety, and improved storage efficiency, thereby driving its adoption across diverse sectors. However, challenges such as high initial investment costs and stringent regulatory requirements may hinder market growth to some extent.

Despite these challenges, manufacturers are increasingly focusing on developing innovative and sustainable packaging solutions to cater to evolving consumer preferences and regulatory standards. Geographically, the Asia-Pacific region is expected to witness substantial growth in the aseptic packaging market owing to rapid urbanization, industrialization, and increasing consumer awareness regarding food safety and hygiene. Additionally, strategic initiatives such as mergers and acquisitions, collaborations, and product innovations are prevalent among key players to strengthen their market presence and gain a competitive edge.

Global Aseptic Packaging report scope and segmentation.

|

Report Attribute |

Details |

|

Estimated Market Value (2023) |

USD 24.53 billion |

|

Projected Market Value (2032) |

USD 61.24 billion |

|

Base Year |

2023 |

|

Forecast Years |

2024 – 2032 |

|

Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment- Based on By Product, By Application, & Region. |

|

Segments Covered |

By Product, By Application, & By Region. |

|

Forecast Units |

Value (USD Billion or Million), and Volume (Units) |

|

Quantitative Units |

Revenue in USD million/billion and CAGR from 2024 to 2032. |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. |

|

Countries Covered |

U.S., Canada, Mexico, U.K., Germany, France, Italy, Spain, China, India, Japan, South Korea, Brazil, Argentina, GCC Countries, and South Africa, among others. |

|

Report Coverage |

Market growth drivers, restraints, opportunities, Porter’s five forces analysis, PEST analysis, value chain analysis, regulatory landscape, market attractiveness analysis by segments and region, company market share analysis. |

|

Delivery Format |

Delivered as an attached PDF and Excel through email, according to the purchase option. |

Global Aseptic Packaging dynamics

The growing need for practical and secure packaging options in a variety of sectors, including food and beverage, pharmaceutical, and healthcare, is one important motivator. As a result of consumers' growing preferences for ready-to-eat and portable food items, aseptic packaging—which extends shelf life without requiring refrigeration or preservatives—is in high demand. Additionally, aseptic packaging solutions have become more popular due to growing concerns about food safety and hygiene, as they help prevent contamination and preserve product integrity throughout the supply chain.

Technological developments in packaging are another important factor propelling market expansion. In order to develop novel packaging materials and methods that maximise product safety, reduce environmental impact, and increase cost-effectiveness, manufacturers are investing in research and development. As a result of rising packaged food and beverage consumption brought on by changing lifestyle patterns and an expanding urban population, there is an even greater need for aseptic packaging solutions.

Notwithstanding, the market encounters obstacles like elevated initial investment expenses and rigorous regulatory mandates. For manufacturers, creating sterile production environments and guaranteeing adherence to regulatory requirements can be expensive and time-consuming. Further difficulties for market participants come from shifting raw material prices and the requirement for constant innovation to satisfy changing consumer preferences.

Global Aseptic Packaging drivers

The increasing preference for convenient and safe packaging solutions across various industries, including food and beverage, pharmaceuticals, and healthcare, is a major driver for the aseptic packaging market. Consumers are increasingly seeking ready-to-eat and on-the-go food products, which require packaging that can maintain freshness and safety without the need for refrigeration or preservatives. Aseptic packaging offers extended shelf life and helps prevent contamination, addressing consumers' concerns about food safety and hygiene. Furthermore, as lifestyles become more fast-paced, the demand for convenient packaging solutions continues to rise, driving the adoption of aseptic packaging technologies globally.

The aseptic packaging market is expanding due to technological advancements in the packaging industry. In order to develop new materials, procedures, and tools that increase product safety, lessen their negative effects on the environment, and increase their cost-effectiveness, manufacturers are spending money on research and development. Manufacturers can accomplish greater levels of sterility, accuracy, and efficiency in the packaging process thanks to advanced aseptic packaging technologies. Furthermore, cutting-edge packaging innovations like clever packaging solutions and eco-friendly packing materials are gaining popularity and providing sustainable substitutes for conventional packaging techniques. In addition to satisfying consumer expectations for environmentally friendly and safe packaging, these technological developments also help manufacturers increase their operational efficiency and competitiveness.

Restraints:

One of the significant restraints for the aseptic packaging market is the high initial investment required for setting up sterile manufacturing environments and acquiring specialized equipment. Establishing aseptic packaging facilities involves substantial capital investment in infrastructure, machinery, and personnel training to ensure compliance with stringent regulatory standards. Additionally, ongoing maintenance and operational costs further contribute to the financial burden on manufacturers, especially for small and medium-sized enterprises (SMEs). The high entry barriers due to capital-intensive nature limit the market entry of new players and pose challenges for existing manufacturers looking to expand their operations.

The aseptic packaging industry is subject to stringent regulatory requirements imposed by government authorities and international standards organizations to ensure product safety and quality. Compliance with regulations such as Good Manufacturing Practices (GMP), Hazard Analysis and Critical Control Points (HACCP), and Food and Drug Administration (FDA) guidelines is essential for manufacturers to operate in the market. Meeting regulatory standards entails significant investments in quality control measures, documentation, and audits, which can increase operational costs and complexity. Moreover, frequent updates and changes in regulatory requirements pose challenges for manufacturers in maintaining compliance and adapting to evolving standards, thereby restraining market growth.

Opportunities:

Growing environmental concerns and heightened awareness of sustainability are creating opportunities for the aseptic packaging market. Consumers are increasingly seeking eco-friendly packaging alternatives that minimize environmental impact and support recycling and waste reduction efforts. Aseptic packaging technologies offer several advantages in terms of resource efficiency, energy savings, and recyclability compared to traditional packaging materials such as glass and metal. Manufacturers can leverage this growing demand for sustainable packaging solutions by investing in eco-friendly materials, optimizing packaging designs, and promoting recycling initiatives. Moreover, governments and regulatory bodies are implementing policies and incentives to encourage the adoption of sustainable packaging practices, further driving market growth.

Segment Overview

By product, the aseptic packaging market encompasses a variety of packaging types tailored to different consumer needs and industry requirements. Cartons, including popular brands like Tetra Pak and Combibloc, represent a significant segment within aseptic packaging. These cartons offer lightweight, durable, and customizable packaging solutions suitable for a wide range of products, including beverages, dairy, and processed foods. Bags and pouches are another prominent product segment, known for their flexibility, portability, and convenience. These packaging formats are commonly used for packaging liquids, snacks, and other consumables, offering consumers on-the-go convenience and portion control. Cans and bottles, although traditional packaging formats, continue to be widely used in the aseptic packaging market, particularly for beverages and pharmaceutical products. Cans provide excellent protection against light and oxygen, making them suitable for preserving the quality and freshness of beverages, while bottles offer versatility in shape, size, and material, catering to diverse packaging needs across industries.

In terms of applications, the aseptic packaging market serves various sectors, with beverages emerging as a primary application segment. Ready-to-drink beverages, including juices, teas, and sports drinks, are commonly packaged using aseptic technology to ensure product safety and extend shelf life. Dairy-based beverages, such as milk and yogurt drinks, also rely on aseptic packaging to maintain freshness and nutritional quality without the need for refrigeration. The food application segment encompasses a wide range of products, including processed foods, fruits, vegetables, and dairy products. Aseptic packaging helps preserve the flavor, texture, and nutritional value of these food items while offering convenience and extended shelf life. In the pharmaceutical sector, aseptic packaging plays a critical role in preserving the efficacy and safety of drugs and medical products. Sterile packaging solutions ensure product integrity and compliance with regulatory standards, making aseptic packaging indispensable for pharmaceutical companies worldwide.

Global Aseptic Packaging Overview by Region

North America holds a prominent position in the market, driven by the robust demand for convenient and safe packaging solutions across the food and beverage, pharmaceutical, and healthcare industries. The region benefits from a well-established infrastructure, advanced manufacturing capabilities, and stringent regulatory standards, which encourage the adoption of aseptic packaging technologies. Moreover, changing consumer lifestyles, increasing disposable incomes, and growing concerns regarding food safety and hygiene contribute to the market's growth in North America. Similarly, Europe emerges as a key market for aseptic packaging, propelled by the region's strong emphasis on sustainability, innovation, and quality assurance.

European consumers prioritize eco-friendly packaging solutions and are receptive to novel packaging formats and materials that enhance product safety and environmental sustainability. Additionally, stringent regulations governing food and pharmaceutical packaging drive the adoption of aseptic packaging technologies across the European market. In the Asia-Pacific region, rapid urbanization, expanding middle-class population, and rising consumer awareness fuel the demand for aseptic packaging solutions. Countries such as China, India, and Japan witness significant market growth attributed to increasing consumption of packaged foods, beverages, and pharmaceutical products. Moreover, government initiatives promoting food safety, hygiene, and technological innovation further bolster market expansion in the Asia-Pacific region.

Latin America and the Middle East & Africa regions also present lucrative opportunities for the aseptic packaging market, driven by urbanization, industrialization, and changing consumer preferences. While these regions face challenges related to infrastructure development, economic instability, and regulatory complexities, they offer untapped potential for market players willing to invest in localized production facilities and strategic partnerships.

Global Aseptic Packaging market competitive landscape

Key players such as Tetra Pak, SIG Combibloc Group AG, Amcor Limited, and Elopak AS dominate the market with their extensive product portfolios, global reach, and strong brand recognition. These industry leaders continually invest in research and development to introduce advanced packaging solutions that address evolving consumer preferences, regulatory requirements, and sustainability concerns. Moreover, strategic collaborations, mergers, and acquisitions are prevalent strategies among major players to enhance their market presence, expand geographical footprint, and diversify product offerings. Additionally, companies are focusing on developing eco-friendly packaging materials, reducing carbon footprint, and improving operational efficiencies to stay competitive in the market.

Alongside established players, a growing number of startups and niche players are entering the aseptic packaging market, leveraging innovative technologies and business models to disrupt traditional packaging practices. These emerging companies focus on niche markets, specialty applications, and customized packaging solutions to cater to specific industry needs and consumer demands. Furthermore, technological advancements such as smart packaging, active and intelligent packaging, and digital printing are reshaping the competitive landscape, offering new opportunities for differentiation and value creation. As competition intensifies, companies are investing in marketing initiatives, brand building, and customer engagement strategies to differentiate their offerings and build long-term relationships with clients.

Global Aseptic Packaging Recent Developments

Scope of global Aseptic Packaging report

Global Aseptic Packaging report segmentation

|

ATTRIBUTE |

DETAILS |

|

By Product |

|

|

By Application |

|

|

By Geography |

|

|

Customization Scope |

|

|

Pricing |

|

Objectives of the Study

The objectives of the study are summarized in 5 stages. They are as mentioned below:

Research Methodology

Our research methodology has always been the key differentiating reason which sets us apart in comparison from the competing organizations in the industry. Our organization believes in consistency along with quality and establishing a new level with every new report we generate; our methods are acclaimed and the data/information inside the report is coveted. Our research methodology involves a combination of primary and secondary research methods. Data procurement is one of the most extensive stages in our research process. Our organization helps in assisting the clients to find the opportunities by examining the market across the globe coupled with providing economic statistics for each and every region. The reports generated and published are based on primary & secondary research. In secondary research, we gather data for global Market through white papers, case studies, blogs, reference customers, news, articles, press releases, white papers, and research studies. We also have our paid data applications which includes hoovers, Bloomberg business week, Avention, and others.

Data Collection

Data collection is the process of gathering, measuring, and analyzing accurate and relevant data from a variety of sources to analyze market and forecast trends. Raw market data is obtained on a broad front. Data is continuously extracted and filtered to ensure only validated and authenticated sources are considered. Data is mined from a varied host of sources including secondary and primary sources.

Primary Research

After the secondary research process, we initiate the primary research phase in which we interact with companies operating within the market space. We interact with related industries to understand the factors that can drive or hamper a market. Exhaustive primary interviews are conducted. Various sources from both the supply and demand sides are interviewed to obtain qualitative and quantitative information for a report which includes suppliers, product providers, domain experts, CEOs, vice presidents, marketing & sales directors, Type & innovation directors, and related key executives from various key companies to ensure a holistic and unbiased picture of the market.

Secondary Research

A secondary research process is conducted to identify and collect information useful for the extensive, technical, market-oriented, and comprehensive study of the market. Secondary sources include published market studies, competitive information, white papers, analyst reports, government agencies, industry and trade associations, media sources, chambers of commerce, newsletters, trade publications, magazines, Bloomberg BusinessWeek, Factiva, D&B, annual reports, company house documents, investor presentations, articles, journals, blogs, and SEC filings of companies, newspapers, and so on. We have assigned weights to these parameters and quantified their market impacts using the weighted average analysis to derive the expected market growth rate.

Top-Down Approach & Bottom-Up Approach

In the top – down approach, the Global Batteries for Solar Energy Storage Market was further divided into various segments on the basis of the percentage share of each segment. This approach helped in arriving at the market size of each segment globally. The segments market size was further broken down in the regional market size of each segment and sub-segments. The sub-segments were further broken down to country level market. The market size arrived using this approach was then crosschecked with the market size arrived by using bottom-up approach.

In the bottom-up approach, we arrived at the country market size by identifying the revenues and market shares of the key market players. The country market sizes then were added up to arrive at regional market size of the decorated apparel, which eventually added up to arrive at global market size.

This is one of the most reliable methods as the information is directly obtained from the key players in the market and is based on the primary interviews from the key opinion leaders associated with the firms considered in the research. Furthermore, the data obtained from the company sources and the primary respondents was validated through secondary sources including government publications and Bloomberg.

Market Analysis & size Estimation

Post the data mining stage, we gather our findings and analyze them, filtering out relevant insights. These are evaluated across research teams and industry experts. All this data is collected and evaluated by our analysts. The key players in the industry or markets are identified through extensive primary and secondary research. All percentage share splits, and breakdowns have been determined using secondary sources and verified through primary sources. The market size, in terms of value and volume, is determined through primary and secondary research processes, and forecasting models including the time series model, econometric model, judgmental forecasting model, the Delphi method, among Flywheel Energy Storage. Gathered information for market analysis, competitive landscape, growth trends, product development, and pricing trends is fed into the model and analyzed simultaneously.

Quality Checking & Final Review

The analysis done by the research team is further reviewed to check for the accuracy of the data provided to ensure the clients’ requirements. This approach provides essential checks and balances which facilitate the production of quality data. This Type of revision was done in two phases for the authenticity of the data and negligible errors in the report. After quality checking, the report is reviewed to look after the presentation, Type and to recheck if all the requirements of the clients were addressed.